US Labor Market: A Bright Star, But Is It Burning Too Hot?

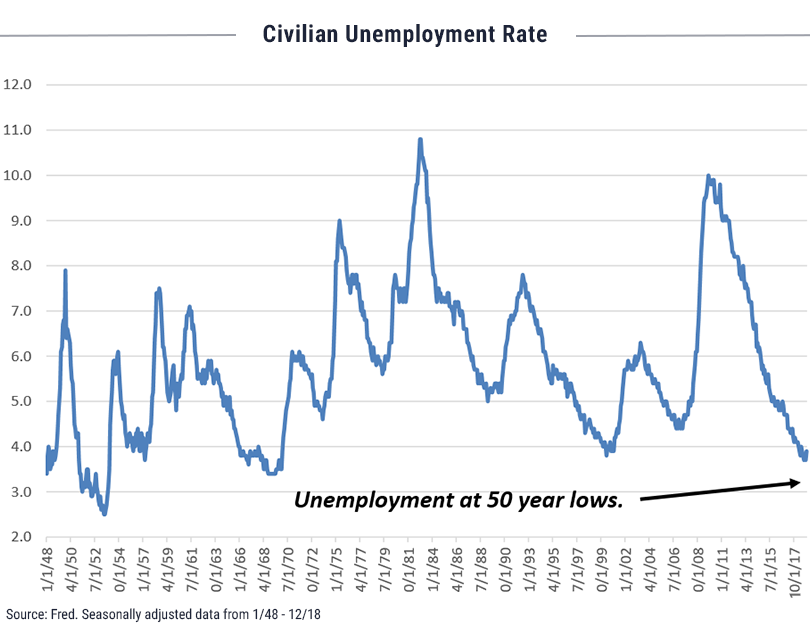

Buried, if not lost, in the recent hubbub around capital markets, Federal Reserve action and the US China-Trade War is an American economic milestone achieved at the end of 2018. For the first time in history the American economy surpassed 150,000,000 jobs, a statistic accented by solid growth (+2.6 million) in the last twelve months. This growth was sufficient to keep the unemployment rate below 4% in eight of twelve months during the year. While overall highly positive for the US economy, the condition of the labor market does drive mixed impacts across other metrics of economic health, including wage growth, productivity, inflation and interest rates.

Record-Breaking Levels

The labor market is arguably the brightest star in the current economic expansion, which - in the summer of 2019 - will become the longest in duration since the National Bureau of Economic Research began publishing the data. Such a lengthy period of uninterrupted growth has produced some predictably favorable trends in the job market; unemployment is at record lows and the number of job openings exceeds the number of hires being made.

