WST 3Q 2018 Commentary

In the third quarter investors set aside concerns about Fed tightening, rising interest rates, trade wars and deficit spending, focusing instead on the strength of the domestic economy and robust corporate profit growth. The U.S. economic recovery is in its 10th year, and the current expansion is the second longest since World War II. Economic expansions don't die of old age, but objective indicators and a review of history suggest that we are late in the cycle. As we discussed last quarter the synchronized global economic growth of 2017 ended this year as both developed and emerging overseas economies proved unable to keep pace with the expansion in the U.S. Still, while the pace of global growth is slower and less synchronized, job and wage growth in most regions continue to support consumer spending, the key driver of any economy. The nearly-unanimous consensus among economists is that the risk of a recession in the next 12 to 18 months is very low. “Growing but slowing” is the mantra of the forecasters.

In the third quarter investors set aside concerns about Fed tightening, rising interest rates, trade wars and deficit spending, focusing instead on the strength of the domestic economy and robust corporate profit growth. The U.S. economic recovery is in its 10th year, and the current expansion is the second longest since World War II. Economic expansions don't die of old age, but objective indicators and a review of history suggest that we are late in the cycle. As we discussed last quarter the synchronized global economic growth of 2017 ended this year as both developed and emerging overseas economies proved unable to keep pace with the expansion in the U.S. Still, while the pace of global growth is slower and less synchronized, job and wage growth in most regions continue to support consumer spending, the key driver of any economy. The nearly-unanimous consensus among economists is that the risk of a recession in the next 12 to 18 months is very low. “Growing but slowing” is the mantra of the forecasters.

"In my fifty years of experience on Wall Street I've found that I know less and less about what the market is going to do but I know more and more about what investors ought to do, and that's a pretty vital change in attitude." - Benjamin Graham

Our expectations align with the consensus view, but our focus remains more tuned to the risks and opportunities that our clients face than on the exact timing of a shift in the economy. As the economic cycle matures the trends in corporate earnings, inflation and interest rates may differ considerably from the steady, reliable growth we’ve enjoyed over the past decade. The interplay among important variables including Fed policy, tax cuts, trade policy, and divisive politics opens the economy and markets to a wider range of outcomes than normal. Most important among those variables is Fed policy, and between now and the end of the year we will get confirmation of the Fed’s direction and more clarity on whether they will pause the current rate-hike cycle at today’s close-to-neutral level or push on into tightening mode. With core inflation expected to rise above the Fed's target level, the risk increases that the Fed will overshoot on interest rates.

As we discuss in the Fixed Income section later in this commentary the bond market continues to express its skepticism about economic growth even as the Fed pushes short-term interest rates higher. What can’t be overstated is the role played by the liquidity provided by the Fed through its zero-interest rate policy and quantitative easing in the economic recovery from the financial crisis and the long expansion that followed. An important example of the shifting interest rate picture is the mortgage market, where rates hit seven-year highs on October 1st, up more than one percent from a year ago. Higher interest rates hit consumers and businesses in the pocket, and after a decade of cheap money borrowers may have trouble adjusting to “normal” interest rates.

The increased uncertainty and risk in the global economic picture comes at a time when most financial assets are priced at or above their long-term averages. The best performing assets, most notably large-cap U.S. growth stocks, have a speculative feel. Given this backdrop we believe the time is right to play defense.

"Offense sells tickets, but defense wins championships.” - Bear Bryant

From a portfolio perspective that means ensuring that the mix of stocks, bonds and cash matches our clients’ needs. In the bond segment of portfolios we are keeping durations relatively short and credit quality relatively high, and within equities we are maintaining allocations to reasonably priced sectors including international and value stocks. To paraphrase legendary investor Ben Graham, it’s much more important to have your portfolio allocated correctly than it is to get the market timing right. Thus our focus remainson allocation and strategy at the client level.

Economic Overview

The global economy continued to roll in the third quarter albeit with regional lumpiness and increasing dependence on above-trend U.S. growth. As we mentioned the consensus forecast calls for continued expansion through 2019, but with a wide range of potential outcomes. An array of economic crosscurrents complicate the outlook. Tariffs and trade frictions remain problematic. Other worries include the growing U.S. budget deficit, the slump in emerging markets, political and budget turmoil in Italy and elsewhere, and rising oil prices. Each of these stories will influence the global economy as they play out. Interwoven among all of the other factors is the most important variable over the next 18 months: Federal Reserve policy.

