WST 2Q 2018 Commentary

Financial markets responded to new and evolving challenges in the second quarter with higher volatility and wider dispersion of asset class returns. The ubiquitous optimism about steady, synchronized global economic growth at the end of 2017 is being displaced by fears of a trade war and concerns about interest rates and corporate earnings, and economists are peering over the horizon to see the convergence of the fading effects of last year’s tax and infrastructure bills and the end of Fed stimulus.

The strong domestic economy continues to support corporate earnings and stock prices for now, but growth is softening outside of the U.S. Inflationary pressures are increasing for the first time in a decade as labor markets tighten and energy prices rise. Higher inflation increases the likelihood that the Federal Reserve will continue to raise rates this year and next, a path which would be consistent with their guidance but potentially precarious in the context of the challenges we outline in this letter. The tone at the end of the quarter was decisively “risk off.” Credit spreads widened and Treasury yields declined as investors opted for the relative safety of U.S. government bonds over riskier corporate debt, and equity mutual funds saw redemptions of over $30 billion during the week ended June 29, according to Reuters.[1] As we enter the second half of the year our core views expressed last quarter remain intact. At this late stage in the economic cycle, with challenges mounting and valuations high across most asset classes, we are relatively defensive in our portfolio positioning.

Follow this link to access and download a printer-friendly version of our commentary.

The most worrisome evolution over the past three months was the deteriorating trade picture. As we write this letter the July 6 inception date for the first round of U.S. tariffs on Chinese products is upon us. The initial volley will begin with the imposition of 25% tariffs on $34 billion of Chinese imports to the U.S., and China will likely retaliate with their own tariffs on an equal amount of U.S. products. The risk of a rapid escalation from there has the markets on edge. China has warned it won’t bend to U.S. pressure, and the Trump administration appears determined not to back down. U.S. trade representative Robert Lighthizer is under instructions to identify two more tranches of $200 billion each of foreign products for follow-on tariffs if China and our other trade partners don’t meet U.S. demands. During the 2016 presidential campaign Trump promised to withdraw from or renegotiate the U.S. role in various trade arrangements including the World Trade Organization (WTO), North America Free Trade Agreement (NAFTA), and the Transpacific Partnership (TPP), with the dual aims of reducing our massive trade deficit and increasing our competitiveness with China. With tax reform completed and the infrastructure bill behind him, trade policy is now the President's top priority. The stakes are rising as the administration shifts from targeted policies aimed at specific imbalances in products like washing machines and solar panels to the much broader array of products to be taxed under the current plan. Globalization played a central role in the recovery from the financial crisis and subsequent boom in the global economy and markets. Regardless of one's politics or opinions we can all recognize that a prolonged trade war could trigger a recession with extensive economic casualties on all sides.

So far, the consensus remains that the initial economic and market impact from the Trump’s trade policy will be nominal, shaving less than one percent off global GDP, but Morgan Stanley's Lisa Shalett fears that the current benign outlook doesn't sufficiently capture the broader context or all of the risks associated with an escalation in tension. She points out that while the initial round of planned tariffs impact only 5% of the $2.5 trillion in U.S. imports, subsequent threats include not just Chinese goods but also European and Japanese cars and cover over 20% of U.S. imports. Our trade partners have begun to fight back. The EU has targeted $3.2 billion of U.S. exports including motorcycles, jeans, and liquor, which could be just a fraction of the products impacted if the conflict escalates. Shalett also warns that over a third of U.S. exports are agricultural and energy-related commodities for which foreign buyers can easily find alternate supplies.[2]

