WST Commentary: 2Q 2019 Markets & Economic Update

"Safety is never a permanent state of affairs." - Ser Davos Seaworth, Game of Thrones

"You get so deep into things sometimes that the abnormal seems normal and normal seems like a distant memory.” - Jordan Belfort, The Billion Dollar Whale

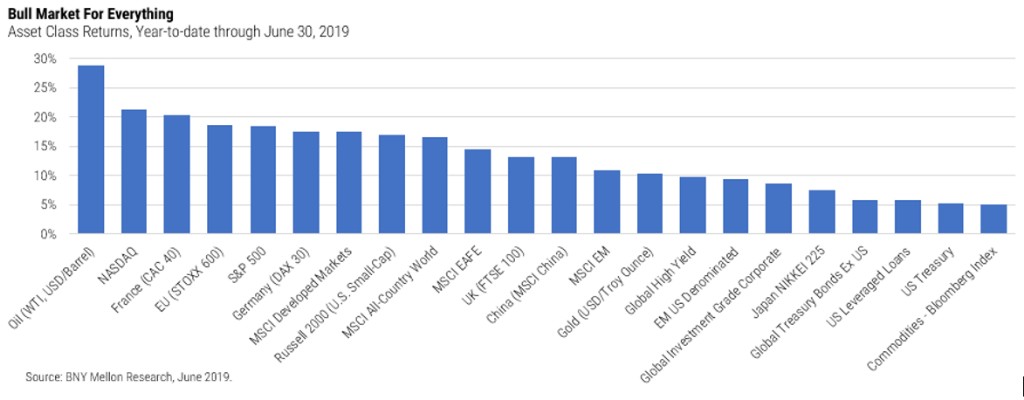

Market volatility continued in the second quarter but shook out as upside for both stocks and bonds; as of June 30 investors have enjoyed the best start to a year since 1997. In fact, as the chart on the next page reveals, it was a “bull market for everything” in the first half of 2019, with strong advances in all asset classes including stocks, bonds and commodities. ZeroHedge reports that in June all 38 of the major asset classes tracked by Deutsche Bank were positive - only the second time since 2007 that markets have been so comprehensively positive in a single month.[1] The resounding rebound in risk assets this year has been driven by positive developments in the two areas we discussed last quarter: central bank policy and U.S./China trade. The synchronized shift back to looser monetary policy and a temporary truce in the trade skirmish injected a fresh dose of optimism about the path of the global economy and eased lingering concern about a recession this year. Several trends underpin the case for continued growth and provide solid footholds for the global economy over the next year. The labor market remains rock-solid, with low unemployment and steady wage growth supporting consumer confidence and retail sales, both of which saw robust growth in May. Productivity also remains strong, as evidenced by continued subdued inflation in the face of low unemployment. Overall the glidepath of the world economy was smooth in the quarter even if the trajectory was lower.

Still, the investment landscape is complex and dynamic, and as the S&P 500 reached a new high at the end of June investors proved willing to look past the many risks lurking on the horizon. Notwithstanding positive trends, the expansion of the global economy is weaker than it was a year ago, as is the profit outlook for corporate America. Global political risks continue to escalate. The possibility of a trade war with China remains high, and as we discuss below the market may be overlooking important long-term shifts in the structure of global trade. Whatever the outcome of the current discussions, we are seeing a new trend in the use of trade policy as tool in negotiations around national defense and broader diplomacy. The trade tensions between the U.S. and China, and each side’s willingness to shift supply and production chains for political advantage, may create long-term headwinds for the global economy. To misquote Winston Churchill, free trade is the worst policy there is except for all the others. Tariffs are taxes ultimately paid by consumers, and they create a drag on the economy. Upheaval from Brexit and other European challenges add uncertainty to the current picture, and U.S. politics will move to center stage as the 2020 elections approach. Finally, while the Fed’s recent accommodation aligns it more closely with the dovish posture of other central banks around the world, it also demonstrates actionable concern about the U.S. economy. In May it appeared the crosscurrents of trade developments and concerns about global growth had moderated, but they reemerged in June and the Fed responded to surprisingly disappointing data with a quick shift in policy. Markets moved from pricing in a tightening cycle just six months ago to today expecting significant easing; given the Fed’s proclivity for quick action, any whiff of inflation could put them back on a tightening course.