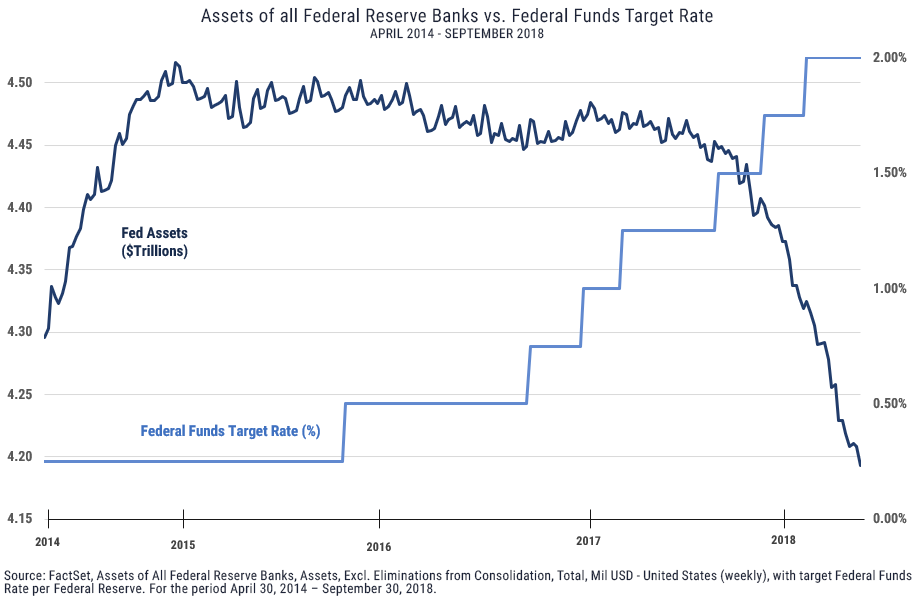

As the U.S. economy collapsed in 2008 the Fed stepped in with a two-pronged policy approach that stopped the freefall and set the country on a path to recovery. First they cut the fed funds rate from 5.25% to zero, flushing the financial system with cheap money. With the economy still sputtering the Fed undertook four rounds of quantitative easing, which by 2010 had added over $2 trillion of liquidity to the U.S. financial system. We will sidestep the details and mechanics of quantitative easing but state simply that the purpose of this expansionary monetary policy was to lower interest rates and spur economic growth by allowing banks to lend more money to more borrowers. By expanding its balance sheet through open-market purchases of financial assets, the Fed made cash available to the system. By setting interest rates at zero the Fed essentially allowed banks to purchase their inventory (money) for free, thus encouraging the banks to make more loans at lower interest rates and stimulating demand by giving businesses access to money to grow and shoppers credit to buy more goods and services.

Now, ten years into recovery, the Fed is reversing those policies by raising the fed funds rate and allowing its balance sheet to shrink as the bonds it purchased under QE mature. Some say the Fed's job is done, but the long-term success of the Fed intervention in the financial crisis can only be judged after the unwinding is complete. Interest rates and the Fed’s balance sheet remain far from normal levels, and it is yet to be seen if the Fed can normalize interest rates and unwind its balance sheet without causing a recession. The graph below depicts the changing trajectory of interest rates and Fed asset holdings. As Fed policy raises the cost of credit they effectively raise the prices of cars, houses, washing machines and anything else that consumers or companies borrow to own. Whether the economy is ready for those cost increases is an important question.

Equity Market Overview

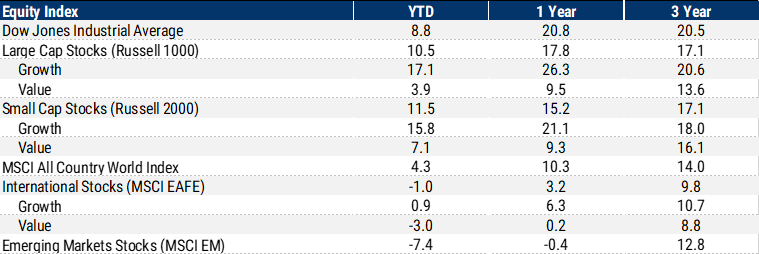

The equity markets took note of the divergence in growth rates around the world during the third quarter, with the Russell 1000 Index of domestic large-cap stocks rising 7.4% while developed market international stocks (MSCI EAFE Index) rose only 1.4% and emerging markets equities (MSCI EM Index) declined 1%. The performance gap between domestic and international stocks this year has U.S. stocks trading at their highest premiums to international shares in many years, creating an opportunity for patient investors to capitalize when the valuation gap narrows, as we believe it will. Even more dramatic than the gap between the performance of equity markets in the U.S. and the rest of the world is the continued investor preference for growth stocks over value stocks. During the third quarter the Russell 1000 Growth Index (up 9.2%) outperformed the Russell 1000 Value Index (up 5.7%) by 3.5%. Over the past year the gap between growth and value as measured by those two indices has widened to 17%, with the Growth index up 26.3% and the Value index rising just 9.5%. Our long-term equity allocations include both international stocks and value stocks, so these performance trends are the focus of our strategy discussions.

