WST 3Q 2017 Quarterly Commentary

The global "bull market in everything" continued in the third quarter with stocks around the world finishing at all-time highs, bond yields hovering near all-time lows, credit spreads continuing to narrow, and private equity, debt, and real estate funds all reporting preliminary results in line with the strong returns in the public markets. Some have called this eight-year rally in investment assets "joyless” because while investors are generally optimistic they are not showing the signs of euphoria that we might expect at this point in the cycle. At under 50%,[1] hedge fund net equity exposure implies a mood of caution. The large cash balances on corporate balance sheets and strong demand for low-yielding but reasonably safe income securities, such as corporate bonds, reveal investor willingness to forgo the opportunity for gains to protect capital with at least a portion of a portfolio. Confidence and complacency as measured by market volatility are high, but it does not appear as if any individual asset classes have reached bubble territory comparable to tech stocks in 2000 or the housing market in 2008.

Even so, count us among the cautious. With the “sun shining so bright” and “things going so right" some degree of complacency is understandable, but the extremely low volatility in stocks this year reflects a sense of invulnerability we find unsettling. It’s not even a “buy the dips” market; there are no dips! The favorable trends in the global economy provide a solid backdrop for corporate earnings, and investors are extrapolating recent earnings performance and applying high valuations to those optimistic estimates. The ultimate underpinning of all investment prices is the long-term bond yield because low yields make other investments more attractive in comparison. Long-term interest rates have fallen steadily since the 1980’s and have been supported by unprecedented central bank intervention since 2009. With the turning point in Fed policy behind us and the Fed’s peers around the world likely to follow soon, we share the concern expressed in The Economist that global central bank policies have distorted bond markets and, by extension, the prices of all financial assets.[2] We will be watching carefully for any upward pressure on long-term rates as the bond market’s supply/demand dynamic shifts after the Fed begins shrinking its balance sheet in October. Also, after the relatively hawkish tone of Fed Chair Yellen’s comments at the September meeting, the market is now pricing in a 70% chance of another rate hike in December. That move, when coupled with tapering by the Fed and the European Central Bank and less aggressive asset purchases by the Bank of Japan, could present a real test for the bond market.

The good news is that for now investment returns around the world are being driven by strong fundamentals, and the outlook for the steadily expanding global economy has improved over the past three months. The IMF released its World Economic Outlook on October 17 and revealed that the second quarter saw the fastest growth in global GDP in five years with all parts of the world participating and no region overheating. The low volatility in the investment markets is mirroring the subdued volatility in economic data. Synchronous global growth with low inflation is exactly the mix of conditions that central bankers would choose as they begin to normalize monetary policy. The durability of the economic expansion mitigates the risk that reduced accommodation will trigger a global recession, and low inflation allows the policy-makers to take a patient, measured approach as they consider their path to higher policy rates and smaller sovereign balance sheets. Investors will be watching, because as we discuss later central bank policy is a key risk facing the markets today.

On the political front investors seem desensitized to the incessant rancor, and while the Trump administration has failed to gain traction on any of its promised legislative agenda items most experts do expect a reduction in corporate taxes late this year or next. Depending upon the president's flexibility and negotiating skills we should also see some progress on deregulation and infrastructure spending, with the latter being driven partially by rebuilding in the wake of hurricanes Harvey and Irma. From a big picture perspective it is somewhat surprising and certainly encouraging that in light of the strong rally after Trump's election last November the market has not responded more negatively to the new administration's inability to make headway on its pro-growth, business-friendly agenda. The fundamental strength of the global economy is the source of the market’s patience, but we think it will be important for the administration to make some progress next year or risk disappointment, which could be reflected in investor sentiment.

