WST 1Q 2018 Commentary

Right on cue volatility returned to the global investment markets in the first quarter of 2018 as the sanguine complacency of 2017 gave way to broad concerns about Fed policy, trade protectionism, and the outlook for technology stocks. After a strong start the S&P 500 peaked on January 26, with the January employment report triggering the long-awaited 10% correction in U.S. equities. Expanding payrolls and a 2.9% increase in average hourly earnings for private sector workers, the fastest increase since 2009, indicated to investors that the economy is heating up and raised fears that the Fed will raise interest rates more quickly than expected. The yield on the 10-year Treasury note jumped to 2.85%, up from around 2% in September, and stocks fell sharply.

Follow this link to access and download a printer-friendly version of our commentary.

Expectations about central bank liquidity and the direction of monetary policy were the most important factors influencing the financial markets in the first quarter, but other developments have played a role in the recent volatility. Since President Trump’s election in November 2016 the markets have generally endorsed his policy mix of tax cuts and deregulation, but now investors are weighing the threat the administration’s confrontational trade policy poses for corporate profits and economic growth. While the specific impact of a trade war on the global economy is difficult to estimate or quantify, the sour tone of the rhetoric about retaliatory tariffs has diminished investors’ appetite for risk.

Over the course of the quarter, just as the economic picture was clouded by concerns about Fed policy and trade policy, equity investors also faced new worries about the seemingly invulnerable Big Tech sector of the stock market. We observe that outsized returns from a small number of large technology companies have been the foundation for the long bull market, but recent events threaten that trend. In March anger about the release of personal data on over 80 million Facebook users, whiplash from the news of a fatality involving a self-driving Uber car, and the general sense that political risk is rising for Big Tech together led investors to question their long-held assumption that the FANG stocks (Facebook, Apple, Amazon, Netflix, Google) are invincible. The President's Twitter attack on Amazon and its CEO Jeff Bezos, who also owns the Washington Post, is the most overt example of the shift in the political tide, but concerns about how these companies store, use, and sell personal data have been rising and will likely lead to increased regulation, with big implications for the entire social media business model.

The best news for investors is that even with macro uncertainty on the rise and the tech sector under fire, the financial markets remain supported by solid fundamentals. For now, the synchronized global economic expansion continues. The U.S. tax overhaul and infrastructure spending plans have boosted corporate capital investment and earnings, making the markets’ valuation multiples more reasonable. Still, the economic recovery in the U.S. is mature and vulnerable to the risks outlined above, and as we will discuss in the equity section later in the letter stock valuations depend upon corporations’ ability to deliver the earnings that Wall Street expects.

On balance we are maintaining our slightly more-conservative-than -normal portfolio positioning. Investor willingness to "buy the dips” suggests that sentiment is still too strong, and investors not worried enough for the quick correction we’ve seen so far to be the end of this new period of volatility. 2018 will be a year of transition, most importantly a transition in Fed policy, and short-term interest rates have risen enough already to offer a reasonable alternative to stock dividends for income-oriented investors. If a trade war occurs or if corporate earnings fail to materialize as expected, sentiment could shift quickly.