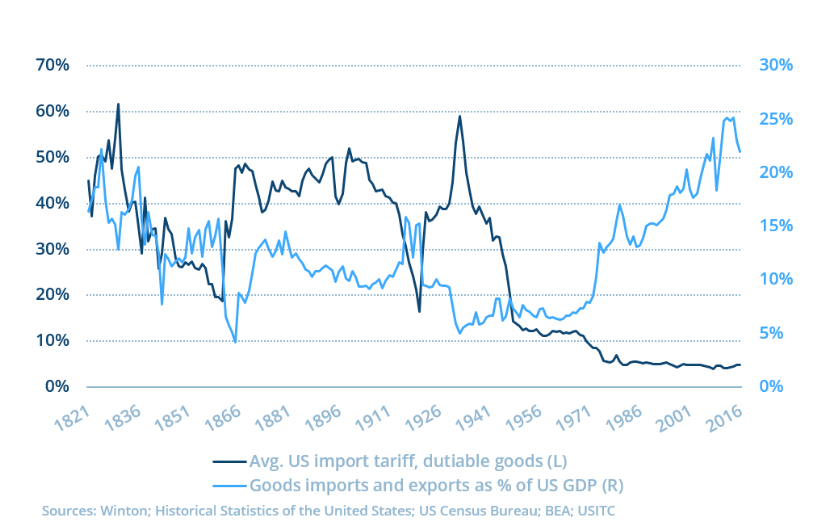

As worrisome as the threat of direct tariffs is to certain industries, the biggest risk of a prolonged trade war is damage to global supply chains. According to the Peterson Institute for International Economics, approximately two thirds of all goods traded globally are produced through or as part of global supply chains, and the proportion is even higher in the high-tech sector.[3] If intermediate products are subject to tariffs as they enter the U.S. they become more expensive as inputs in the U.S. economy, and the tariff lists include many inputs and intermediate goods used in American production. Looking specifically at the administration’s targeted sectors, trade experts point out that most U.S. imports from China in the tech sector come from affiliates of multinational firms rather than Chinese domestic firms. Taxes on those products will decrease American competitiveness, so while the tariffs are intended to penalize Chinese firms that have improperly obtained American technology they may in fact be more onerous on U.S. tech companies. Also, many U.S. imports from China contain value created in other countries, including American intellectual property. For example, the Peterson Institute points out that some of our biggest companies such as Apple and Nike focus on marketing, design and innovation in the U.S. but outsource parts of the physical production process to countries and regions where production costs are lower. Some view that fact negatively, but the global supply chain "reduces costs, raises productivity, expands the global market share of U.S. firms, and allows the United States to focus on what it does best: innovating, researching, and designing the cutting-edge goods and services of the future.”[4] As the chart below reveals, global commerce has boomed since World War II as decades of low tariffs and free trade allowed markets to allocate resources efficiently and companies to run their design, production and distribution processes efficiently and profitability. A long trade war would be a major setback to global growth.

Economic Overview

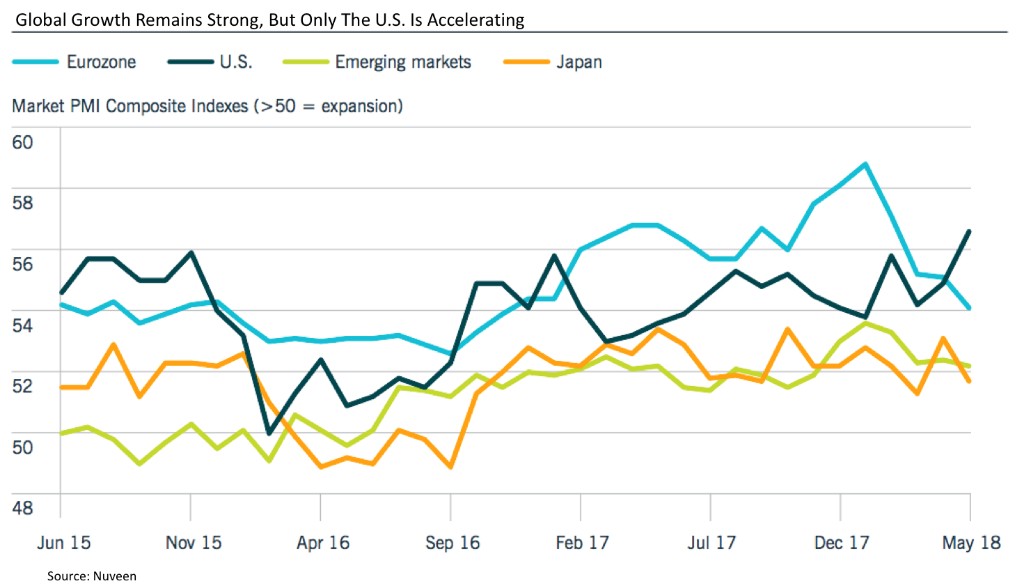

While it may be premature to mention the possibility of a recession, many key indicators suggest that the synchronized growth of the global economy has peaked. As the chart below demonstrates the U.S. is the only major economy enjoying accelerating growth as the third quarter begins, and even our economic cycle is mature. Tax reform has improved corporate profits and lowered taxes for most families, but the pick-up in domestic GDP growth to 4% annual pace in the second quarter more likely reflects growth being pulled forward rather than a sustainable acceleration. Trade policy is the wildcard, and the next economic downturn could come sooner than expected if the situation deteriorates.