Economic Overview

The final revisions of the second quarter GDP numbers revealed, as expected, solid performance by the U.S. economy during the first half of the year. Growth averaged just above 2% annualized and consumer spending and business investment posted the best back-to-back quarters since 2014. Less widely anticipated was the strong momentum carried into the third quarter. The expansion was tracking at a roughly 3% annualized pace prior to the devastation caused by Hurricanes Harvey and Irma, and while the third quarter numbers will reflect the impact of the storms subsequent quarters should reveal a strong rebound.

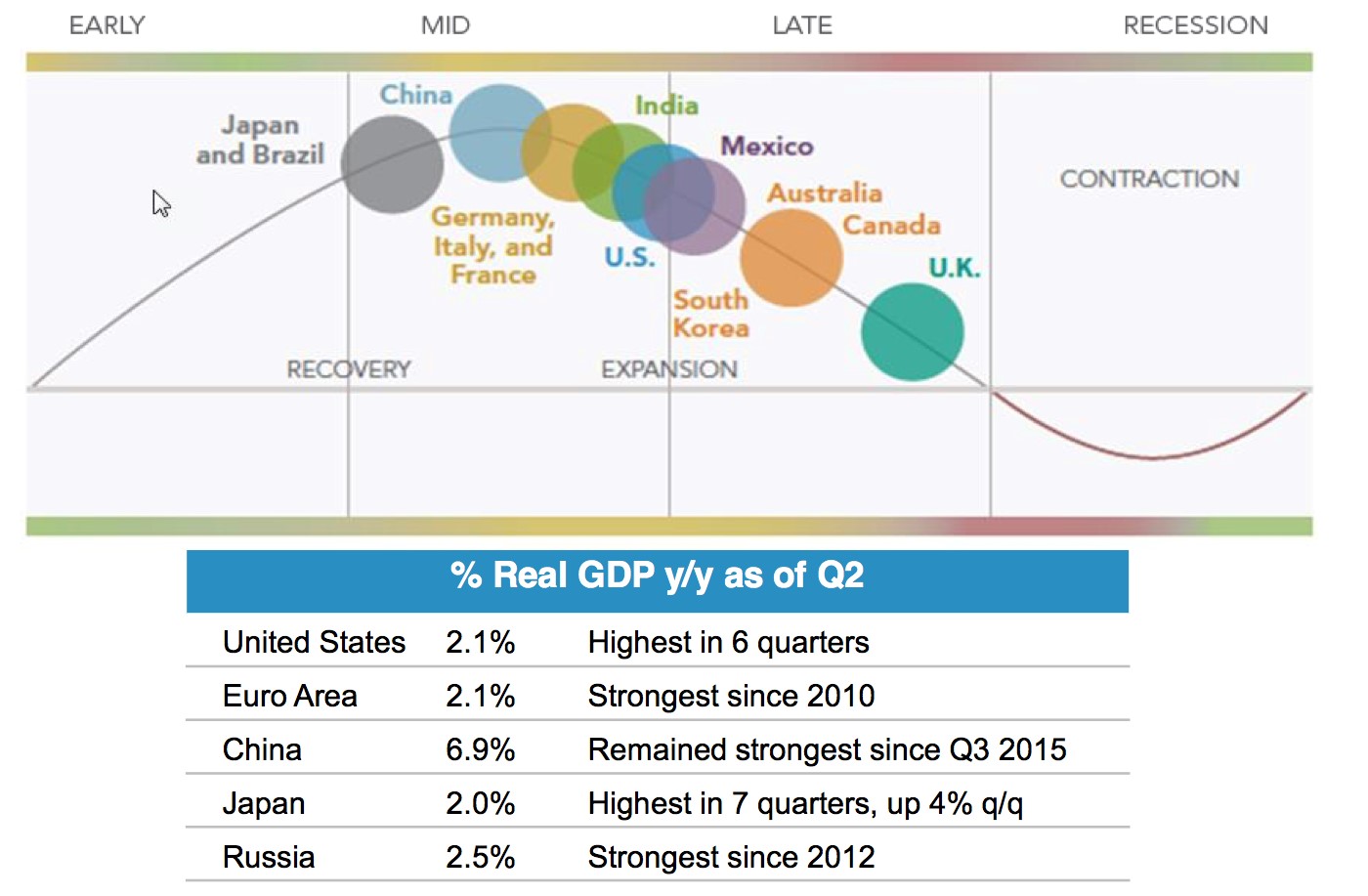

Overall the broadening and strengthening economic expansion around the world is bullish for the investment markets. Global growth in the first half of 2017 averaged 3.5% - the best start since 2014 - and importantly the composition of growth has shifted to a more self-sustaining dynamic of rising domestic demand and consumption accompanied by an uptick in global trade. The below chart reveals the synchronized nature of the current expansion, with all major economies in mid-cycle growth mode. This improved economic momentum, which has been supported by accommodative monetary and fiscal policies, should allow global economic growth to maintain its 3.5% pace for the remainder of 2017 and into 2018.