For now, however, the U.S. economic expansion is the longest on record and markets rang in that milestone in full “risk-on” mode to end the quarter. Stocks, bonds and commodities rose together as sentiment improved. We have often repeated the adage “expansions don't die of old age,” but we consider unusual the level of investor complacency about the duration of this growth cycle. It’s rare for safe-haven assets such as government bonds and gold to rally at the same time stocks do, so the paradox we discussed last quarter remains in place. Bond investors believe the economy is weakening and the Fed will need to cut, while stock investors remain sanguine about economic and earnings growth. To some extent the strength in stocks this quarter can be explained as a “TINA” trade (There Is No Alternative). With the 10-year yield hovering around 2% after peaking at 3.2% at the end of 2018, yield-hungry investors are again looking to stock dividends for income. That appears a reasonable trade but is exposed to risk should earnings weaken or bond yields rise. Consistent with our cautious view on the economic cycle and earnings picture we’re positioning a bit more defensively than in recent years as we head into the back half of the year.

In our view the most worrisome current indicator is the inversion of the U.S. Treasury yield curve – a dynamic that steepened through the end of the quarter. As we discussed last quarter, the yield curve inverts when the 10-year Treasury yield falls below the short-term yield, signaling the market’s belief that the economy will weaken and force the Fed to cut the discount rate. An inverted yield curve has predicted every recession in the past 50 years with just one false alarm (in 1998). While the current inversion has been relatively brief, it does call for caution.

Economic Overview – China Syndrome

With its long expansion increasingly threatened by trade tensions and politics, the global economy walked a tightrope in the first half of 2019. The final revisions to 1Q economic data came in better than expected - reflecting 3.1% annualized growth in U.S. GDP - but trade issues weighed on growth in the second quarter. The tone was set by President Trump’s tariff increase on $200 billion of Chinese imports and restrictions imposed on U.S. companies doing business with Chinese telecom giant Huawei. While the stock market has rebounded, other indicators (most notably bond yields and the yield curve) continue to raise questions about the resiliency of global consumption and business spending.

Trade has slowed and manufacturing activity has softened, approaching recessionary levels at mid-year.

Fears of a prolonged and deeper trade war are depressing business confidence and dampening business investment, as demonstrated by J.P. Morgan's index of global business capital expenditures, which showed a decline in business investment spending in the second quarter after strong growth last year.[2] Cap-ex, defined as spending on assets with an expected useful life of more than one year, is an important indicator because it reflects corporate managements’ longer-term view of the health of the economy and their businesses. Analysts did find some grounds for optimism in the meeting between Trump and Chinese President Xi at the G20 summit in Japan the last week in June, but absent meaningful progress towards permanent resolution the impact of the trade war continues to spread in early July. Earnings estimates for U.S. corporations are declining and sentiment reflects unease about the outlook. A recent poll by Monmouth University found that more than six in ten Americans are “very concerned or somewhat concerned” their local economy will be impacted by trade tensions with China.[3] Strong consumer confidence has provided important support for the economy, and with consumer spending accounting for almost 70% of U.S. GDP the broader economy will suffer if the threat of a trade war leads to curtailed consumption.

