Milestones Without Context? The 10-year Treasury Yield Hits 3%

On April 24th, 2018 - for the first time since January 3rd, 2014 and for only the fourth time since July 2011 - the US 10-year Treasury yield reached 3.0%. “Stock selloff pushes Dow down 400-plus points; 10-year Treasury yield touches 3% milestone,” read the Los Angeles Times headline. CNNMoney published an article entitled “Why everyone is stressing about the 10-year Treasury Yield,” positing “the most widely watched bond in America is close to a barrier that could cause trouble for the markets."

But was this so-called milestone in fact a milestone - truly significant in the context of market history - or simply clickbait? Either way, what are the implications for financial markets in the context of today?

Economic context of the 10-Year

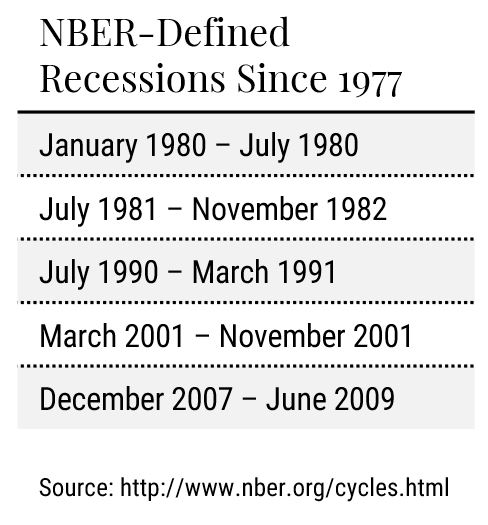

According to the National Bureau of Economic Research – a nonpartisan research outfit and the unofficial arbiter of U.S. business cycles - there have occurred five recessions over the past four decades. Over this same period, US nominal Gross Domestic Product (GDP) experienced annualized growth of 5.7%, and the S&P 500 Index experienced a cumulative price increase of 2,684% (approximately 8.6% annually). We feel safe in assuming this vast sample of US economic and equity market history encompasses the range of probable outcomes in the years ahead.

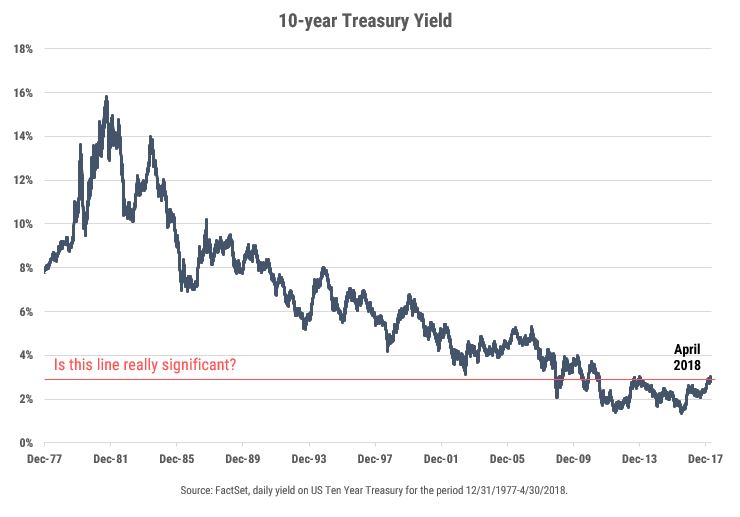

The below chart measures the 10-year Treasury yield over that time period (December 1977 – April 2018). The yield peaked at 15.84% on 9/30/1981 and experienced a low of 1.36% on 7/8/2016; the average over the period was 6.32%.

How do bond yields impact stock returns?

Rising interest rates at all levels matter to bond investors, but stock investors should not make the same assumptions.

For equity investors, the answer to the impact question is “it depends," and history provides no clear answer as to what it depends on. It is tempting and seemingly safe logic that at some level low long-term interest rates can reduce the appetite of investors seeking the higher expected return of stocks. We also feel safe in asserting that at some level high long-term interest rates can reduce the demand for goods and services, raising the likelihood of a business cycle downturn and lower corporate profits - critical inputs into the valuation of stocks. Clearly there is a balancing act at work, and we looked to analyze the behavior of the S&P 500 Index as a proxy for US equities against different interest rate trends.