Economic Overview and Fed Policy

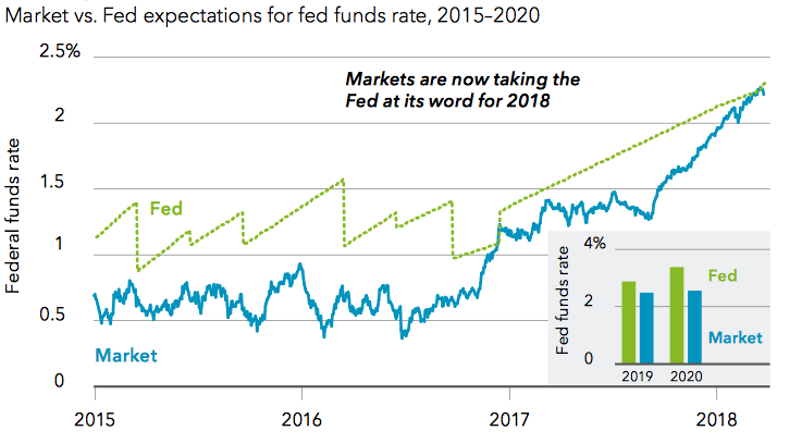

The global economy has continued its steady progress in 2018 as economic growth around the world remains solid. According to the Fed, after growing 3.2% in 2016 and 3.6% in 2017, real global GDP is expected to expand 3.5% this year and next, in line with the long-term average. Despite the positive fundamentals the general tone on Wall Street shifted over the course of the quarter, as optimism about healthy growth gave way to concerns about inflation and rising interest rates. The U.S. unemployment rate has hovered at a 17-year low since October, and the tight labor market has finally started to drive wage growth and inflation, which ticked above 2% in the quarter. The “Goldilocks” environment of steady growth and strong employment trends coupled with low inflation and accommodative Fed policy produced fertile conditions for the market in recent years. Now, with the Fed having made clear its intention to continue raising interest rates and reducing its balance sheet, investors are uneasy. Federal Reserve Chairman Jay Powell presided over his first meeting of the FOMC in March, and while the path of rate increases that the committee outlined for 2018 was a bit shallower than the market anticipated the longer-term projection for the fed funds rate as demonstrated by the post-meeting “dot plot” was steeper. The committee believes the economy is on a faster and more sustainable growth path than it was in 2017, with inflation set to pick up “notably” this spring. Despite stated caution about the longer term risks the economy faces, the Fed appears determined to continue the path of policy normalization begun under Janet Yellen. Very importantly, as the chart below reveals, there exists a major disconnect between the Fed’s stated projection for the policy rate over the next three years and market expectations.

Sources: BlackRock Investment Institute, with data from Bloomberg and Credit Suisse, March 2018. Notes: The chart shows the 12-month forward market-implied fed funds rate (using overnight index swaps) versus the 12-month forward path implied by the Fed’s “dots” in its Statement of Economic Projections. The inset chart shows the Fed’s dots for 2019 and 2020 versus market expectations as measured by Credit Suisse

While market interest rates have caught up with Fed projections for this year, the median projected fed funds rate for the end of 2020 according to the “dot plot” is now 3.4%, double the current rate, significantly higher than current market expectations, and well above today’s 30-year Treasury bond yield of 3.0%. We interpret the Fed’s message to be that they are determined to normalize policy over the next three years, and we expect considerable eruptions of market volatility as they pursue that objective.

Trade War – A Tariffying Possibility

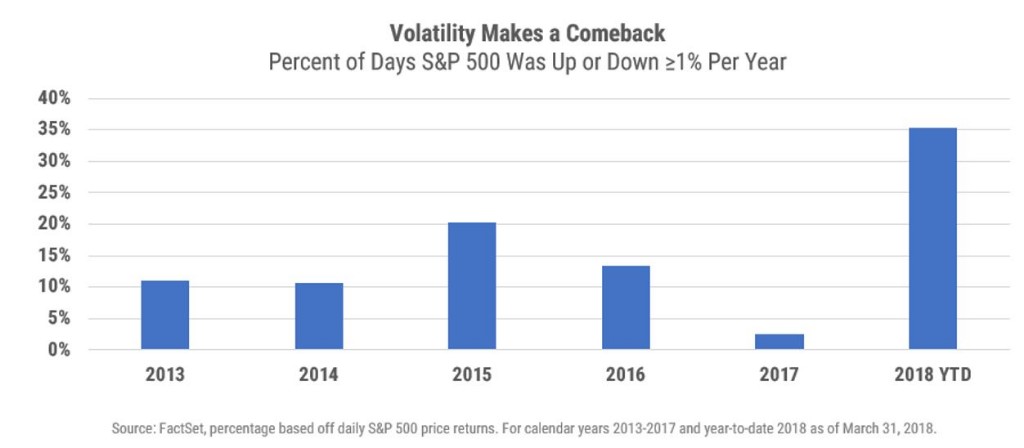

Beginning in late March and continuing as the second quarter unfolds, intensifying fears of a trade war with China are driving market volatility to levels last seen during the financial crisis. Through mid-March the S&P 500 had moved 1% or more on 35% of the trading days this year, a sea change from the stability (in the form of historical low levels of volatility) observed in 2017. This volatility reflects legitimate concerns that a prolonged trade conflict could dampen growth, drive a surge in inflation and derail the economy.