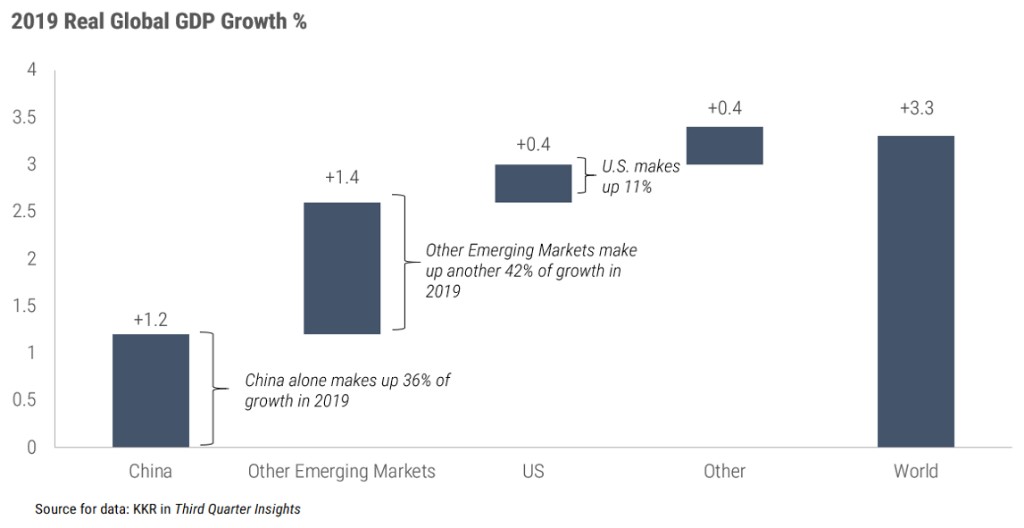

The importance of China to the health of the world economy is emphasized by the graph above, from KKR. The overall global economy is expected to grow 3.3% this year and over a third of that growth is projected to come from China, with another third driven by other emerging market economies closely tied to China. The news swirling around the week-to-week escalation of the trade conflict overshadows a fundamental change in the structure of our relationship with China and the global economy as a whole. In its Third Quarter Insights publication KKR summarizes the shift: “Globalization, the notion that there is merit to the growing interdependence of the world's economies, cultures, and populations, is under serious review - and potentially under attack.” KKR's assertion - that a modern day “Cold War” has broken out between China and the United States - has important implications for global supply chains and therefore corporate strategy and profitability. For example, $11 billion of the $70 billion that Huawei spent buying components in 2018 went to U.S. firms including Qualcomm, Flextronics and Broadcom.[4] While those relationships appear to be at least provisionally protected after the most recent trade talks in Japan, it’s easy to envision a rekindling of the conflict around Huawei or some other target.

Central Banks to the Rescue, Again

With trade tensions exacerbating the risk of a global slowdown central bank policy has reemerged as the key source of optimism (or relief) about the economy and markets. The Tax Cuts and Jobs Act of 2017 boosted domestic growth last year and continues to help this year, but with its impact already baked into expectations its stimulative force has dissipated. That leaves Fed and ECB monetary actions as the only needle-moving policy tools available to support growth. The Fed’s four rate hikes in 2018 sent tremors through the markets and the subsequent shift to neutral in January, along with continued accommodation from the ECB, drove the big rebound in valuations for risky assets early in the year. Expectations for rate cuts from both banks and possibly another round of quantitative easing by the ECB fueled the continued rally in the second quarter even while heightening the reliance on loose money.

In early July IMF President Christine Legarde, a staunch supporter of the ECB’s efforts to spur growth in the ailing Eurozone through aggressive monetary policy, was nominated to be the next president of the ECB. That announcement encouraged the markets and drove European yields lower and equities higher.