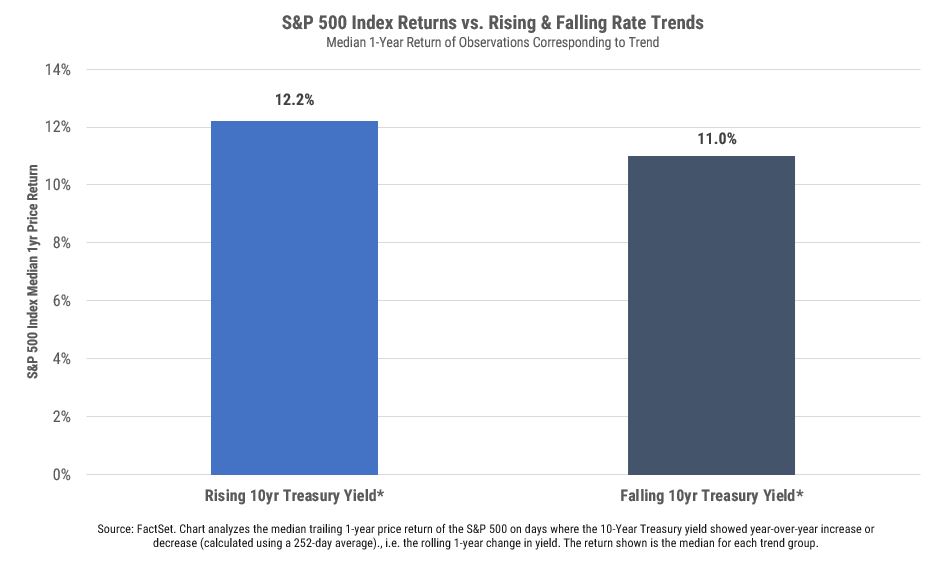

Rising vs. falling rates

The first chart below illustrates the daily S&P 500 Index 1-year price return on days we define as marked by “rising rate” or “falling rate” trends (based on whether the 10-year yield rose or fell year-over-year as of that day). During the forty-year period we focused on for this analysis, 43% of days were marked by a rising-rate trend versus 57% of days marked by a falling-rate trend.

The overall analysis would suggest that rising rate trends have historically been more supportive of S&P 500 price performance during the corresponding period.

Direction is not all

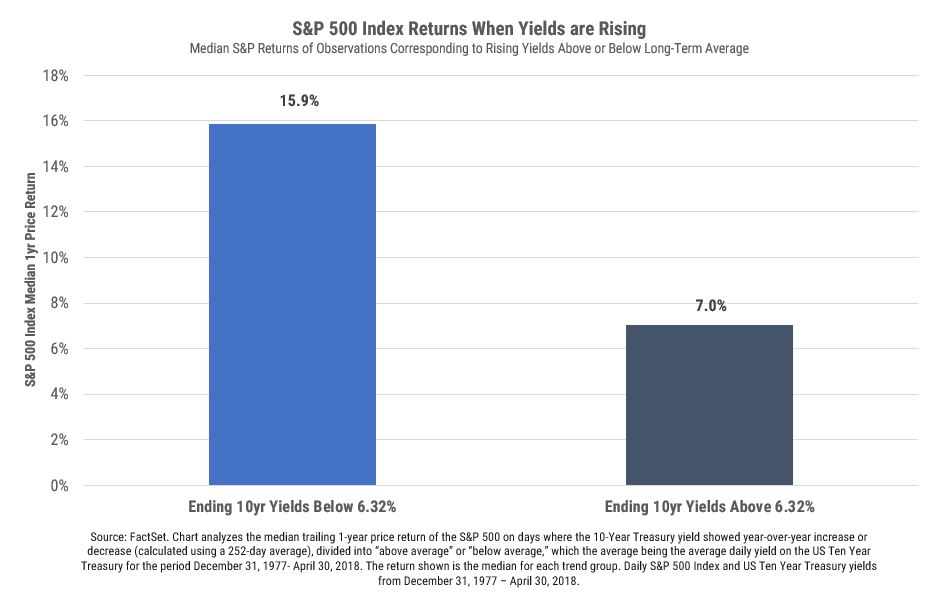

The notion that rising interest rates are supportive to equities seems fairly well-accepted among market-watchers, so the first chart simply supports broadly held "market wisdom." However, we believe an important corollary focuses on where that rising rate stands in relationship to long-term history. We assume there is meaningful difference between a yield rising to 1.51% off the long-term low of 1.36% and a yield inching from 15.75% to the long-term high of 15.84%.

The second chart focuses only on the rolling one-year periods since 1977 when the 10-year Treasury yield was rising. The bars represent the median one-year return in the S&P 500 Index when the rising 10-year Treasury yield was above or below that long-term (roughly 40-year) average yield of 6.32%. This analysis would indicate a favorable relationship between S&P price action and yields rising from a below-average rate, but the main takeaway is that at some level the interest rate does appear to matter – it would simply seem that 3% is not the “milestone” rate.

The Law of Round Numbers

As silly as it sounds, financial markets seem to love round, headline-grabbing numbers – whether it’s the Dow Jones Industrial Average at 24,000 or the 10-year Treasury yield at 3%. Headline appeal doesn’t give significance to 3% with regards to the 10-year, but that number is significant for other reasons – we believe it reflects a growing economy and rising corporate profits, both factors that have historically been positive for stock prices. With that observation in mind, we urge our clients to resist the headline hue and cry and focus on the long-term context.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.