As we write this letter counterpunches have escalated the conflict since the original exchange between the U.S. and China that threatened 25% tariffs on $50 billion of imports on each side. At those levels the tariffs would impact about 10% of China's $500 billion of exports to the US and almost 40% of our exports to China. President Trump considers our annual $300 billion trade deficit with China and their purported theft of $50 billion worth of U.S. intellectual property through coercion and cyber-attacks to be affronts worth fighting over, and the administration started the spat by announcing a 25% import tariff on steel and 10% on aluminum.[1]

Trade experts suggest that the U.S. tariff list, which begins with metals producers, is a blunt instrument designed to protect a few specific industries from foreign competition, while the list China published on April 4th is subtler and is aimed at influencing broad trade policies. As The Economist points out China’s list directly defies World Trade Organization rules and hits at pressure points in America’s democracy, including industries with powerful lobbies like aircraft and soy beans, and products from politically sensitive states. Wisconsin is home both to Paul Ryan, the Speaker of the House of Representatives, and a sizeable share of America’s cranberry exporters. Mitch McConnell, the Republican leader of the Senate, represents Kentucky, home to America’s bourbon exporters. Both products are included in China’s tariff threat list.[2] Optimists contend that this political approach and the measured size of China’s threatened retaliation (matching almost exactly the U.S. levels in each round of tit-for-tat announcements) suggest the Chinese are willing to pursue dialogue with the U.S. to address the disputes.

While the U.S. has legitimate gripes about Chinese trade practices, even a just trade war will have collateral damage. Many U.S. companies will be hurt if the tariffs are implemented, even if the actions are short-lived, and a protracted conflict will stifle growth and spur inflation. Localized damage from a short skirmish that ends with a new trade agreement between the U.S. and China should not deal too severe a body blow to the $19 trillion U.S. economy, and a new deal that addresses Trump’s grievances would be worth fighting for. However, early April’s unsettled markets reveal the concern and uncertainty bred by a more adversarial global trade environment, and if it continues that uncertainty will hamper investment and trigger more volatility in the financial markets.