Equity Market Overview

On October 9, 2007, ten years ago to the day as we write this letter, the S&P 500 set a record closing high of 1,565. That record would stand for over five years. In the weeks following that record-setting day third-quarter earnings results from the big banks began to reveal huge write-offs of mortgage-backed securities, precipitating the financial crisis and the crushing bear market that would cut the value of the index by 57% over 17 months. We see no clear parallels to be drawn between then and now except that stocks have made 43 new highs in 2017 including six in a row in early October. We are reminded of the adage that warns us “no one rings a bell at a market top.”

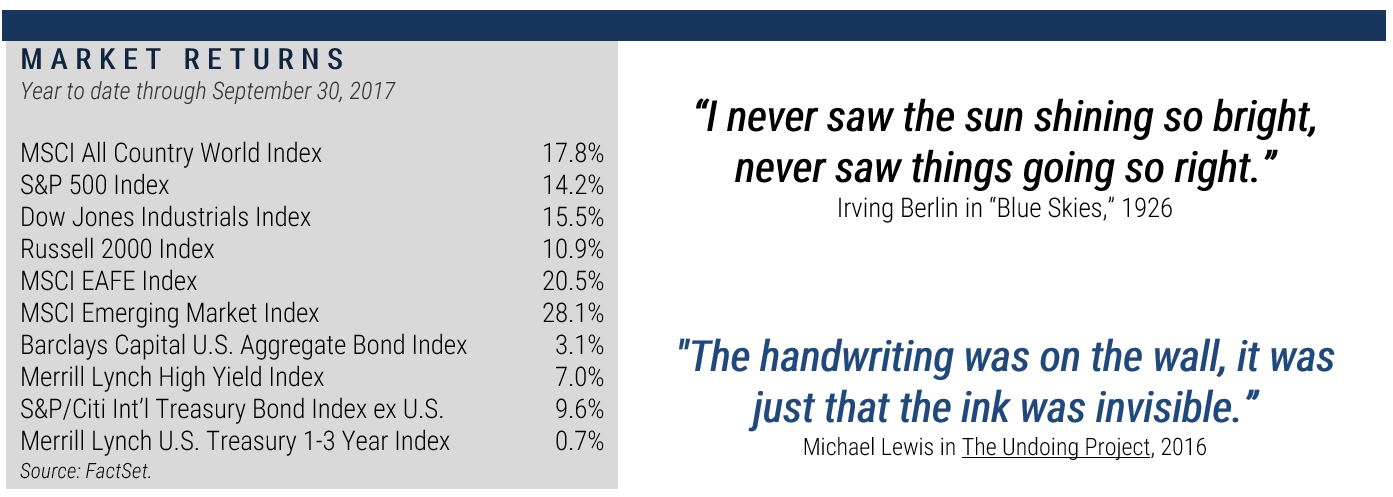

The S&P 500 closed out the third quarter by posting a positive monthly total return for the eleventh straight month. The last negative monthly return for the S&P 500 was in October 2016 when it declined 1.8%. The market index rose 2.1% in September, bringing its quarter-to date and year-to date total returns to 4.5% and 14.2%, respectively. The Dow Jones Industrial Average was up 5.6% in the third quarter, while the technology-heavy NASDAQ 100 Index enjoyed a total return of 6.2%.