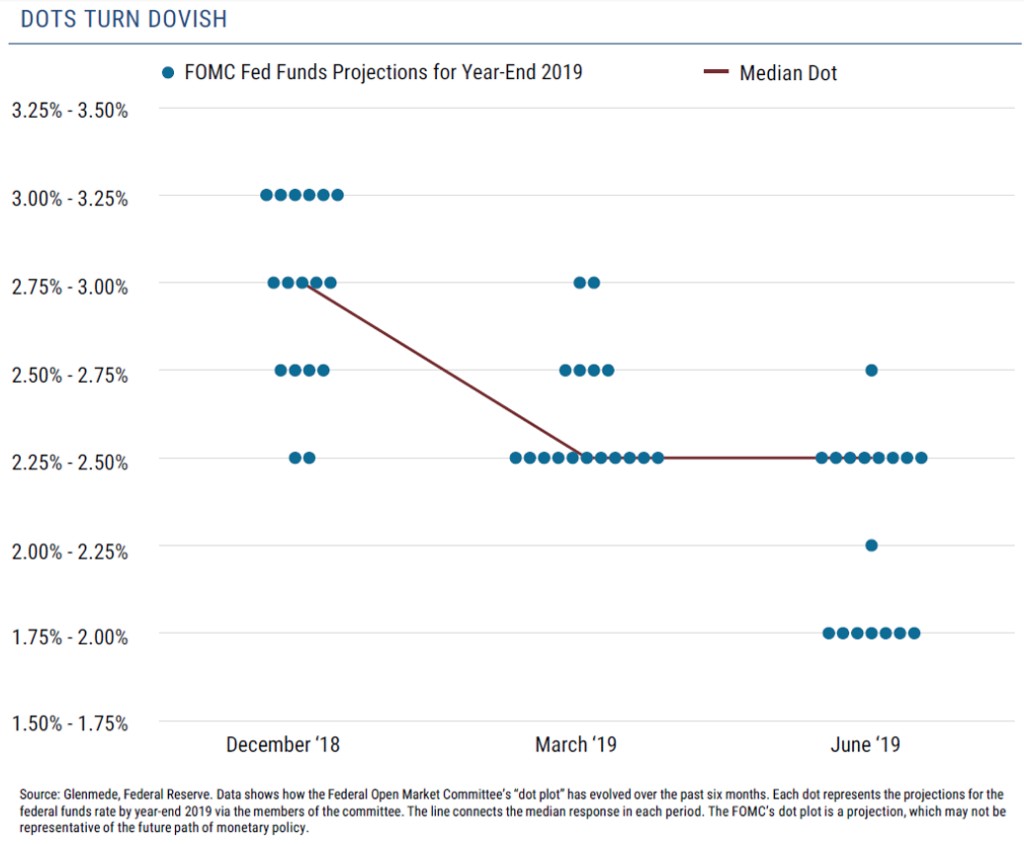

The next chart captures the evolution of Fed policy this year and demonstrates the worrisome disconnect between the Fed’s plan and market expectations for interest rates. In December the Fed’s final hike of 2018 increased the target for its benchmark interest rate to a range of 2.25% to 2.5% - the highest level since 2008. All ten members of the FOMC voted in favor of that decision and predicted two rate hikes over the course of 2019, so as of December 2018 the median projection for the Fed funds rate at year-end 2019 was 2.75% to 3.0%. The chart speaks to the significant change in the script by the June meeting, where the Fed chose to keep the rate at the current 2.25% to 2.5% range with a bias toward easing rather than tightening.

It would be difficult to overstate the impact of that policy shift and the resulting changes in expectations and market sentiment this year. With the Fed and the ECB determined to support near-term growth, Fed rate cuts are back on the table. The Fed hasn’t reduced the discount rate in over a decade, but investors remember how powerfully bullish a Fed tailwind can be for the markets, so the strong rally in the first half of 2018 not only reflects market optimism for renewed central bank support but also raises the stakes for future Fed policy. Just as quickly as sentiment turned positive in the first half it may be undone if expected rate cuts don’t materialize or - worse in the view of investors - the Fed returns to a tightening bias. The mismatch between the enthusiastic market expectations for Fed policy over the next two years and the Fed's own estimates is a major worry with the futures markets predicting two cuts this year and possibly another one or two next year. With bond and stock valuations pricing in those expectations, markets could be sorely disappointed if the Fed stands pat.

Bond Market Overview

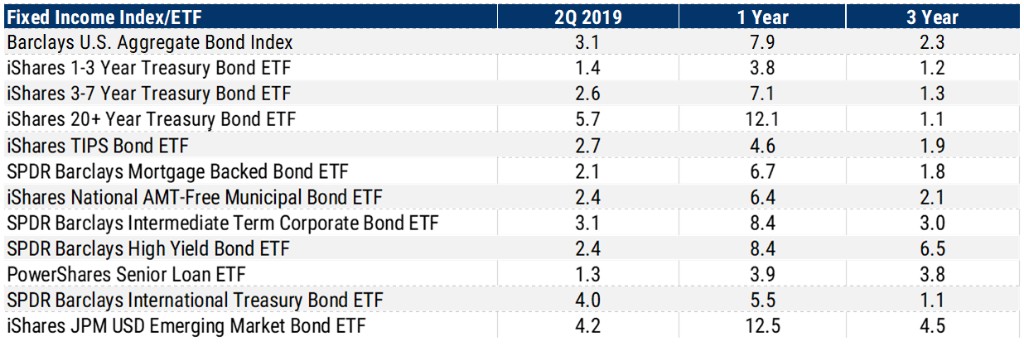

Global interest rates continued to fall in the second quarter. The U.S. 10-year Treasury yield hit its lowest level since November 2016 and the German 10-year Bund yield hit fresh all-time lows and then dropped to -0.4% on July 2. That paroxysm occurred when the ongoing fears of an economic slowdown in Europe were exacerbated by U.S. threats to impose tariffs on an additional $4 billion of eurozone goods in retaliation for subsidies to Airbus. Yields declined across all maturities and credit spreads tightened in June, providing strong returns across the board for fixed income investors. Despite relatively conservative positioning (expressed mainly through short duration), our core fixed income portfolios participated in the rally thanks to an emphasis on credit and an underweight to Treasuries.