Equity Market Overview

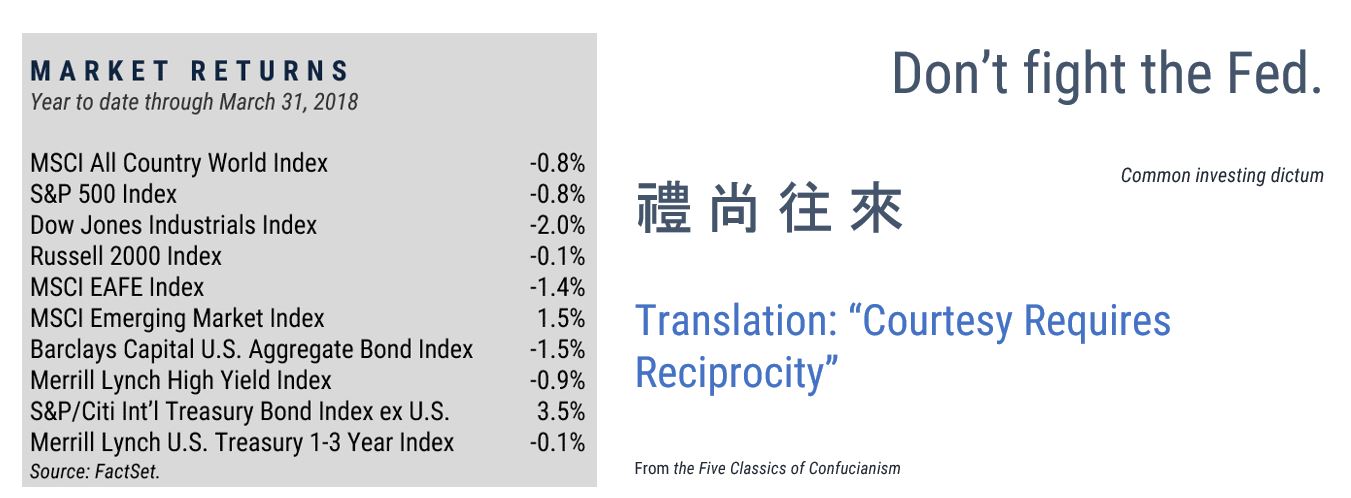

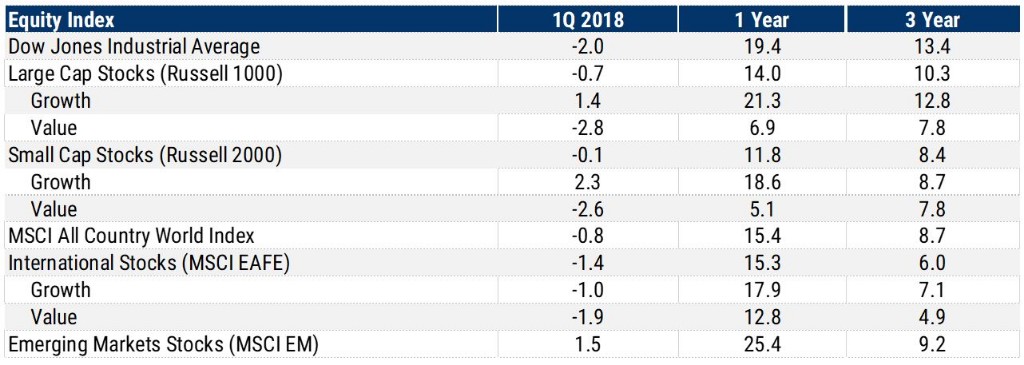

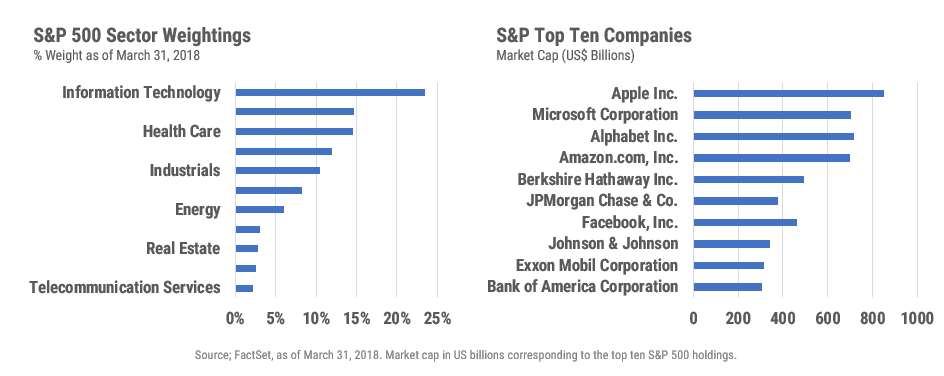

The S&P 500 responded to the new environment of risk with an approximately 1% decline for the three months ended March 31st, its first negative quarter since 2015. That small drop masks the surge in volatility that led U.S. equities to new highs on January 26 and then saw both the S&P 500 and the Dow Jones Industrial Average enter correction territory (defined as a 10% decline from peak) two weeks later. The Dow plummeted 3,200 points during those two weeks and the excitement included two 1,000-point intra-day declines. At those levels the markets’ strong earnings performance and expectations for even higher corporate profits this year provided support for stocks and they bounced back each time. Based upon the improving earnings forecasts and the quarter’s small declines in stock prices, the S&P 500 now trades at price-to-earnings multiple close to that a year ago despite 2017’s price gains. The consensus estimate for S&P 500 earnings in 2018 is $158.00, an increase of 20% over 2017, so the index now trades at less than 16.4 times forward earnings estimates, just a bit higher than the 25-year average of 16.1.[1]

Source: FactSet, as of March 31, 2018.

Source: FactSet, as of March 31, 2018.