The lackluster performance of emerging markets equities over the past year has been driven partially by fundamental factors but exacerbated by a number of idiosyncratic issues and fears that should ease as the cycle continues. As we read the research being generated by investors specializing in emerging markets, the overall tone is positive. The emerging markets "bucket" includes a wide range of regions and countries but the largest and most important emerging economies are enjoying economic growth in the 4-5% range. The outlook for continued growth is good. The demographics of the emerging world are favorable with generally younger populations and expanding consumer bases. Emerging market specialists see competitive, growing companies with good long-term prospects and the ability to withstand economic cyclicality comparable to that of companies in the United States.

The strongest headwinds facing emerging market equities over the past year have been tightening credit and the stronger dollar, both factors driven by the shift in Fed policy. Higher interest rates in the U.S. make the dollar more attractive to investors around the world but create problems for countries that have issued dollar-denominated sovereign debt. For them, every dollar of debt service costs more in their local currency as the dollar strengthens. If interest rates in the U.S. continue to rise and the dollar continues to appreciate, emerging economies will continue to face these headwinds. However we think the equity markets have overreacted as sentiment has been crushed by factors including fears of a trade war, concerns about politics and elections, and the economic crises in Argentina and Turkey, which face deep challenges but together make up only 2% of global GDP.

As we assess the outlook for emerging markets the country we will follow most closely is China, and as the fourth quarter begins the trade war with the U.S. is beginning to take a toll. Chinese export orders dropped in September by more than any month in two years; the slowdown is broad, impacting automobiles, machinery, and other sectors. The Chinese central bank has responded by reducing bank reserve requirements three times this year and is expected to do so again in light of the September data.[1] We’ll be watching the news and data out of China as the fourth quarter progresses. With the Chinese stock market down over 14% this year the sentiment around China is so negative that some margin of safety exists to buffer against additional downside. Any good news on the trade front could trigger a bounce in stock prices. Interestingly the MSCI Emerging Markets Index rallied 4.7% during the last week of the quarter on encouraging reports about trade talks between the U.S. and China.

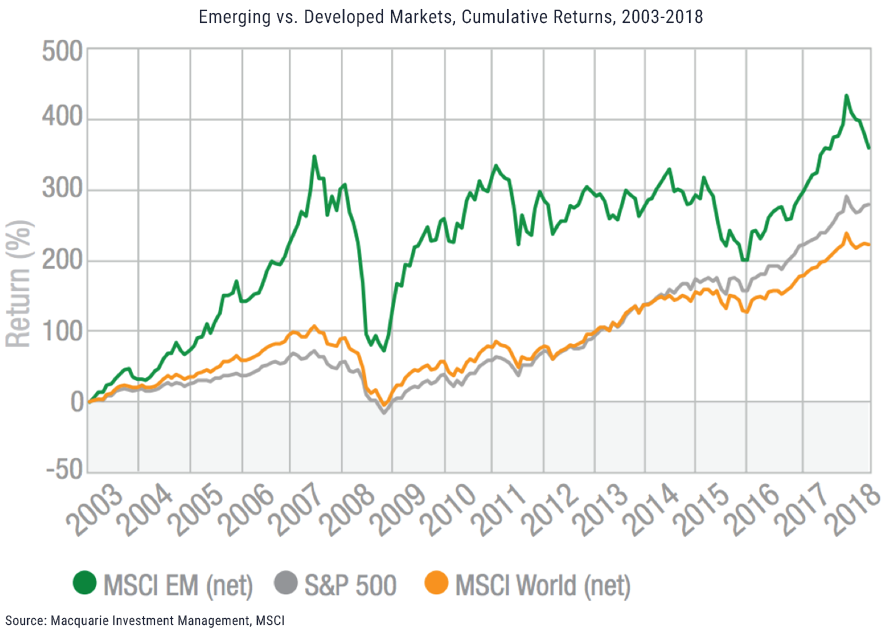

From a long-term perspective, the case for maintaining a portfolio allocation to emerging markets is strong. Return patterns on EM equities are definitely more volatile, but long-term investors in the sector have historically been rewarded for the risks they have taken. As the chart above demonstrates, despite the huge drawdown in 2007-2008 and the current underperformance in 2018, emerging markets equities have outperformed the S&P 500 and the MSCI World indexes by substantial margins over the past 15 years. It's easy to forget that emerging markets were the best-performing asset class in 2017 after sentiment bottomed in 2016.