A glaring reminder of the crazy state of bond markets occurred in late June when Austria reopened their 100-year bond and had €5.3 billion of orders at 1.2%. Barron's Jim Grant invited investors to consider that a lot can go wrong in 100 years and to imagine a hypothetical century bond issued by the Austrian government in 1919. Holders of that security were subject to setbacks including 2500% inflation in 1922, civil war in 1934, Hitler's annexation of Austria in 1938, and political and economic turmoil throughout the ‘70s and ‘80s. Setting aside history and assessing the attractiveness of the current 100-year bond, we note that inflation in Austria is currently running at 1.7% - half a percent higher than the bond yield. Grant points out that while bonds can play an important role in portfolios they have no real upside beyond the income they produce, while long-term bondholders participate fully in downside risk driven by default, repudiation and inflation.[5] Investor willingness to assume that none of those risks will materialize over the next century strikes us as a stark leap of faith, driven by desperation for yield.

The extreme low global sovereign yields exemplified by Germany and Austria anchor U.S. rates by driving demand from investors around the world for the relatively generous yields available here.

Low global interest rates in general and the inverted yield curve in the U.S. are driving a shift in the structure of the bond market that’s unfavorable for investors.

Borrowers continue to take advantage of their ability to lock in low rates by extending the maturities of their outstanding debt, so the overall duration and risk of the bond market as a whole has increased. Meanwhile lower yields mean bondholders receive less compensation at each maturity level. Duration measures the sensitivity of the price of a bond or bond index to a change in interest rates, with longer maturities and higher durations increasing the price sensitivity of bonds to movements in rates. According to J.P. Morgan, over the past 35 years the average duration and yield of the Bloomberg Barclays U.S. Aggregate Bond Index have been 4.9 years and 6.6% respectively, and as of June 30 the duration of the index is 5.7 years and the yield is 2.5%. That means bond index investors are taking 15% more risk while receiving well under half the income than the market has generated historically.[6] Given the current backdrop we’re maintaining our conservative bond allocations as we focus on capital preservation and income generation with a maturity structure shorter than that of the index.

Equity Market Overview

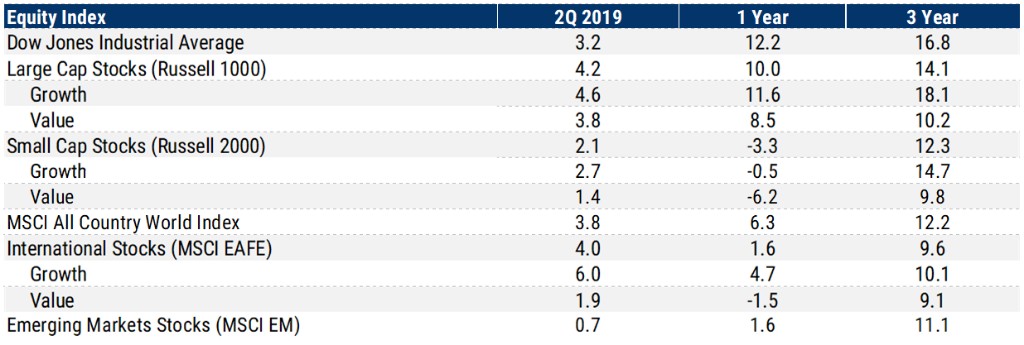

Coming off a strong rally in the first quarter equity markets continued to trend broadly forward over the past three months, albeit at a more measured pace. The S&P 500 added 4.3% in the second quarter, driving total returns to 18.5% for the year. Many of the style trends in the first quarter also persisted in this quarter, with growth outperforming value by nearly 1% and the Russell 1000 large cap index beating the Russell 2000 small cap index by 2.1%. Large cap growth stocks in particular continued to rally higher, up 4.6% on the quarter, while small cap value lagged behind at 1.4%. Internationally both developed and emerging markets underperformed U.S. equities in the second quarter, despite a weakening dollar and rising oil prices. Although Switzerland, Australia, and Germany posted strong performances north of 7%, the UK dragged the EAFE developed market index lower amid Brexit tensions and the departure of prime minister Theresa May. Meanwhile, strong gains from Russia and Brazil were overshadowed by a 4% downturn in Chinese stocks due to trade tensions, resulting in a mere 0.6% gain for the overall emerging markets index.