Developed market non-U.S. stocks also struggled in the first quarter after outpacing domestic stocks in 2017. The MSCI EAFE returned -1.4% for the quarter while the broad MSCI ACWI ex U.S. Index was down 0.8%. Emerging markets were the only geographic equity class with positive returns as the MSCI Emerging Markets Index rose 1.5%. Emerging markets benefited from investor cash flows following their strong returns in 2017, in contrast to the equity asset class overall which saw net negative money flows over the course of the quarter. The performance of the international equity segment benefited from continued weakness in the dollar, which makes holdings of foreign stocks more valuable for U.S. investors. The Euro has strengthened 14% versus the dollar over the past 12 months, a boon for U.S. investors but a challenge for the European companies receiving dollar revenues from abroad. About half of the revenue of the Stoxx Europe 600 index comes from abroad, so continued dollar weakness, a likelihood in the event of a trade war, would create headwinds to their profitability.[1] As it stands now, we are maintaining our weightings to international equities in portfolios but watching closely. The dynamics around tariffs and a possible trade war could have important implications for the relative performance of various geographies.

While the broad market rebound at the end of the quarter was supported by resurgent technology stocks, clouds are gathering around the Big Tech sector and forcing investors to rethink the assumption that the companies that make up the FANG+ Index are invincible. Arguably the creation last year of that index, which comprises “a select group of highly-traded growth stocks of next generation technology and tech-enabled companies”[2] is evidence of excessive enthusiasm for the companies that make it up: Facebook, Amazon, Apple, Netflix, Google, Alibaba, Baidu, Nvidia, Tesla, and Twitter. Certainly, the sector has been the engine of the bull market. While the S&P 500 enjoyed a return of 19% in 2017 the Tech sector overall was up 37%, and since the beginning of last year the FANG+ index is up over 70% compared with 18% for the S&P 500. The growth of the FANGS and the technology sector has transformed the composition of the overall equity market. The information technology sector of the S&P 500, which does not even include Amazon because it is classified a consumer discretionary stock by S&P, accounts for about a quarter of the overall index.

This concentration of value in one sector and such a small number of companies increases overall market risk and draws our focus to the important emerging challenges facing those companies. The fundamental driver of the growth in the technology realm is the buildout of infrastructure and services to meet the needs of people and companies as they move their lives online and into the Cloud. As that process has evolved two distinct sets of issues have come under scrutiny. The Facebook data breach highlighted the first issue, social media security concerns around personal data. The magic of modern technology is its ability to know us and connect us with people, products, and services that we like and in which we are interested, and our willingness to allow companies to collect that data and use it to make those connections has largely been taken for granted until recently. As customers and legislators demand better data security and more privacy, the social media and marketing companies will need to find ways create the magic without compromising the safety of their customers’ data.

The second issue is the scale and power companies achieve as data and services are concentrated with fewer providers. Trump’s antagonism toward Amazon may be partially political but will have a meaningful impact on the company’s profitability if, for example Amazon’s shipping costs increase because the Postal Service raises their rates, as Trump is threatening. European Union antitrust chief Margrethe Vestager has made it her mission to ensure dominant tech companies don’t abuse their power to stifle innovation and competition. Among recent actions the EU fined Google €2.4 billion last year for allegedly using its dominance in search to favor its own online shopping service, and fined Facebook €110 million for misleading regulators during their review of its acquisition of messaging company WhatsApp.[1] U.S. regulators are watching the EU’s progress closely, and we anticipate more regulation from Washington as the process evolves.

Financial Times tech analyst Rana Foroohar suggests Silicon Valley has become the new Wall Street and is now “the prime target for a populist backlash in a world increasingly bifurcated, economically and socially. Big Tech has been among the most politically insulated sector in the S&P 500, while financials and energy have been the most closely scrutinized and regulated,” according to Foroohar.[2] Investors will need to consider how these roles may reverse in the current administration, and how increased regulation and scrutiny will impact the pace of product development in the technology sector and the profitability of those companies. More regulation means more administrative costs for existing companies and higher barriers to entry for new ones, both of which will stifle growth.