Already the Eurozone and emerging markets are facing strong new headwinds. Growth in Europe remains a bit above the long-term trend, but the data are softening. Higher oil prices are a factor, but the slowdown is probably a return to normalcy as the excitement surrounding the prospect of widespread European reform and economic integration inspired by the election of Emmanuel Macron in France is dampened by an increasingly unstable political picture throughout Europe. President Macron met with German Chancellor Merkel in June with little success in their efforts to chart a path forward for the EU, and the emerging reality is that the economic and political interests of the EU members don't align well. Germany is the economic power of the region and Merkel understandably resists allowing Germany to be dictated to by the Union's weaker members. Italy’s Mateo Salvini has raised the level of discord over immigration in Europe and the sovereignty of the EU as his disdain for Merkel and promises of lower taxes and more social spending are mirrored by “nativist” politicians in other countries. Dissatisfaction with EU policies are leading some in Italy to advocate an “Italeave” or “Quitaly” to go along with Britain’s Brexit.

The emerging market economies have the dubious distinction of falling in just six months from the biggest positive surprise of 2017 to the biggest under-performers in 2018. Fears of a trade war hit China hard and raised concerns about other trade-dependent countries including Russia, Brazil, and South Korea. Trade concerns also triggered a strong rally in the dollar during the second quarter, creating a ripple effect throughout emerging markets with a particularly negative impact on countries with dollar-denominated debt. As the dollar becomes more valuable relative to those other currencies that debt becomes more expensive to service.

As the challenges facing the global economy become more pronounced, the risk increases that the Fed will overshoot in its transition to higher policy rates. The Fed's preferred measure of inflation, the core personal consumption expenditures price index (PCE), was up 2% from a year ago in May, matching the Fed’s inflation target for the first time in six years. Recent FOMC minutes confirm that their policy map aims to raise rates over the next year to a “neutral level” which no longer stimulates faster growth, ending a decade of unprecedented support. In speeches and other comments committee members have discussed concerns around trade tensions, emerging markets instability, and political uncertainty in Europe, but for now those risks are not softening their outlook.