Looking forward into the remainder of this year and into 2020, we see more volatility in the markets driven by mixed economic signals and the increased reliance on the Fed. Earnings expectations are a concern. There is a natural erosion to beginning-of-the-year estimates as analysts tend to start the year on an optimistic note and ratchet down the numbers as the year progresses. Going into the reporting season for the second quarter the pressure on estimates is increasing with almost twice as many downward revisions as upward revisions through June. Given that trend and the high bar set last year by both earnings and equity prices, the majority of the return this year has been due to higher valuations. The median P/E ratio of a universe of 1,243 U.S. stocks was 14.4 at the start of the year and had risen to 17.7 by June 30, an increase of 22.5%. The markup is widespread as 86% of the 1,243 names in this universe are displaying higher multiples than they did in January. Large companies continue to garner favor, probably because of their perceived stability as the economic cycle ages, and the top half of the market cap universe has experienced a larger increase in valuation than the bottom half. The uptick in valuations seems at odds with the fundamentals we discussed earlier including the global weakness in capital expenditures, a key ingredient for economic growth and the drop in the global PMI manufacturing figures, which were posting their lowest reading since 2012 in May.

FactSet’s quarterly Earnings Insight report projects an estimated Q2 earnings decline of -2.6% for the S&P 500, which would mark the index’s first year-over-year earnings contraction in consecutive quarters since 2016.

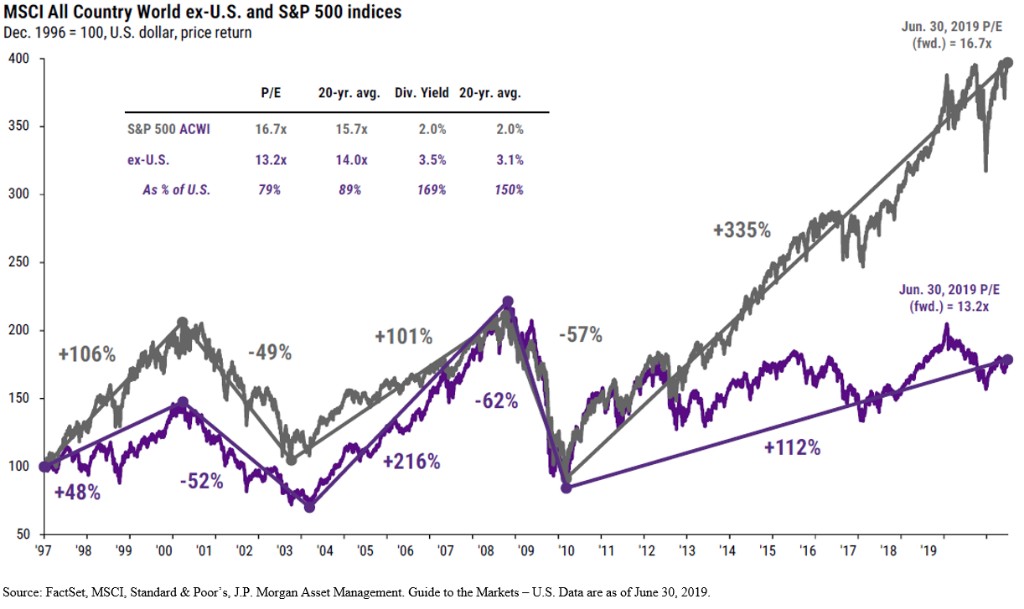

In the face of volatility and widely disparate sector performance we’re maintaining our “core-plus” equity portfolio strategy. The core of each account is invested in the S&P 500, around which we add size, style and geographic diversification. Given the relatively high valuations on U.S. large cap stocks those portfolio tilts look particularly attractive now, and over time we expect to see dollars chase undervalued segments of the market. Small-cap value is the only sector of the U.S. market trading below its 20-year average price-to-earnings ratio, and inexpensive, out-of-favor value stocks by definition offer downside protection and upside potential due to their relatively attractive valuations. As we’ve discussed in previous letters the same story applies to international equities, with emerging markets particularly attractive from a valuation and growth perspective. Stocks outside of the U.S. will benefit from any Fed rate cuts that mitigate the yield advantage that dollar investors enjoy now by enhancing the returns earned by dollar-denominated investments in foreign stocks. We continue to await the inflection point at which the growth characteristics and inexpensive valuations of non-U.S. equities trigger the next cycle of outperformance by foreign stocks. As the below chart demonstrates, since the market bottom in March 2009 the S&P 500 has tripled the return of the All Country World Index ex-US and now trades at a 25% premium on the forward P/E basis.