Bond Market Overview

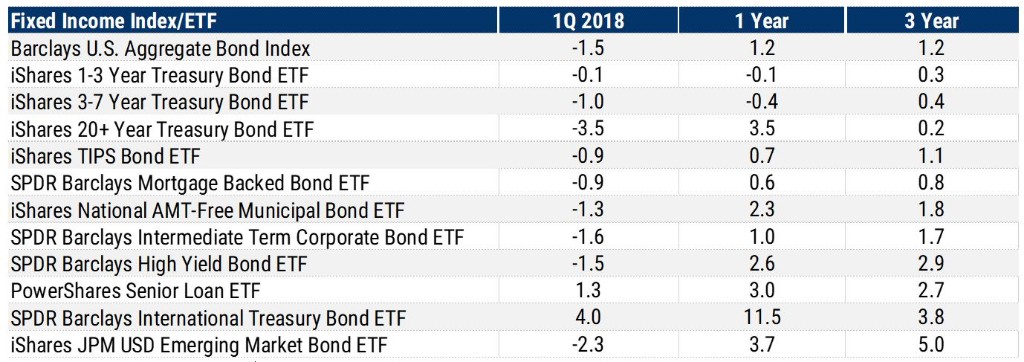

Despite a flight-to-quality rally in the last week of March the bond market had a tough start to 2018, and the Barclay’s Aggregate Bond Index declined 1.5% for the quarter. For most of our clients bonds are the least interesting part of the portfolio, but with the Fed in the news and fixed income returns in the red, we are fielding lots of questions about portfolio positioning in a rising rate environment. That concern is understandable. The Fed rate hike in December 2015 was a reversal of 10 years of unprecedented monetary accommodation, and the pace of the Fed’s policy shift has accelerated with three rate hikes in 2017, one in March 2018, and two or three more expected this year. The 10-year Treasury closed the quarter with a 2.74% yield, up sharply from the 2.40% level at which it ended 2017. In late February and early March the 10-year yield reached 2.9% and looked poised to make a run at the psychologically important 3% level before late-quarter weakness in stocks led investors back to the safety of bonds. Along with long-term Treasuries corporate bonds were the worst performing segment of the market in the first quarter, as pent up supply from companies awaiting details of the tax plan last year hit the market. International bonds and bond funds were the best-performing segment, with all the sector’s outperformance driven by the decline in the dollar. Just as in the case of international stocks, foreign bonds held by dollar-based investors rise in value as the dollar declines.

Source: FactSet, as of March 31, 2018.

Looking at the remainder of the year we see increasing headwinds for bonds. Short-term bonds will respond to the Fed policy rate, which the FOMC has committed to increasing. Longer-term bonds yields, which are more sensitive to market expectations about economic growth and inflation, also rose in the first quarter, and are vulnerable for several reasons. Inflation expectations have remained stuck in the 2% range, but we see important inflationary pressures that are not yet priced into the market. We mentioned the impact of the strong labor market, and survey data from the Business Roundtable indicate that businesses of all sizes continue to expand, hire more workers, and raise wages. Also, import prices rise as the dollar weakens, and were up 3.5% year-over-year in February, well ahead of expectations.[1] The biggest risk to the current benign inflation outlook is the possibility of a trade war. Tariffs and trade wars are inflationary, causing prices on imported goods to increase and pressing U.S. companies to raise prices on domestic products to make up for the loss of export sales. If tariffs are implemented they will lead to higher input prices for many manufacturing and construction industries which rely on steel and aluminum imports, ultimately resulting in higher prices for U.S. consumers. Altogether the strong U.S. economy, weaker dollar and risky trade picture lead us to factor rising inflation into our thinking.

Those inflationary pressures come at a time when bond market supply and demand dynamics have also shifted and created new challenges for fixed income investors. Throughout 2016 and 2017 the Fed, Bank of Japan, European Central Bank, and Bank of England collectively bought fixed income assets at a rate of about $150 billion per month. This expansive monetary policy, which supported bond prices, is reversing now. The Fed, for example, reduced its balance sheet by $12 billion in March. On the supply side of the equation increased spending and lower tax rates will increase budget deficits in the U.S, forcing the Treasury to issue more debt to cover the gap. Depending upon how the trade squabble unfolds Beijing could unwind part of its vast $1.2 trillion holdings in U.S. Treasuries, a move that would pressure the dollar and push bond yields higher.