Non-U.S. equities continued to lead, with the emerging markets again outperforming all other asset classes. The performance of foreign markets is attracting attention from many investors who reduced their allocations while those geographies were out of favor, and international equity mutual funds have experienced massive inflows this year. European stocks began the year amid uncertainty about the rise of populism and the viability of the European Union, and as political risk has subsided and earnings have improved investors have rotated back into those markets. Counter to almost all predictions at the beginning of the year the stabilization and stronger growth in both developed and emerging economies have led most foreign currencies to strengthen versus the dollar in 2017, providing additional tailwinds for U.S. investors holding foreign assets.

The table below details the performance of various market segments. Our tactical equity portfolio tilts to small-cap and value stocks generated mostly positive results for the third quarter and the past year. The small-cap tilt has added to performance as U.S. small companies represented by the Russell 2000 index rose 5.7% for the quarter and are up 20.7% over the last 12 months versus the Russell 1000 index of large-cap stocks, which has returned 4.5% and 18.5% for the quarter and 12-month period. The value tilt has added to performance in overseas markets where value has outperformed growth by over 7% in the past 12 months (MSCI EAFE Value Index up 23.2% vs. MSCI EAFE Growth Index up 16.1%) but growth stocks continue to lead in the U.S.

As we discussed above the fundamentals driving the equity markets remain positive. Second quarter earnings for S&P 500 Index companies increased 19% from the same quarter one year ago, marking the third quarter in a row of growth close to 20%. Full year earnings (last four quarter total) were also up about 18% versus one year ago. Most analysts remain bullish about the momentum in the corporate earnings environment, predicting more good news in the form of 15% growth versus the same period a year ago when the third quarter 2017 results are released in coming weeks. With the economic and earnings pictures looking so good our concern is that the markets are overextended and complacent and therefore vulnerable to a negative surprise or downward revision in the outlook. We will look at that idea through two lenses, volatility and valuation.

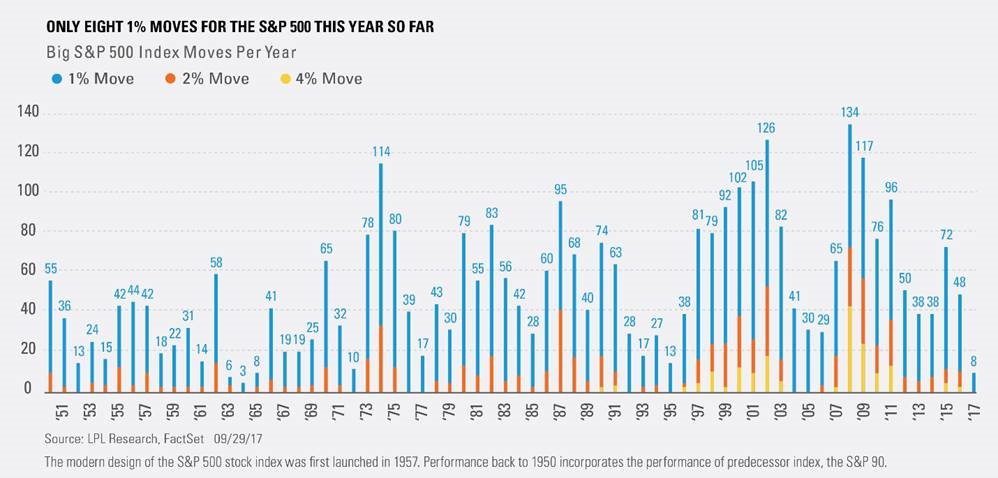

Volatility is a statistical measure of the dispersion of returns for the market, or more simply a measure of how much the market moves up and down in response to news or changing sentiment. High volatility indicates that investors are nervous and responding to news, while low volatility indicates complacency. The chart below courtesy of LPL Research indicates that 2017 has been one of the least volatile years in history with only eight intra-day moves of 1% for the S&P 500 index, the least since 13 in 1995. Only 1963 and 1964 saw fewer.