Equity Market Overview

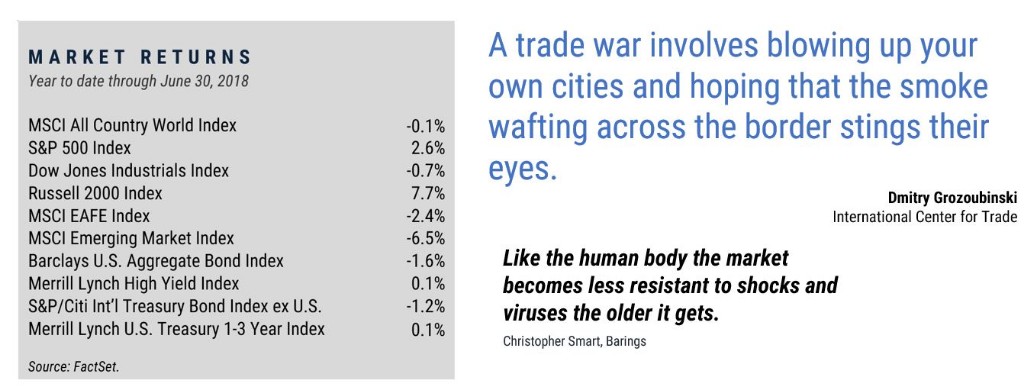

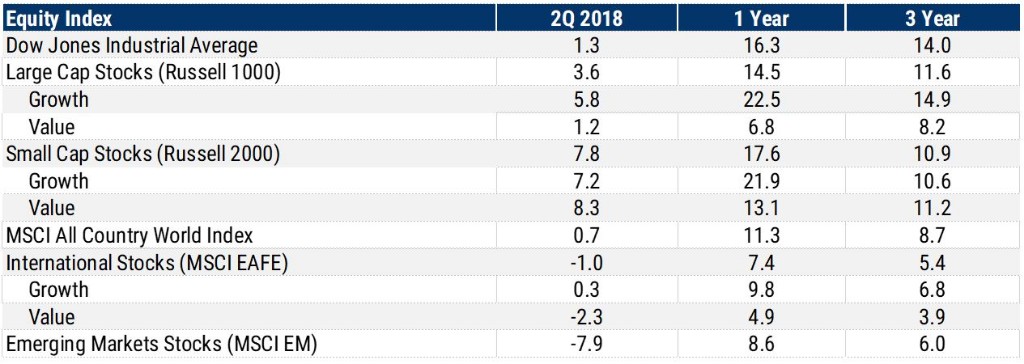

Global stocks ended the quarter at the same level they began the year, but that flat performance belies renewed volatility and big differences between the best and worst performing sectors. U.S. equity indexes posted positive returns but international indexes were generally negative. The S&P 500 generated a 3.4% return for the quarter while the MSCI EAFE index was down 1.0%. The Russell 2000 small cap index enjoyed a 7.8% return and neared its all-time high while emerging markets stocks suffered a difficult quarter, falling nearly 8%. The Dow Jones Industrial Average shed more than 1,000 points or 4.1% in the last three weeks of the quarter, pulling that index into negative territory for the year. The Dow is considered more sensitive to trade policy than the other broad indexes because its component companies tend to depend more upon the global supply chain and generate more revenue overseas than the average U.S. company. Overall the global equity market as measured by the Bloomberg World Stock Market Capitalization Index has shed almost $10 trillion in value since peaking in late January.

The dominance of U.S. equities over international equities remains an important market theme. Since 2010, the S&P 500 has generated a cumulative return of 183% while the MSCI All-Country World Index ex. U.S. has gained only 83%. Last year it appeared the tide was turning as international stocks generally outperformed their U.S. counterparts, but in the first half of 2018 the numbers swung back to U.S. outperformance with returns driven by domestic economic growth, strong corporate profits, and business-friendly tax and regulatory policies. S&P 500 earnings rose 25% year-over-year in the first quarter, the highest earnings growth rate since the third quarter of 2010, and nearly 80% of S&P 500 companies reported a positive earnings surprise versus Wall Street estimates, the highest percentage since FactSet began tracking this metric in 2008.

The possible downside of all of the good news is that the exceptionally strong earnings performance of American companies is largely baked into stock prices now and estimates of future earnings remain very optimistic. U.S. equities are priced for perfection, and earnings projections have not been adjusted to reflect any impact of a trade war. According to Yardeni Research, Wall Street expects 2019 S&P 500 earnings to top $177.00 per share, a 9.8% increase over 2018.[1] If the trade conflict is more damaging to the economy and earnings than the current sanguine outlook expects, U.S. stocks will be vulnerable.

As we mentioned above, trade concerns are weighing especially heavily on international equity markets. Fears of a trade war, the strengthening dollar, and rising U.S. interest rates have hit stocks in China and other emerging markets hard. The Shanghai Composite index is officially in bear market territory after falling more than 20% since its January 24th high. Country-specific developments also played a role in some emerging markets. For example, labor unrest, anemic economic growth, and political uncertainties contributed to the MSCI Brazil index’s slide of more than 26% in the quarter.

Faltering growth and political uncertainty in developed international markets drove renewed volatility as investors fear that the stronger mandate for anti-establishment, anti-EU policies threaten the viability of the union. Somewhat surprisingly the final data revisions revealed that the Japanese economy shrank in the first quarter at an annualized rate of 0.6%, marking the end of eight straight quarters of economic expansion for the world’s third largest economy. That was the longest period of sustained growth there since 1989 and is unlikely to be repeated in the near future. With an unemployment rate of just 2.5% and a rapidly aging workforce, Japan is simply running out of workers.