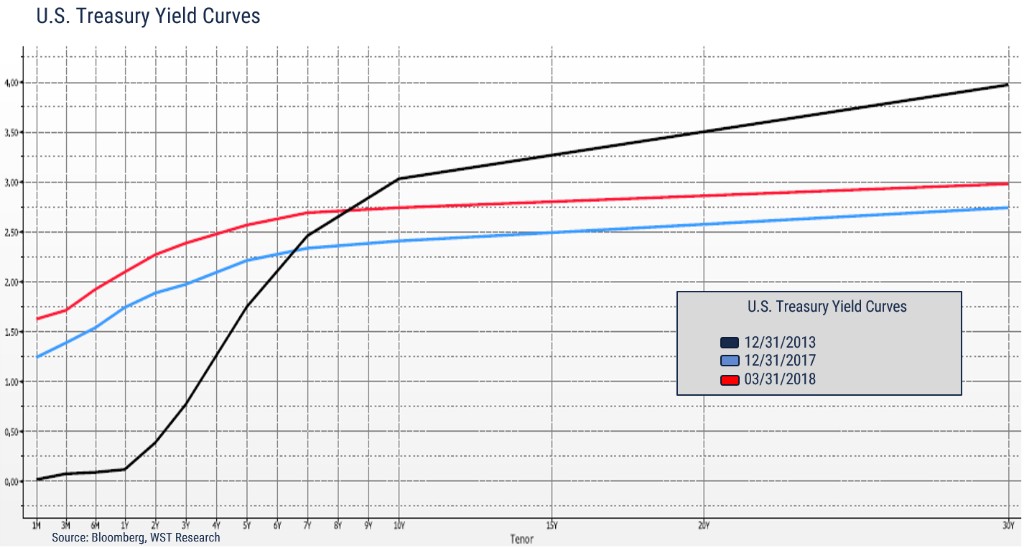

The following graph depicts the Treasury yield curve four years ago, three months ago, and at the end of March. The changes in interest rates and the shape of the yield curve over those time horizons are important to our perspectives on bonds now. At the end of 2013 the Fed was in maximum accommodation mode, but with short-term interest rates anchored near zero the yield curve was steep with the 10-year Treasury yielding over 3% and the 30-year Treasury 4%. Over the ensuing four years the yield curve flattened (the black line transitioned to the blue line on the graph below) because aggressive quantitative easing by the Fed pushed longer term yields down. Even as the fed funds rate rose from 0 to 1¼%, long-term yields remained low, we would suggest artificially low, due to QE. Inflation remained subdued and central bank purchases continued. The parallel shift upward in the yield curve over the past three months (blue line transitioning to red line on the graph) reflects Fed tightening driving rates higher on the short end of the curve, and higher inflation and the shrinking Fed balance sheet pushing rates up on the long end. Barring a recession, which we don’t foresee, each of these trends should continue, so we expect gradually rising rates for all maturities.

The good news for bond investors, and returning to the question of portfolio positioning, is that higher short-term rates allow us to invest in safe, liquid securities with reasonable yields and limited interest rate risk. For both taxable and non-taxable clients we continue to structure portfolios to take advantage of the steep section of the yield curve, out as far as 10 years, and to avoid long-term bonds, which offer meager incremental returns and more volatility. Where appropriate we have also added floating-rate bond funds to portfolios, which enjoy higher yields as interest rates rise, and are maintaining our allocations to international bonds.

Our twofold mission within the fixed income segment of accounts, capital preservation and income generation, remains unchanged. As rates rise our strategy will allow us to reinvest the proceeds of bond maturities in new securities with higher yields, and in the current environment we are better compensated while we wait. Shorter term, more liquid securities and funds also make us nimbler in the event an equity market correction creates an opportunity to buy stocks at cheaper levels.

