Markets Buzz, But Is PMI a Fly in the Ointment?

While trade agreement headlines have markets in a celebratory mood, accumulating U.S. economic data speaks to the undertow of slow global growth. Unpacking the Manufacturing Purchasing Managers Index (PMI) - the leading indicator of manufacturing and service sector activity — released July 1, 2019 speaks to this dynamic.

The PMI comprises five sub-indexes derived from surveys of supply-chain managers across various industries.

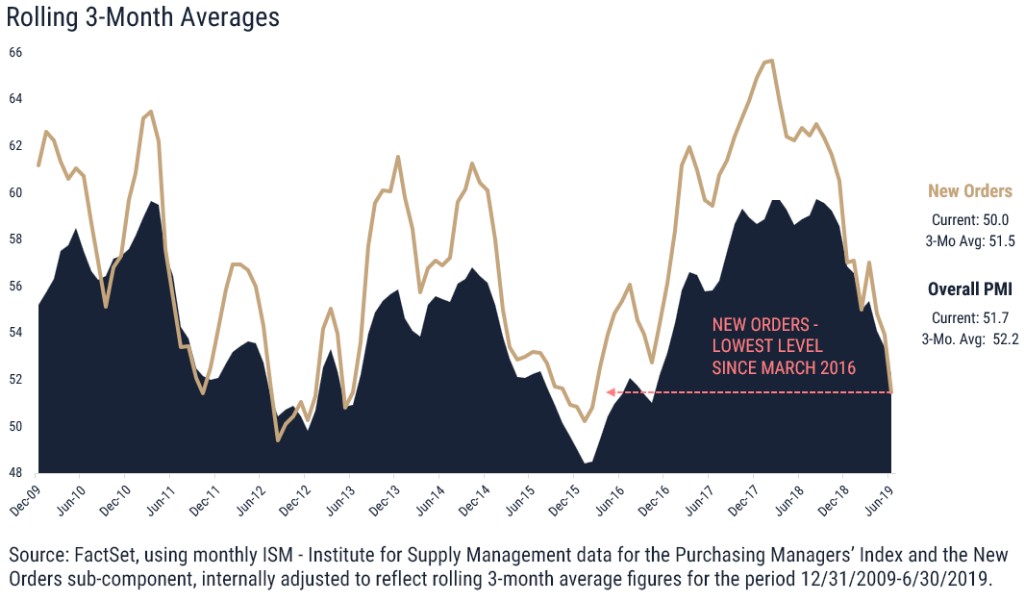

Historically the New Orders Sub-Index has been the strongest predictor of what the PMI level will look like going forward and the current trend is uninspiring at best. The graph below plots a rolling 3-month average of both the overall PMI and the New Orders Index, beginning in December 2009.

Longer-term history (going back to 1948) shows the New Orders Index is higher than the overall PMI in 81% of the monthly data - this dynamic is to be expected if an economy is growing, and for much of this history growth has been the mode for the US economy. Since the current expansion began (2009), the New Orders Index has been above the PMI 87% of the time and since November 2012 (80 months) 94% of the time.

June data - the latest - shows the New Orders Index at 50.0, at its lowest level in over three years and dipping below the overall PMI at 51.7. New Orders were below overall PMI during two of the three months in 2Q 2019 — the first rolling three-month period where this has occurred since October 2012.

What does this mean for the rest of 2019?

Estimates have retraced hard recently, just as we approach earnings season; we will know only in hindsight whether slipping economic numbers hedge earnings disappointments, but the reality of these economic data will surely be observed in earnings themselves.

A sub-50 PMI is not difficult to visualize based on the data above, and we would expect it to reignite recession narrative despite optimistic markets and a doggedly accommodative central bank. The Fed rallied the stock market recently by signaling its intention to cut rates in the coming months, and it may be that investors are placing significant faith in the Fed to leverage policy tools to reverse the recent weakness and current trend in manufacturing data.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.