Everybody Knows

Information flows faster than ever today in our daily lives and in the financial markets. For example, one of the most eagerly anticipated economic data is the monthly jobs report released on the first Friday of the month at 8:30 am by the Bureau of Labor Statistics. Reporters from around the world literally stand on the steps of the Department of Labor building in Washington D.C. in a rush to disseminate the information. This data point is an important indicator since the United States has the largest share of the global economy. Nevertheless, it is debatable whether this monthly data is so urgent it deserves such devoted real-time attention in a world that is estimated to have a 2017 GDP of nearly $78 trillion (Statistics Times).

The more instructive insight lies in what this mad scramble for incremental information says about us. It is predictable human behavior to move faster when the environment around us accelerates. For example, it is easier to move at your pace when driving on a road by yourself than it is when you feel the draft of cars traveling at a much higher speed. In this context, astute investors are aware the decision to buy an asset is two dimensional – what you know and what the market knows. Investors less aware of this relationship are much more likely to buy at the top of a market cycle, unaware there were no more buyers at higher prices.

The best poker players know the importance of playing not just the cards but playing the players sitting at the table. Lack of awareness of this strategy will most lead to consistently losing hands. The concept of Common Knowledge is a central tenet in game theory and is summarized below.

Something is common knowledge if;

- It is known by all the players

- And all the players know all the other players know it

- ... And so on

The circuitous line of reasoning in the theory of common knowledge represents the inherent difficulty of having an information advantage in gambling and investing. The reality is most of our knowledge is not originated or acquired by us but rather is part of the knowledge held by the community. Investors who believe the knowledge they hold is unique will overestimate the probability of positive outcomes in decisions driven by that knowledge.

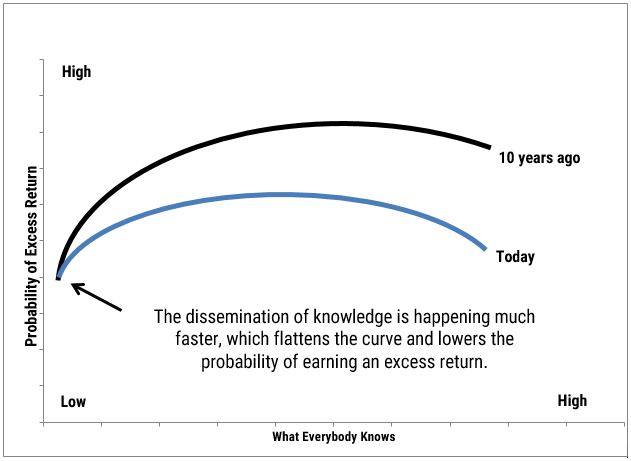

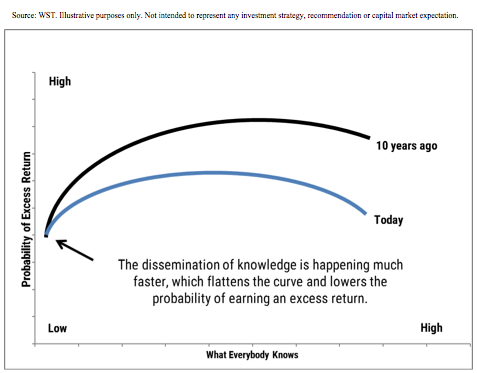

This knowledge illusion can best be illustrated by the graph below. The horizontal axis represents the level of common knowledge investors have and the vertical axis represents the probability of earning excess return defined as an above market return; there is a positive but decelerating slope to the relationship between the two variables. For example, the more people know a unique fact about a stock the probability of positive return increases as this information disseminates in the market. However, at some point the information becomes fully known and discounted in the price of the stock, which leads eventually to a lower and even declining likelihood of earning an excess return. Significantly, this line is shifting down over time with a flatter slope as information travels faster and is discounted more quickly in the market. Part time investors are especially disadvantaged by this trend as full time investors arbitrage the opportunity of incrementally valuable information more quickly than ever.

Leonard Cohen’s lyrics highlight an important observation about investing. The market sets the price and is a reflection of the common knowledge of investors. This knowledge is being discounted more quickly in the market place due to the speed of information flow. This is true both in what makes investors euphoric and what makes investors fearful in their investment decisions.

Before making any investment purchase it is imperative to ask the question “Who knows what I know?” More often than ever, the answer today will be “everybody knows.”

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.