Inflation: What's in a Number?

Historically, few economic measures have outweighed inflation in terms of importance, as inflation impacts nearly every facet of the economy. As consumers, everyone is subject to changes in the prices of goods and services. As investors we are beholden to inflation by way of its impact on interest rates on borrowed funds and interest income earned from savings options. Assets that produce no cash flow are particularly sensitive to expectations of inflation imputed on their future values when sold.

“Inflation is like sin; every government denounces it and every government practices it.” - Sir Frederick Leith-Ross

If inflation has been preeminent, it has been just as difficult to measure accurately. As consumers, our lives are too complex to generalize and at the same time our experiences are highly localized and driven by where we live, or where most of our consumption occurs. Forward-looking expectations of inflation by investors are notoriously trend-following and perceived inflation is often widely askew of actual or observed inflation. Simply put, inflation—as with beauty—is in the eye of the beholder.

The Federal Reserve’s Dual Mandate

Ponder that reality relative to the dual mandate of the Federal Reserve. The Fed has long operated its monetary policy according to two primary objectives focused on maximum employment and price stability. The former is a long-term goal dramatically impacted by demographics, immigration policy, technology and a multitude of other factors and inputs. As a result, there is no explicit or “magical” employment number that the Fed targets—they will know it when they see it. By contrast, the Fed does set an explicit number on inflation, considered shorter-term in nature and controllable through market operations as well as interest rate targets set by the central bank. Historically, the Fed will attempt to curb inflation through interest-rate increases and vice-versa.

It is therefore significant what measure of inflation the Fed uses and the level at which it drives their policy decisions. While most of us are familiar with the Consumer Price Index (CPI) as the de facto measure of inflation, the Fed prefers the Personal Consumption Expenditures Price Index (PCE) to base its inflation target. Plenty of economists concur with the Fed in its preference for the PCE over the CPI because it is considered more dynamic and adaptable to changing consumption patterns, and a broader measure of actual expenditures. The Fed has set 2.0% as its target rate of inflation.

Hold on a Minute?

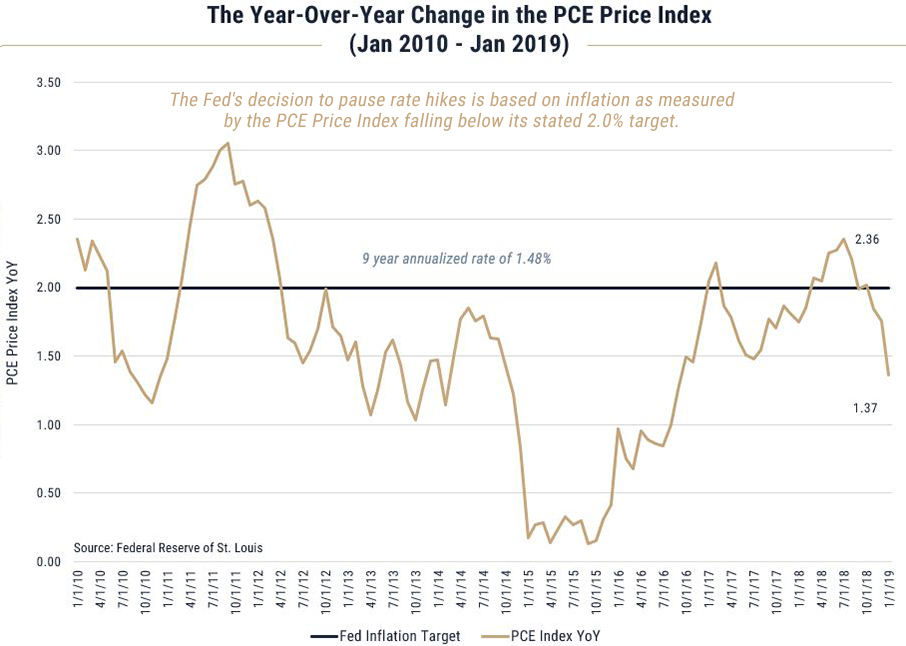

In his March 20 news conference, Fed Chairman Jay Powell surprised markets by stating the decision of the Federal Open Market Committee (FOMC) to momentarily pause its interest rate increases. The Fed’s decision appears sensible when we consider the graph below—which plots the year-over-year change in the PCE Price Index and shows that measure fell from above the 2.0% target last July—when it hit 2.36%—to the January 2019 level of 1.37%.

Investors in long-term Treasury securities responded by lowering the yield they demanded from 3.23% in early November last year to the current yield of around 2.52%.

What About the Long Term?