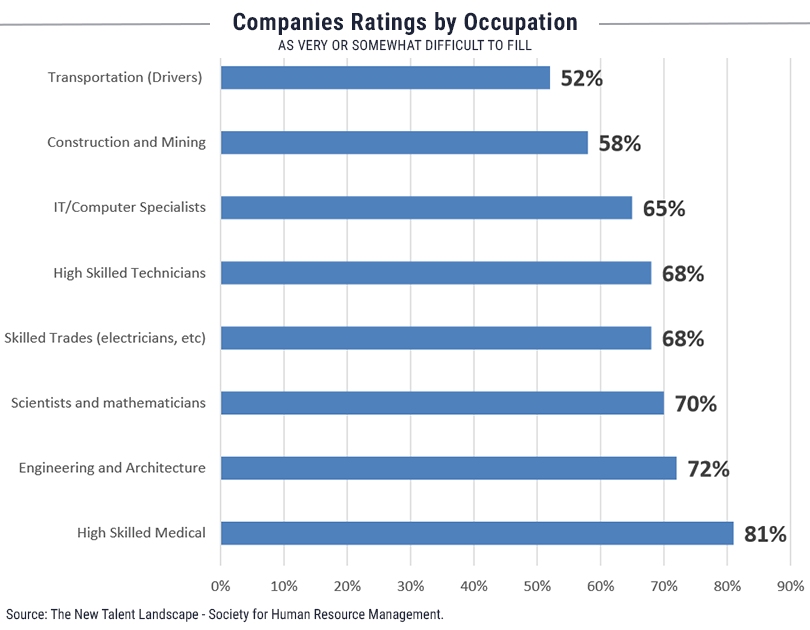

The flipside of this strength and record-high levels of job openings, however, is a growing shortage of skilled labor. Survey-based data supports the sense that the US labor market is extremely tight. As reported in the monthly Economic Trends report issued by the National Federation of Independent Business (NFIB), twenty-three percent of surveyed small business owners cited as their “Single Most Important Business Problem” the difficulty of finding qualified workers; this figure fell between November and December but was still just 2% below the record-high level recorded in November. According to the study, thirty-nine percent of survey participants reported job openings they would not fill in the current period. This figure represented a five-point rise and a new record high, according to NFIB.

“Twenty-three percent…selected “finding qualified labor” as their top business problem, more than cited taxes or regulations as their top challenge.” - NFIB Small Business Economic Trends , December 2018

Tightness in supply of skilled labor is now evident across many industries - especially those which require a highly educated, technical and trade-oriented workforce.