Summary

The long, broad rally in risk assets was interrupted in the first quarter by concerns about the end of global quantitative easing, rising interest rates, a possible trade war, and worries about the tech sector. Those factors were enough to turn both stock and bond returns negative for the quarter, and we expect volatility to continue as each of those stories plays out over the rest of the year. With economic fundamentals so strong and no recession in sight we don’t expect a secular bear market anytime soon, but we remain cautious as the markets assess the challenging factors we’ve outlined. We’re taking the opportunity to review our clients’ expectations and objectives and, in many cases, have rebalanced portfolios back to neutral or slightly below our long-term risk allocation targets. As the second quarter gets underway we will continue to focus on ensuring that the mix of investments in each portfolio matches our clients’ needs.

As always, we sincerely appreciate the opportunity to serve you and look forward to a visit or conversation soon. For more market updates, visit the WST blog.

The WST Team

[1] Shalett, Lisa, “The Unpriced Inflation Agenda,” Morgan Stanley - On the Markets, April 2018.

[1] Schechner, Sam, “The Woman Who Is Reining In America’s Technology Giants,” Wall Street Journal, April 5, 2018

[2] Foroohar, Rana, “Echoes of Wall Street in Silicon Valley’s Grip On Money and Power,” Financial Times, July 3, 2017

[1] Sindreu, John, “As Europe Prospers, Stocks Fizzle,” Wall Street Journal, April 4, 2018

[2] Intercontinental Exchange (ICE) website. https://www.theice.com/fangplus

[1] Performance 2018 - S&P 500 Sectors & Industries, Yardeni Research, April 2018

[1] Swanson, Ana “The United States is Starting a Trade War With China, Now What?” New York Times, April 4, 2018

[2] “Blow For Blow” The Economist, April 4, 2018

Unless otherwise indicated, performance information for indices, funds and securities is sourced from FactSet as of March 31, 2018. This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC that are subject to change and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable, but cannot be guaranteed for accuracy. Some portions of this letter were written in conjunction and collaboration with Capital Markets Consultants Inc. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. It is made available on an "as-is" basis without warranty. There are no guarantees investment objectives will be met.

This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC and are subject to change from time to time, and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty. There are no guarantees investment objectives will be met.

The information contained herein has been obtained from sources believed to be reliable, but cannot be guaranteed for accuracy.

Market indices are unmanaged and do not reflect the deduction of fees or expenses. You cannot invest directly in an index such as these and the performance of an index does not represent the performance of any specific investment strategy. We consider an index to be a portfolio of securities whose composition and proportions are derived from a rules based model. Market indices are unmanaged and do not reflect the deduction of fees or expenses. You cannot invest directly in an index such as these and the performance of an index does not represent the performance of any specific investment strategy.

The S&P 500 Index is a market capitalization weighted index, including reinvestment of dividends and capital gains distributions that is generally considered representative of U.S. stock market. The Dow Jones Industrial Average (DJIA) is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange (NYSE) and the NASDAQ. The MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI ex USA Index is designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI EAFE Index is a stock market index that is designed to measure the equity market performance of developed markets outside of the U.S. & Canada. It is maintained by MSCI Barra, a provider of investment decision support tools; the EAFE acronym stands for Europe, Australasia and Far East. The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 845 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The Russell 2000 index measures the performance of the 2,000 smallest companies in the Russell 3000 index. The Bloomberg Barclays U.S. Aggregate Bond Index covers the USD-denominated, investment-grade, fixed-rate, taxable bond market of SEC-registered securities. The index includes bonds from the Treasury, Government-Related, Corporate, MBS, ABS, and CMBS sectors. The BofA Merrill Lynch U.S. High Yield Index tracks the performance of U.S. dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million. The BofA Merrill Lynch 1-3 US Year Treasury Index is an unmanaged index that tracks the performance of the direct sovereign debt of the U.S. Government having a maturity of at least one year and less than three years. The S&P/Citigroup International Treasury Bond ex-U.S. Index measures the performance of treasury bonds, with maturities greater than or equal to one year, issued by non-U.S. developed market countries.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.