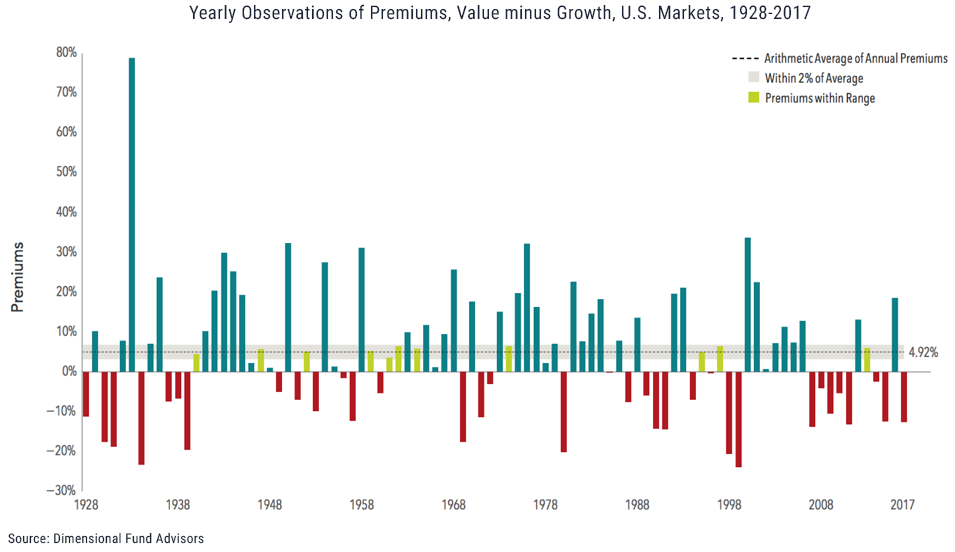

The performance gap between growth and value stocks also looks different when viewed from a long-term perspective. From 1928–2017 the value premium, defined as the return difference between stocks with low relative prices (value) and stocks with high relative prices (growth), in the U.S. had a positive annualized return of approximately 3.5%, meaning that value stocks have outperformed growth stocks by 3.5% annually over that 90-year period.[2] In seven of the last 10 calendar years, however, growth stocks have outperformed value stocks in the U.S., understandably leading some investors to wonder if this extended period of underperformance undermines the validy of the long term data. With the help of a study by Dimensional Fund Advisors (DFA), we looked at history to consider that question.

The following chart shows yearly data for the U.S. value premium going back to 1928. The annual arithmetic average for the premium is close to 5%, but in any given year the premium has varied widely, sometimes experiencing extreme positive or negative performance. In fact, there are only a handful of years in which the premium was within a 2% range of the annual average; most other years were farther above or below the mean. This data reveals the extreme variability of annual returns and reinforces the need for patience in a long-term investment program. If returns were predictable in the short-term based upon recent performance then tactical shifts between sectors would be an effective way to beat the market. Unfortunately the data reveal the difficulties that performance-chasers face, and we believe the best way to capture the long-term growth that stocks offer is to maintain a disciplined, patient allocation that includes the portfolio tilts that offer the highest returns.

So, what about the longer-term performance? While the current stretch of underperformance for the value premium is unusual it is not unprecedented, nor does it suggest that investors should abandon their alloctions to value stocks. In the same study mentioned above, DFA evaluated the annualized performance of the eighty 10-year rolling calendar periods since 1928 and found that the value premium has been positive, meaning value stocks outperformed growth stocks, in 67 of those periods. The 10-year period ending 2017 is the fifth worst period of underperformance by value stocks in the study. It all sounds grim until the final piece of the puzzle is put in place, and that is the fact that the best periods for value stocks tend to follow the most dramatic periods of underperformance.[3]

The statistical analysis may seem daunting, but think back to the internet and housing bubbles, both of which saw sustained periods of outperformance by growth stocks over value. Inexpensive (value) stocks provide a buffer in poor markets that has historically more than offset any performance missed during frothy growth-dominated periods. What does all of this mean for investors? While a positive value premium is never guaranteed over any specific time frame, including value stocks in a portfolio means the investor is “buying low” with part of their assets at all times. Inexpensive, out of favor market segments and companies can stay that way for long periods, but in the past buying value has been the recipe for success. Because the value premium has not historically materialized in a steady or predictable fashion, we remain convinced that a consistent investment approach that maintains exposure to value stocks in all market environments gives us the best chance to capture the premium over the long run.