While the market moves up or down 1% many times in most years, we also normally see at least a few bigger intraday changes, with 2% to 4% moves not uncommon. The market has not had a single day in 2017 where the index rose or fell 2% or more, and according to LPL Research the last time the S&P 500 moved at least 4% was nearly six years ago.[3] To put the current low-volatility environment in context the S&P 500 had four consecutive days with 4% or larger swings in August 2011. Obviously low volatility on its own is not a problem; our concern is that after eight years of steadily rising stock prices investors have forgotten about risk. Investment advisor Charlie Bilello related on his Pension Partners blog that he had been asked by a client if it was safe “to park some money” in the S&P 500 “for a few months.” Bilello says the steady, low volatility ascent of the stock market has given investors the impression the index is “the new money-market fund.” “Hardly,” he replied. “The absence of risk does not mean the elimination of risk, just as the absence of rain does not mean there will never be another storm.” [4]

While volatility measures help us assess the mood of the market, fundamental valuation metrics gauge how much investors are willing to pay for a dollar of earnings, dividends or cash flow. Valuation analysis is far from perfectly predictive in the short term but there is a strong negative correlation between current valuations in the stock market and future returns. Logically enough buying stocks or the market indexes when valuations are low generally leads to higher returns. Analysts use a variety of ratios in their assessment of how expensive or attractive the market is, and the most commonly cited is the Price/Earnings ratio.

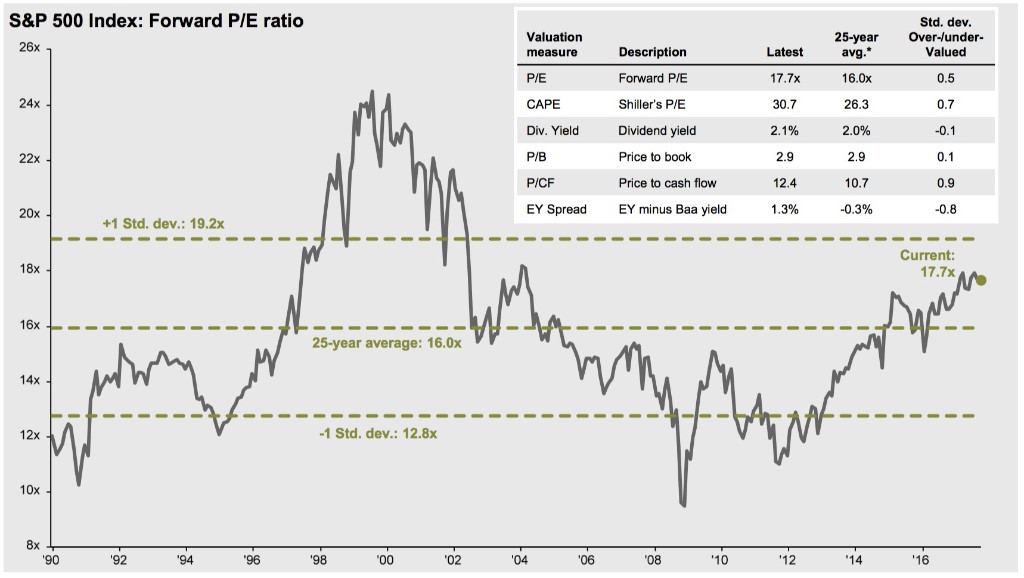

The chart below from J.P. Morgan Asset Management reveals that the S&P 500 is trading at 17.7 times the expected earnings for the index over the next 12 months. That valuation is not in bubble territory like the late 90’s but it is expensive relative to history and is based upon earnings estimates that reflect all of the good news that we’ve discussed.