Summary

At the outset we stated the investment landscape is complex and dynamic. Fed Chairman Powell summarized the current situation in Fed’s June commentary, stating “the baseline outlook is favorable, but risks weigh more heavily on the outlook now.” The state of the economy is a mixed bag and volatile driver of investment markets. At a fundamental level, weaker growth dampens the long-term outlook for corporate profits, but for now the markets are cheering disappointing growth and inflation news because it prompts more central bank support. At some point additional liquidity results in diminishing returns, and monetary action cannot indefinitely extend the economic cycle. At the end of June over $14 trillion of global bonds – nearly a fifth of global supply - traded at a negative yield to maturity. How much more can central bankers do? Accommodative Fed policy is almost always supportive of risk assets, but the situation this time feels unique. The headwinds facing the markets seem more structural in nature, particularly the trade related issues. Central bank policy can't offset the damage inflicted by a major trade war, so the outlook for the economy and markets remains at risk as the trade negotiations continue.

Important Disclosures:

Unless otherwise indicated, performance information for indices, funds and securities as well as various economic data points are sourced from FactSet as of June 30, 2019. This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC that are subject to change and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy. Some portions of this letter were written in conjunction and collaboration with Capital Markets Consultants Inc. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. It is made available on an "as-is" basis without warranty. There are no guarantees investment objectives will be met.

This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC and are subject to change from time to time, and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty. There are no guarantees investment objectives will be met.

The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy.

Market indices are unmanaged and do not reflect the deduction of fees or expenses. You cannot invest directly in an index such as these and the performance of an index does not represent the performance of any specific investment strategy. We consider an index to be a portfolio of securities whose composition and proportions are derived from a rules-based model. Market indices are unmanaged and do not reflect the deduction of fees or expenses. You cannot invest directly in an index such as these and the performance of an index does not represent the performance of any specific investment strategy.

The S&P 500 Index is a market capitalization weighted index, including reinvestment of dividends and capital gains distributions that is generally considered representative of U.S. stock market. The Dow Jones Industrial Average (DJIA) is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange (NYSE) and the NASDAQ. The MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI ex USA Index is designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI EAFE Index is a stock market index that is designed to measure the equity market performance of developed markets outside of the U.S. & Canada. It is maintained by MSCI Barra, a provider of investment decision support tools; the EAFE acronym stands for Europe, Australasia and Far East. The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 845 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The Russell 2000 index measures the performance of the 2,000 smallest companies in the Russell 3000 index. The Bloomberg Barclays U.S. Aggregate Bond Index covers the USD-denominated, investment-grade, fixed-rate, taxable bond market of SEC-registered securities. The index includes bonds from the Treasury, Government-Related, Corporate, MBS, ABS, and CMBS sectors. The BofA Merrill Lynch U.S. High Yield Index tracks the performance of U.S. dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million. The BofA Merrill Lynch 1-3 US Year Treasury Index is an unmanaged index that tracks the performance of the direct sovereign debt of the U.S. Government having a maturity of at least one year and less than three years. The S&P/Citigroup International Treasury Bond ex-U.S. Index measures the performance of treasury bonds, with maturities greater than or equal to one year, issued by non-U.S. developed market countries.

[1]https://www.zerohedge.com/news/2019-07-02/goldman-only-reason-why-there-bull-market-almost-everything

[2] China Syndrome, Russell Investments, Global Market Outlook, 3Q Update.

[3] Trade War Hits China Sentiment – Financial Times, June 27, 2019.

[4] Stick To the Plan, Insights, Global Macro Outlook, June 2019.

[5] Grant, Jim The Trouble With Austria’s Centuries, Barrons, July 8, 2019.

[6] Guide To The Markets, J.P. Morgan Asset Management, July 2019.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.