Bond Market Overview

Bond bears were roused from their long hibernation in the third quarter as investors observed the momentum of the U.S. economy and began to prepare for more aggressive Fed tightening. With three rate hikes done in 2018 and a fourth expected in December, the central bank is increasingly hawkish. Economic data on GDP growth, employment, and wages were surprisingly strong at each reading in August and September, and the widely held assumption that the Fed would pause in 2019 is giving way to a belief that the rate increases will continue into next year. The tone of the Fed’s commentary is telling. Normally dovish Fed governor Lael Brainard broke from her previously “looser-for longer” view in a speech in September when she indicated that more rate increases are warranted given the economic stimulus provided by the Trump administration's tax cuts.[4] Her comment matched the perspective of Fed Chair Jay Powell, who said in a speech in early October that he was “very happy” with the “remarkably positive” U.S. economy and predicted that the current expansion could “continue for quite some time.”[5]

With the economy on track and the Fed apparently determined to stay ahead of inflation, the fixed income markets have shifted in 2018. While the most pronounced change is in the short maturity range where the 1-year Treasury bill now yields over 2.5%, long-term rates have risen as well. Long-term bonds are most sensitive to interest rate increases and were the worst performing segment of the market during the quarter despite the flattening yield curve. Treasury bonds in the 20 year+ maturity range have generated a total return of negative 3.5% this year, including income. Bank loans and other floating-rate products, which we discussed last quarter and have added to portfolios where appropriate, are the best-performing fixed income asset class this year with a 4% return as measured by the PowerShares Senior Loan ETF. Corporate and particularly high-yield bonds also performed relatively well in the third quarter because optimism about the economy translates into bullishness about corporate performance.

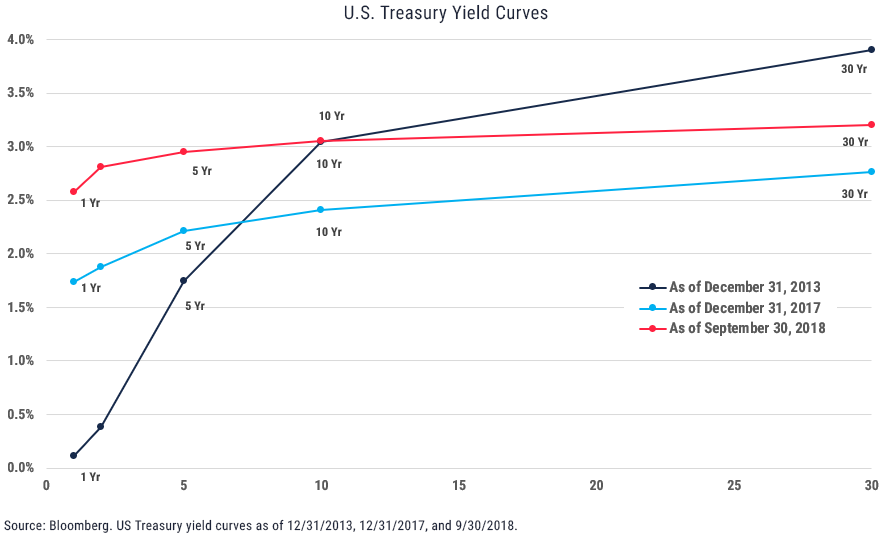

The ongoing flattening of the yield curve is important. The short maturity segment of the bond market is driven primarily by the rates set by the Fed but longer term yields are driven by expectations about growth and inflation. As we mentioned at the outset the narrow gap between short and long yields reflects not only the ongoing strong demand for income-producing assets but also skepticism on the part of bond investors about the long-term outlook for growth and inflation. If the market believed that economic growth would remain strong and that inflation would rise it would demand higher yields on longer-term bonds. With the Fed apparently intent on pushing the Fed funds rate to 3% or higher from its current target range of 2% to 2.25% the market is facing two possible scenarios: either the yield curve will invert or long-term rates will rise. As the fourth quarter gets underway and the strong economic data continue to flow, the second scenario seems to be occurring. As we write this letter during the first week of October the yield on the 10-year Treasury has breached 3.2%, its highest level since 2011.