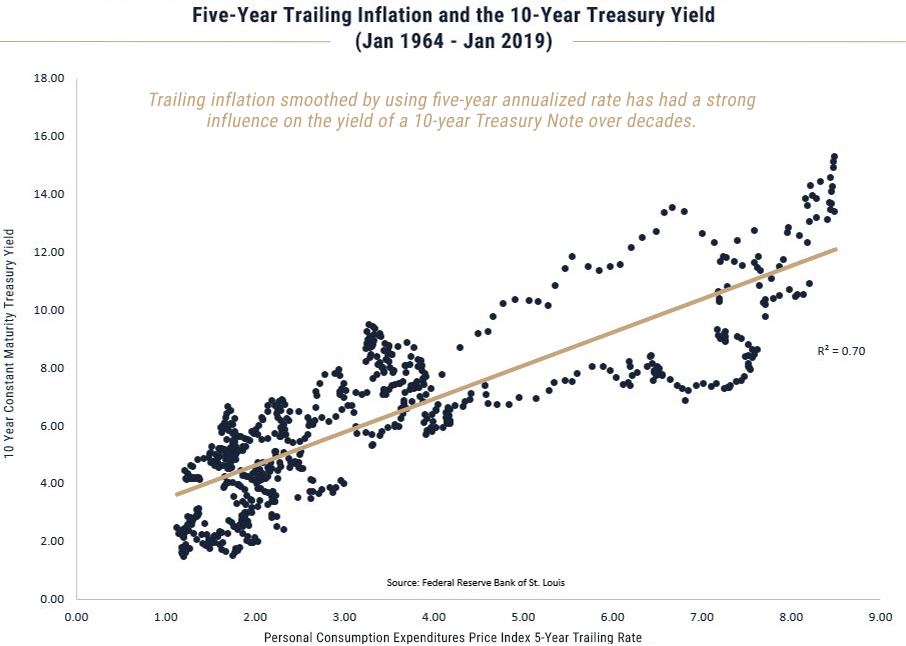

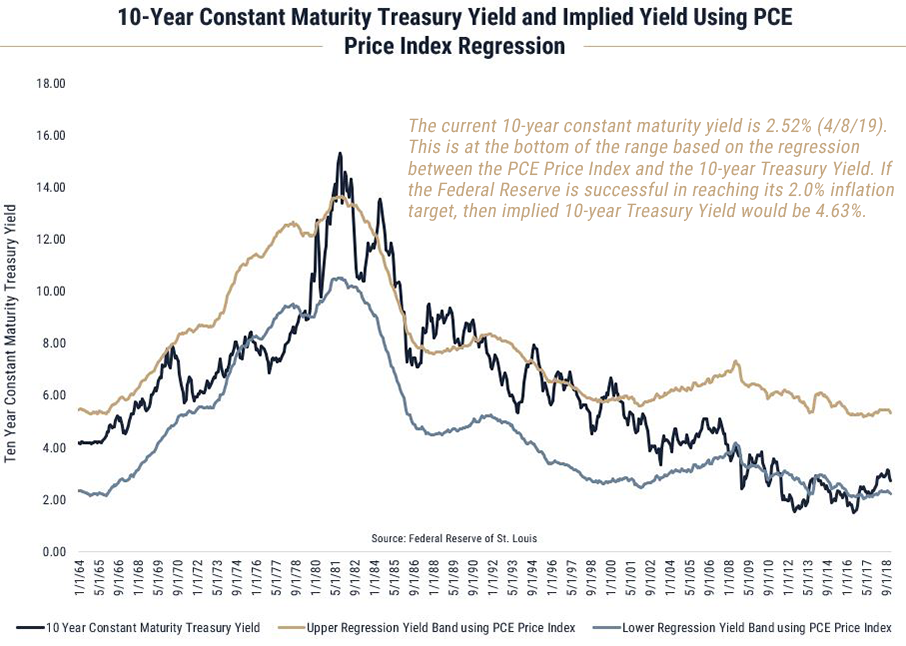

Shorter-term movements aside, investors in 10-year Treasury notes and stocks are more concerned about the long term. This compelling data can be interpreted to suggest that the Fed has only temporarily lost its appetite for rate hikes desire to raise rates and unwind its own balance sheet. The first graph below highlights the relationship between trailing five-year inflation, as measured by the PCE Price Index, and the 10-year Treasury yield—data measured monthly since January 1964. It seems clear that 10-year Treasury yields are heavily dependent on what the core PCE Price Index inflation has been over trailing five-year periods. From this analysis, we can now impute the trendline regression value of the 10-year Treasury yield and compare it to the actual yield. This is highlighted in the second graph and includes upper and lower bands based on +/- 1 standard deviation of the regression line.

So What?

Stock investors reacted exuberantly to the Fed’s message on holding rates steady and resurgent markets quickly erased much of the losses from the 4Q 2018 meltdown. This reversal seemed to reflect belief that the Fed had pulled itself back from the brink of further tightening in the face of a slowing global economy. Markets don’t seem quite as concerned that the Fed is just as capable of reversing or backtracking should the data recommended that course of action.

We agree the data-dependent Fed needed to heed what is happening at home as well as abroad and, in particular, review its own policy intentions relative to the growing accommodation of other global central banks. However, we are also focused on whether this prolonged period of low inflation (as measured by the Fed’s definition) has compelled investors to look past the inflation piece of the Fed’s mandate.

Central banks overseas appear committed to stemming the deceleration of growth and keeping their economies on an even keel. Those efforts may in turn yield better economic data that—in the US and especially from abroad—may bring the 2% targeted inflation rate back into focus and push long-term rates back up. We’re not convinced that investors have priced in this possibility. Keeping a sharp eye on the PCE Price Index as the measure of inflation will be critical for bond investors.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.