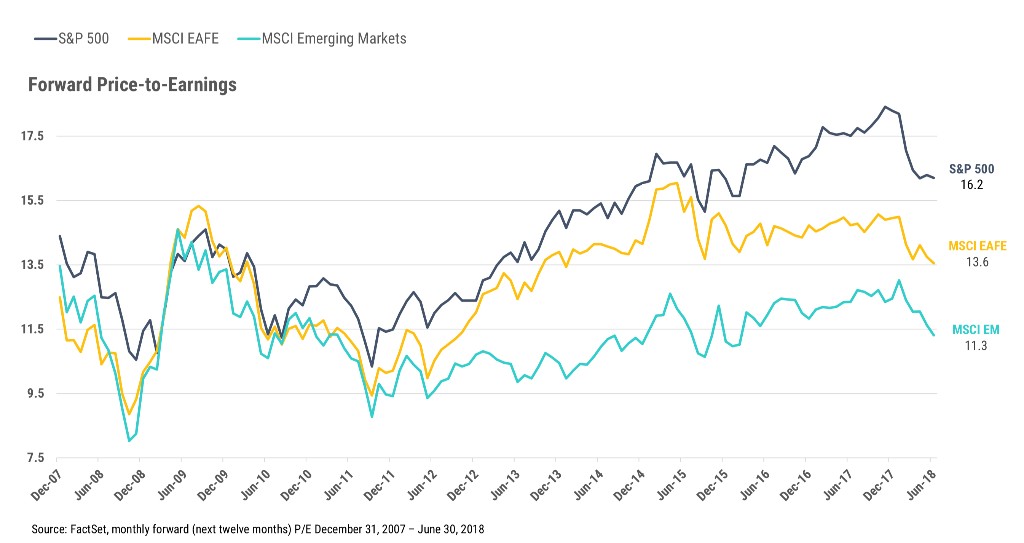

The good news for international equity investors is that while the "Goldilocks" macro-economic environment of 2017 has dissipated, other fundamental catalysts for those markets remain in place. As the table below demonstrates valuations remain relatively attractive for developed market equities and extremely attractive for emerging market stocks. Rising incomes and technological innovation continue to spur consumption across Asia, and corporate profit growth remains healthy despite the recent slowdown. IMF forecasts predict a widening long-term growth differential between emerging economies and developed markets, and we continue to believe that emerging market equities will eventually enter a of a cycle of outperformance relative to developed markets. Idiosyncratic risks unique to each individual country impact the economies of emerging markets including Brazil, Mexico, Russia, etc., but despite the recent data the longer-term growth trends and macroeconomic fundamentals in each have improved in recent years. We continue to maintain our allocations to non-U.S. equities both for diversification purposes and to position portfolios to take advantage of the long-term trends.

Bond Market Overview

Bonds remained under pressure in the second quarter due to monetary tightening, strong jobs data and rising inflation, and those headwinds will likely continue in the second half of the year. As we discussed last quarter we’ve reached an inflection point in the interest rate cycle where global central banks are normalizing monetary policy after a decade of stimulus. Central bankers and fixed income investors are in uncharted territory as the markets sort out the timing and implications of the policy shift, so uncertainty and volatility are high.

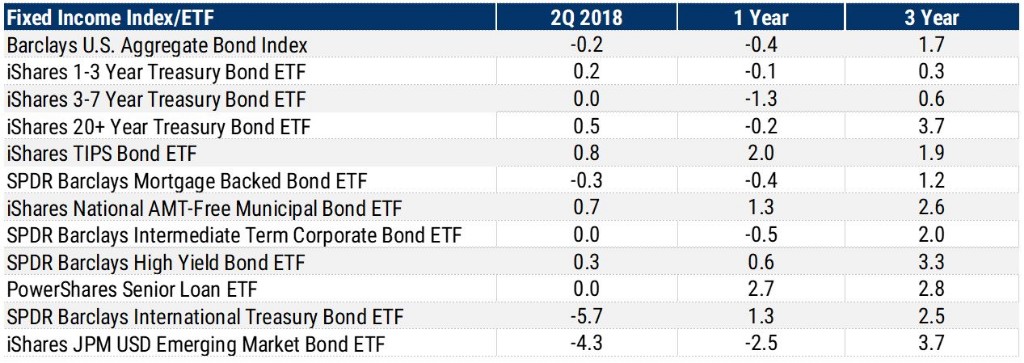

The Barclays U.S. Aggregate Bond Index generated a slightly negative return in the quarter and is now down 1.6% year-to-date. The 10-year Treasury broke through the symbolically important 3% level in May before retreating on trade fears, but inflation and economic data continue to put upward pressure on rates. Given this backdrop, money market, high yield, floating rate and short-term bonds have performed relatively well while emerging market debt, investment grade corporates and U.S. Treasuries have lagged. In the tax-free municipal bond market high-grade issues have produced slightly negative year-to-date returns as rates drifted higher. Municipal-to-Treasury yield ratios have increased so municipals are relatively inexpensive and appear more attractive. The supply of new issue tax free bonds is down following the record number of financings completed in December 2017 as municipalities raced to get those deals done before the new tax law took effect.