With cash and other short-duration, low-risk investments now offering reasonable returns after years of zero interest rate policy and long-term bonds expensive and vulnerable to the risk of a steeper yield curve, we have an opportunity to reasses the positioning of bond allocations. Fixed income assets play two roles in portfolios: capital preservation and income generation. The dearth of yield on low-risk assets over the past decade forced investors to accept more risk in their quest for income. Now we can shorten durations and still enjoy reasonably good income streams, even while focusing on capital preservation. As the graph below demonstrates investors are not well-compensated for taking duration risk beyond the 5-10 year range, so we continue to focus on that part of the curve. By doing so we can harvest almost all of the yield available, minimize volatility and remain positioned to take advantage of rising rates by having cash available to invest at higher yields as bonds mature.

Summary

With the economic expansion and bull market among the longest in history, it’s tempting to extrapolate those trends into the future. Both have lasted much longer than almost any forecaster predicted. Global economic fundamentals remain positive and while there are many variables that could derail global growth none appear to pose imminent risks. Still, we’re inclined to maintain our relatively conservative and defensive positioning. Certainly the “easy money” has been made for this cycle, and with valuations expensive and interest rates rising the odds are in favor of lower returns and higher volatility. The mix of assets in any client’s allocation depends upon their individual needs and preferences, but we’re focused now on making sure that portfolios have the resilience to achieve those objectives in a more volatile environment. We’ll keep you updated as the fourth quarter progresses.

Sources

[1] Liyan Qi and Lingling Wei, China’s Economy Losing Steam as Trade Conflict With U.S. Intensifies, The Wall Street Journal, October 1, 2018.

[2] Source: DFA. Computed as the return difference between the Fama/French US Value Research Index and the Fama/French US Growth Research Index.

[3] Where’s The Value? Dimensional Fund Advisors, July 2018.

[4] Wigglesworth, Robin. Investors Buckle Up For Longer Fed Tightening Cycle, Financial Times September 25, 2018.

[5] Badkar, Mamta. Strong Economy Sends U.S. Treasury Yields Soaring, Financial Times October 4, 2018.

Unless otherwise indicated, performance information for indices, funds and securities as well as various economic data points are sourced from FactSet as of September 30, 2018. This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC that are subject to change and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy. Some portions of this letter were written in conjunction and collaboration with Capital Markets Consultants Inc. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. It is made available on an "as-is" basis without warranty. There are no guarantees investment objectives will be met.

This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC and are subject to change from time to time, and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty. There are no guarantees investment objectives will be met.

The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy.

Market indices are unmanaged and do not reflect the deduction of fees or expenses. You cannot invest directly in an index such as these and the performance of an index does not represent the performance of any specific investment strategy. We consider an index to be a portfolio of securities whose composition and proportions are derived from a rules based model. Market indices are unmanaged and do not reflect the deduction of fees or expenses. You cannot invest directly in an index such as these and the performance of an index does not represent the performance of any specific investment strategy.

The S&P 500 Index is a market capitalization weighted index, including reinvestment of dividends and capital gains distributions that is generally considered representative of U.S. stock market. The Dow Jones Industrial Average (DJIA) is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange (NYSE) and the NASDAQ. The MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI ex USA Index is designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI EAFE Index is a stock market index that is designed to measure the equity market performance of developed markets outside of the U.S. & Canada. It is maintained by MSCI Barra, a provider of investment decision support tools; the EAFE acronym stands for Europe, Australasia and Far East. The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 845 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The Russell 2000 index measures the performance of the 2,000 smallest companies in the Russell 3000 index. The Bloomberg Barclays U.S. Aggregate Bond Index covers the USD-denominated, investment-grade, fixed-rate, taxable bond market of SEC-registered securities. The index includes bonds from the Treasury, Government-Related, Corporate, MBS, ABS, and CMBS sectors. The BofA Merrill Lynch U.S. High Yield Index tracks the performance of U.S. dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million. The BofA Merrill Lynch 1-3 US Year Treasury Index is an unmanaged index that tracks the performance of the direct sovereign debt of the U.S. Government having a maturity of at least one year and less than three years. The S&P/Citigroup International Treasury Bond ex-U.S. Index measures the performance of treasury bonds, with maturities greater than or equal to one year, issued by non-U.S. developed market countries.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.