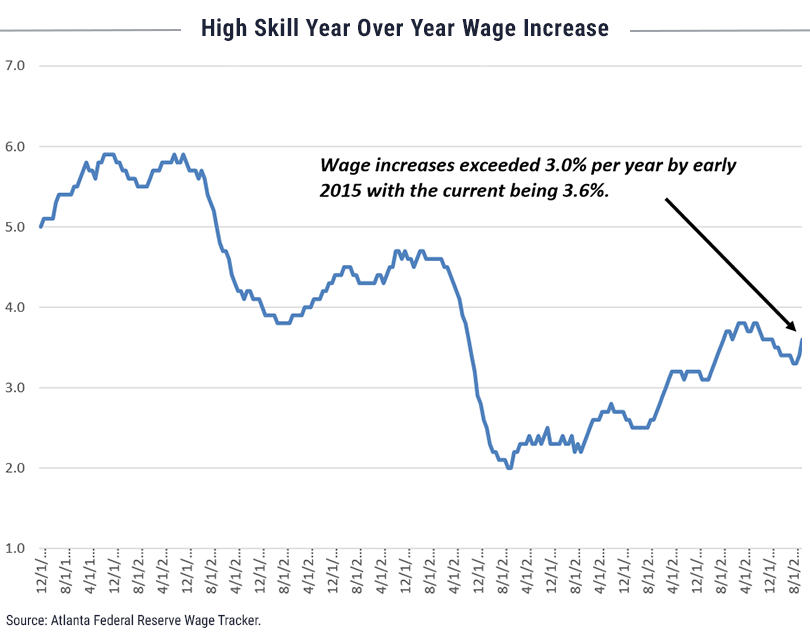

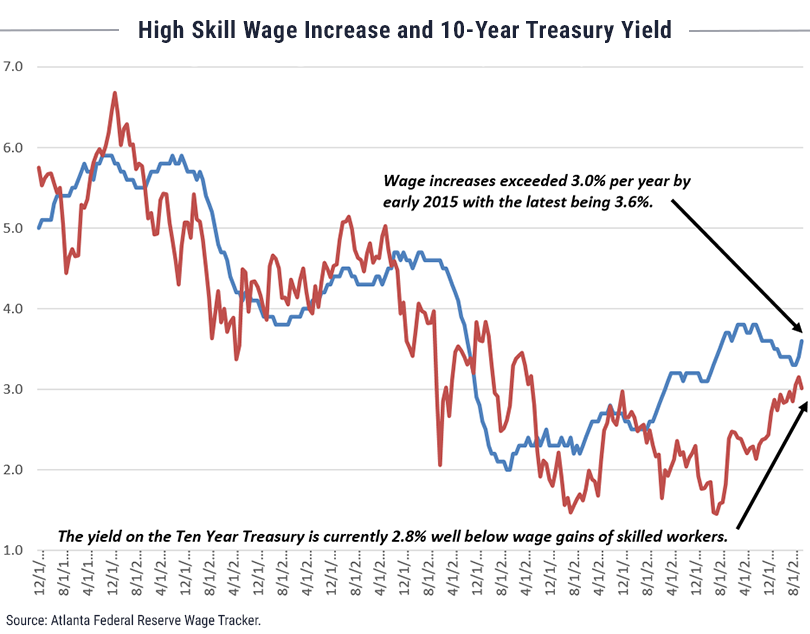

Rising Wages

Rising wages are a natural outcome when the demand for labor exceeds the supply. Since 2015, year-over-year wage increases have exceeded 3.0% (growth stood at 3.6% as of December 2018). Interestingly, when dis-aggregated into age cohorts that data shows workers aged 16-24 years experiencing the strongest rate of wage growth. Higher minimum wage laws may account for the comparatively high rise of 6.4% year-over-year within that age category.

Labor Productivity

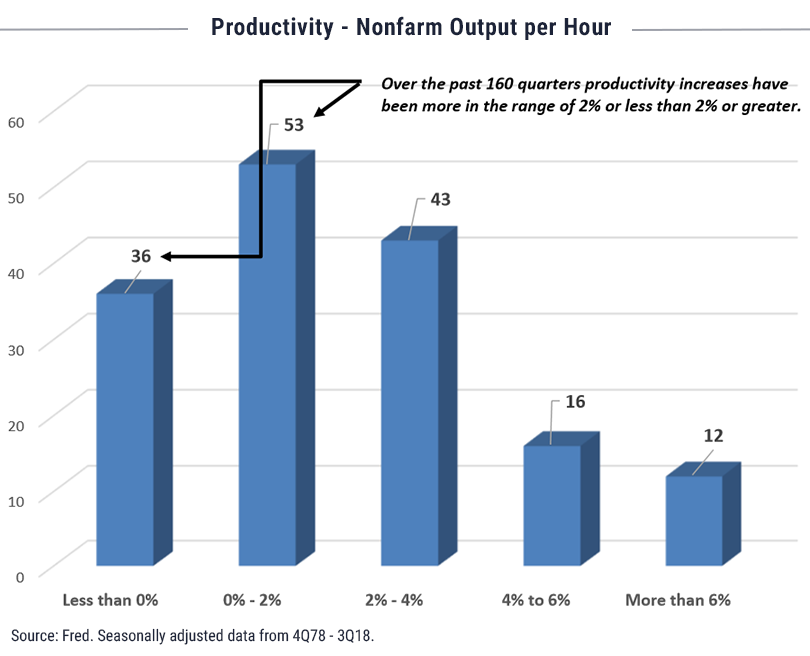

Rising wages are a fundamentally important ingredient for sustaining the current economic expansion, but wage growth for its own sake is not necessarily a positive. Rising wages must be linked with increases in worker productivity; should companies find themselves paying more for the same level and quality of output, they may be more likely to pass along the costs of wage growth in the form of higher prices. It is worth noting that productivity increases over the past 40 years have trended downwards, and it is unlikely we will see material productivity gains this far into an economic expansion.

Implication for Interest Rates

If unaccompanied by increasing worker productivity, rising wages could be problematic in the context of low interest rates. Historically, there has been a strong correlation between wage gains and interest rates. Without a meaningful slowdown in the labor market, wage gains currently running well above the current yield of the U.S. Ten-Year Treasury Note may portend upward pressure on interest rates. As of now we are hard-pressed to picture a significant slowdown in large wage growth given labor market tightness and potential policy factors such as minimum wage increases.

While we remain positive on the US economy and the fundamental strength of companies operating within it, we do bear in mind these late-cycle economic factors when formulating our own capital markets outlook and strategy. In our view continued defensiveness especially in fixed income portfolios (from a maturity and quality perspective) may be warranted given the interplay of labor data and low rates, the increased Treasury issuance required to fund the Tax Reform Act of 2018, and the increasingly flat yield curve.

For more insights, visit the WST blog.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.