The most notable performance issues in the fixed income markets during the quarter were widening corporate bond spreads and the flattening yield curve, both of which reflect diminished investor appetite for risk. The positive economic environment in 2017 supported spread compression as investors willingly accepted smaller incremental returns on corporate bonds versus government bonds, but the political and economic risks we've outlined above have the market rethinking that perspective. The narrow spreads at the end of last year likely represent the low-water mark for the current credit cycle.

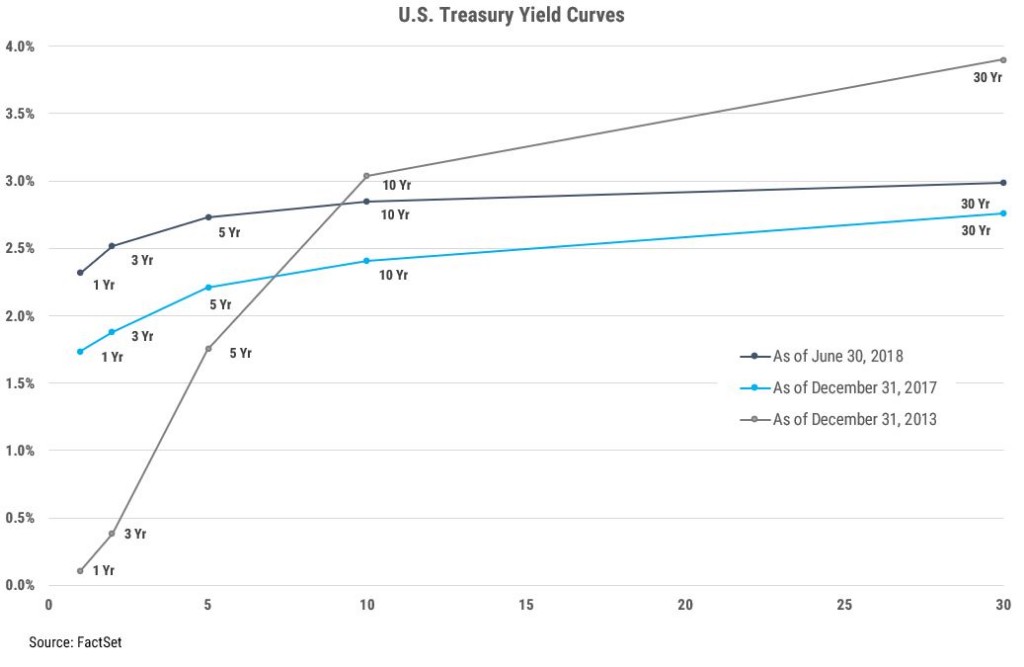

More complicated and important is the flattening of the Treasury yield curve. The difference between short and long-term Treasury bond yields is an important indicator of sentiment about economic growth and inflation. In normal times investors demand more compensation for investing in longer term bonds to compensate them for inflation risk. If market expectations about growth and inflation decline, long term rates decline as well. An inverted yield curve, where short-term rates are higher than long-term rates, has historically been predictive of a recession, and four of the last five recessions have been preceded by an inverted yield curve. A flattening yield curve is analogous to a falling barometer; it warns that stormy economic weather lies ahead but leaves much uncertainty about the timing and magnitude of the changes to come. As the second quarter ended the difference between the two-year and 30-year Treasury yields fell to 32 basis points, the smallest gap since 2007.

The toughest question facing economists and bond investors now is how to juxtapose the Fed’s plan for normalizing rate policy with the current Treasury yield curve. The Fed plan as expressed through the dot plot calls for the Fed Funds rate to reach the 3.0-3.25% range in 2019 and as high as 3.5% in 2020, levels significantly above the current 10-year Treasury yield. Those plans either invert the curve or force long-term yields higher than current expectations, and neither of those scenarios would be good news for the economy and markets. So, while the Fed continues to communicate its intent to raise rates at a “moderate” pace, the dot plot and the evolving narrative about faster inflation have the market worried that the Fed will overshoot at a moment when the economy is vulnerable to the impact of trade policy. The following chart reveals the dynamics of the Treasury yield curve this year: higher short rates due to Fed tightening, higher long rates due to concern about inflation, and a flattening curve due to skepticism about the durability of the global economy.

