Money for Nothing?

Since 1973, the National Federation of Independent Business (NFIB) - the largest small business association in the country – has conducted a monthly survey of its members. The current monthly report is a based on surveying a total of 10,000 small business members, and it covers a variety of topics important to small business owners; all said, it can be a useful insight into what trends are rising and falling in a critical segment of our economy. What the NFIB survey is suggesting about the labor market, and how those suggestions square with Fed action, is the subject of this letter.

Among investors, one of the more hotly debated economic topics is how well behaved inflation data is, as we begin the ninth year of the current economic expansion. While, according to the National Bureau of Economic Research (NBER), this current expansion would rank as the third-longest expansion since 1900, it also is the slowest expansion during the post-WWII period. Throw in low energy prices and the “Amazon” effect on consumer prices and this low-inflation period seems perfectly logical.

However, the true headline-seizing dialogue has been around continued improvement in the labor market without accompanying increases in wage gains. Even Federal Reserve Chairwoman Janet Yellen responded in a recent Congressional testimony that poor labor productivity is primarily responsible for low wage gains. But to quote another D.C. insider, “It depends on what your definition of ‘is’ is.”

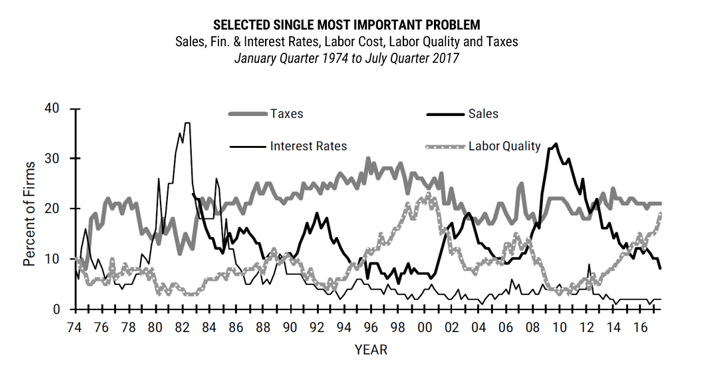

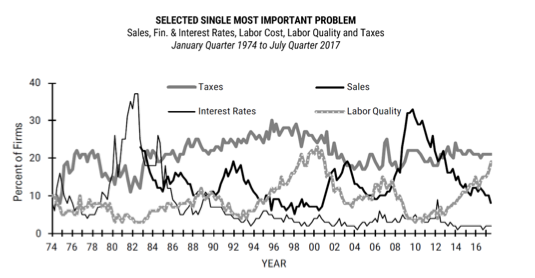

Aggregated economic data is squarely in the bucket of a generalization that rarely, if ever, describes what really is happening at ground level. For example, one of the survey questions in the July NFIB survey queried small business owners as to their single most important business problem among ten categories. The graph below illustrates how respondents answered in four of these categories. Encouragement can be found in the trend for sales, which was cited as the most pressing issue by the lowest percentage of respondents in 15 years. On the other hand, labor quality is now the single most important business problem for 19% of respondents, representing a 15-year high. Additionally, 35% of all owners reporting job openings could not fill them in the current period, which is the highest percentage since November 2001. Of those companies reporting hiring or trying to hire, 87% reported few/no qualified applicants for the positions they were trying to fill.

Aggregated economic data is squarely in the bucket of a generalization that rarely, if ever, describes what really is happening at ground level. For example, one of the survey questions in the July NFIB survey queried small business owners as to their single most important business problem among ten categories. The graph below illustrates how respondents answered in four of these categories. Encouragement can be found in the trend for sales, which was cited as the most pressing issue by the lowest percentage of respondents in 15 years. On the other hand, labor quality is now the single most important business problem for 19% of respondents, representing a 15-year high. Additionally, 35% of all owners reporting job openings could not fill them in the current period, which is the highest percentage since November 2001. Of those companies reporting hiring or trying to hire, 87% reported few/no qualified applicants for the positions they were trying to fill.

Source: NFIB July 2017 survey, http://www.nfib.com/surveys/small-business-economic-trends/

Source: NFIB July 2017 survey, http://www.nfib.com/surveys/small-business-economic-trends/

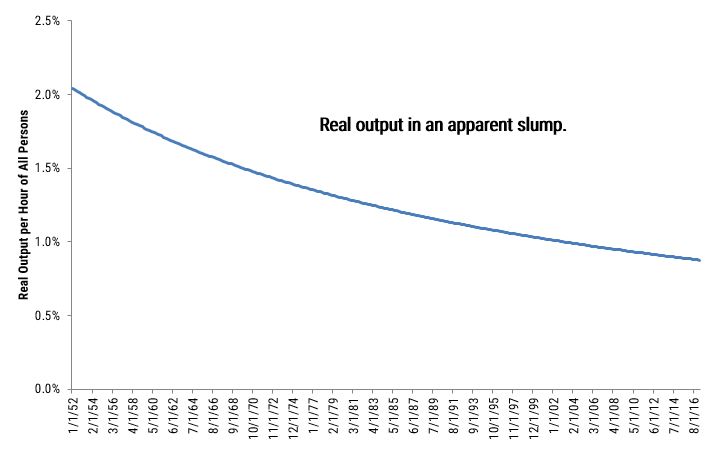

Janet Yellen was accurate when talking about poor productivity, but this problem is not a new one. The graph below, from FRED (Federal Reserve Economic Data), illustrates the five-year rolling annualized growth of productivity since 1952. At the current five-year annualized rate of less than 0.9% per year, we are at all-time lows. In this context, it would appear curious labor productivity would be the primary cause of low wage growth over recent periods.