Given the upward pressure that Fed policy is putting on rates and the lack of meaningful incremental return associated with longer maturities, we continue to position bond portfolios conservatively with biases to short duration and credit sensitive issues. Where appropriate we’ve continued to add floating rate bond funds to portfolios to take advantage of higher short-term yields. Our objectives within bond portfolios are capital preservation and income generation, and for the time being we’re emphasizing safety of principal in an effort to position portfolios to take advantage of higher yields later.

Summary

In summary we remain cautious on our outlook for the global investment markets. The fundamental economic environment remains positive, but slower growth, higher inflation, tighter monetary policy, and geopolitical and trade uncertainty together have increased the risk that the long global expansion has reached a cyclical peak. With risks rising we are positioning portfolios a bit more conservatively on the margin. Plenty of opportunities for positive returns remain; value stocks in the U.S. are reasonably priced and international markets offer attractive potential despite their challenges, especially in emerging markets. Exposure to risk assets is necessary for achieving long-term return objectives, but mitigating downside risk is also important. We don’t believe a recession or bear market are imminent, but we do expect lower returns than investors have enjoyed in recent years. Each individual client or institution has unique needs, and our most important job is to make sure the allocation of risk and return potential in every portfolio matches those needs.

On an administrative note, many of you are aware that WST is in the midst of a major technology transition and implementation. The changes are designed to enhance our internal processes and more importantly to improve our clients’ experience and access to information. We hope to have the implementation complete by the end of the third quarter and look forward to more and better communication and reporting. If you have any questions or comments during the transition please don't hesitate to let us know.

As always, we sincerely appreciate the opportunity to serve you and look forward to a visit or conversation soon!

The WST Team

[1] “Equity Funds Lose $30 Billion As Investors Flee U.S. and EM Stocks: BAML,” Reuters, June 2018

[2] Shallett, Lisa. Trade Tensions Intensify, On The Markets, Morgan Stanley, July 2018

[3] Lovely, Mary and Liang, Yang. Trump Tariffs Harm U.S. Tech Competitiveness, Peterson Institute for International Economics, May 2018.

[4] Ibid.

[1] https://www.yardeni.com/pub/yriearningsforecast.pdf

Unless otherwise indicated, performance information for indices, funds and securities as well as various economic data points are sourced from FactSet as of June 30, 2018. This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC that are subject to change and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable, but cannot be guaranteed for accuracy. Some portions of this letter were written in conjunction and collaboration with Capital Markets Consultants Inc. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. It is made available on an "as-is" basis without warranty. There are no guarantees investment objectives will be met.

This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC and are subject to change from time to time, and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty. There are no guarantees investment objectives will be met.

The information contained herein has been obtained from sources believed to be reliable, but cannot be guaranteed for accuracy.

Market indices are unmanaged and do not reflect the deduction of fees or expenses. You cannot invest directly in an index such as these and the performance of an index does not represent the performance of any specific investment strategy. We consider an index to be a portfolio of securities whose composition and proportions are derived from a rules based model. Market indices are unmanaged and do not reflect the deduction of fees or expenses. You cannot invest directly in an index such as these and the performance of an index does not represent the performance of any specific investment strategy.

The S&P 500 Index is a market capitalization weighted index, including reinvestment of dividends and capital gains distributions that is generally considered representative of U.S. stock market. The Dow Jones Industrial Average (DJIA) is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange (NYSE) and the NASDAQ. The MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI ex USA Index is designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI EAFE Index is a stock market index that is designed to measure the equity market performance of developed markets outside of the U.S. & Canada. It is maintained by MSCI Barra, a provider of investment decision support tools; the EAFE acronym stands for Europe, Australasia and Far East. The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 845 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The Russell 2000 index measures the performance of the 2,000 smallest companies in the Russell 3000 index. The Bloomberg Barclays U.S. Aggregate Bond Index covers the USD-denominated, investment-grade, fixed-rate, taxable bond market of SEC-registered securities. The index includes bonds from the Treasury, Government-Related, Corporate, MBS, ABS, and CMBS sectors. The BofA Merrill Lynch U.S. High Yield Index tracks the performance of U.S. dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million. The BofA Merrill Lynch 1-3 US Year Treasury Index is an unmanaged index that tracks the performance of the direct sovereign debt of the U.S. Government having a maturity of at least one year and less than three years. The S&P/Citigroup International Treasury Bond ex-U.S. Index measures the performance of treasury bonds, with maturities greater than or equal to one year, issued by non-U.S. developed market countries.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.