Source: Federal Reserve Economic Data, citing US Bureau of Labor Statistics. Rolling 5-year calculation performed by WST using quarterly data. Retrieved from fred.stlousfed.org, on August 11, 2017.

Source: Federal Reserve Economic Data, citing US Bureau of Labor Statistics. Rolling 5-year calculation performed by WST using quarterly data. Retrieved from fred.stlousfed.org, on August 11, 2017.

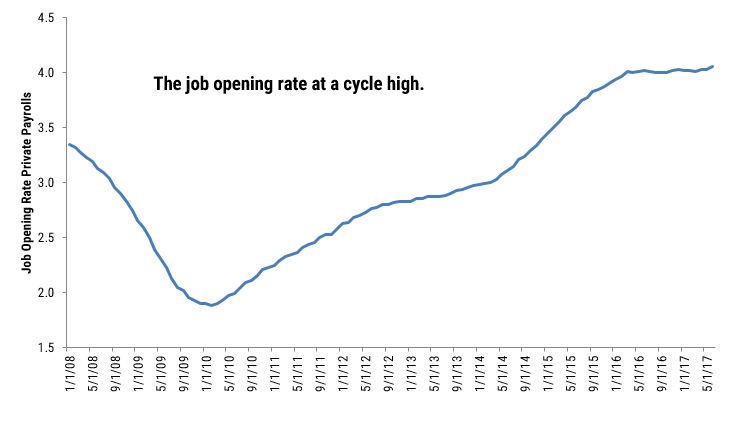

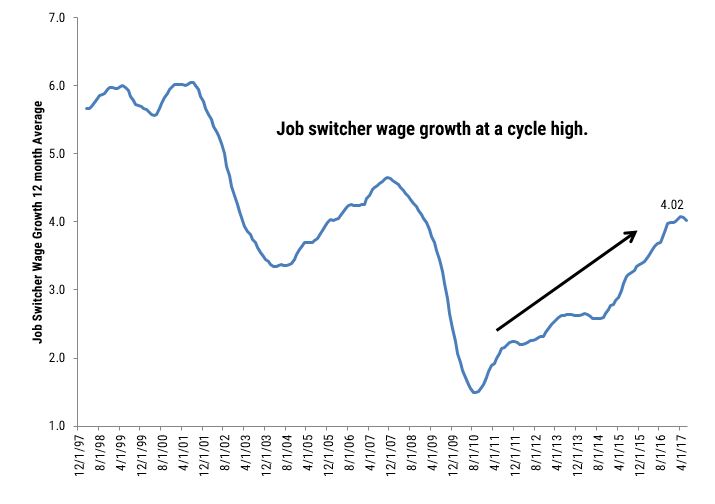

Could it be wage growth is being not being measured accurately? In the NFIB survey, reports of higher worker compensation continues to be strong, an indicator that is logically consistent with historically tight labor markets. The final two graphs, from the US Bureau of Labor Statistics, appear also to support the NFIB data.

The first chart shows the job opening rate clearly at a cycle high which suggests plenty of demand for labor:

Source: US Bureau of Labor Statistics, https://www.bls.gov/jlt/. Retrieved August 11, 2017.

Source: US Bureau of Labor Statistics, https://www.bls.gov/jlt/. Retrieved August 11, 2017.

Next is a 12-month moving average of job switchers - presumably a number driven by those in search of better quality, higher-paying jobs. High skill job wage growth seems to suggest that better wage is a driver of the job switcher data; high skill wage growth was 3.7% in June and at a much higher rate than 2.7% for low skilled jobs. High skill wage growth has been at 3.0% or higher for 29 straight months and 3.5% or higher for the past 11 months.

Source: US Bureau of Labor Statistics, https://www.bls.gov/jlt/. Retrieved August 11, 2017.

Source: US Bureau of Labor Statistics, https://www.bls.gov/jlt/. Retrieved August 11, 2017.

We’ll have to leave it to the Fed to discern whether employers are paying money for nothing, as measured by productivity data. However, from our perspective, the data supports the notion that jobs are being left unfilled in high numbers and real wage growth is attractive when worker skills are being matched by employer demand. The NIFB survey on sales and our own analysis of sales data suggests wage growth is following the improvement in company fundamentals.

For us as investors in the quarters ahead, these observations boil down to whether this trend remains supportive of further gains in stocks, and if (as it appears) the data supports our more cautious stance on bonds.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.