For stocks to continue rising the economic fundamentals will need to keep improving and corporate earnings will need to meet or exceed the markets’ expectations. Those will be challenging hurdles and the market has very little margin for error given today’s Goldilocks environment. As we mentioned above and will discuss more below interest rates are an vital component of P/E multiples. When interest rates are low bonds are relatively unattractive so investors are willing to pay higher prices for stocks.

Comparing the dividend yield for the S&P 500 today, which the chart reveals is 2.1%, with the current yield of 2.3% on the 10-year Treasury note, we can see that those two alternatives are roughly equal for an income investor. Consider how much less attractive that 2.1% dividend yield would be if the yield on the Treasury Note were 3% or even 4%, well within its long-term average range. Our takeaway from this analysis is that stocks are expensive at a time when economic expectations and corporate earnings are particularly strong, interest rates are low and possibly headed higher, and complacency about risk is high.

Bond Market Overview

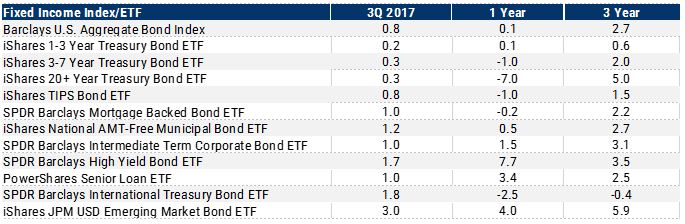

Our bond portfolio positioning continues to be defensive, focused on diversification, income generation, and capital preservation. At today's low yields bond investors may not be adequately compensated for the interest rate risk engendered by the strengthening global economy, policy tightening expected under the Fed's balance sheet reduction plan, and global tapering of QE. Yields spiked after the election last November as investors bet that Trump’s tax reform, infrastructure spending, and deregulation agendas would create a surge in growth and inflation. As the agenda stalled the “reflation trade” unwound, and interest rates have returned to levels close to those before the election.

Reviewing the third quarter, the 10-year Treasury note finished at a 2.3% yield, exactly where it began. The selloff in the bond market at the end of the second quarter continued into early July but reversed when the benign inflation numbers moderated the hawkish tone of central bank rhetoric. Yields then slipped lower in August on safe haven buying driven by North Korea’s missile launches, but reversed course again in September as investors’ appetite for risk returned. The Barclays U.S. Aggregate Bond Index rose 0.8% as the credit segment of the index continued to outperform. Investment grade and high yield corporate bonds saw seemingly insatiable demand from investors seeking income, and the momentum trade driven by strong recent returns probably added to the demand for corporates. For the quarter the Barclays High Yield Corporate Index was up another 2%, bringing the year-to date results to 7%. Yield spreads relative to Treasuries narrowed more for all credit-related sectors and are close to record lows. Emboldened by low corporate default rates and improving corporate earnings and balance sheets, investors are willing to buy bonds with less incremental return for the risks they’re taking. Again the market is operating with a very slim margin for error.

Now the Fed Open Market Committee (FOMC) is faced with a policy quandary created by stubbornly low inflation on one hand and a desire to normalize monetary policy on the other. As we learned after the September FOMC meeting Fed Chair Janet Yellen stands firmly on the side of tightening despite the weak inflation numbers, and an overstep by the Fed is an important risk.

Wage growth has stayed below 2.5% for more than two years, and the CPI index measuring the year-over-year change in prices for goods and services has been in a downward spiral since January. The Fed’s current estimate for 2017 inflation is 1.5% and the last time the U.S. experienced inflation at the Fed’s 2% target rate was in 2012. Even so the Fed has already implemented four rate hikes since 2015 and appears increasingly likely to hike again in December, which would be its third this year. It also plans three more increases in 2018. This month the Fed will begin unwinding its $4.5 trillion balance sheet, effectively raising the cost of long-term debt for consumers and businesses. Of course Fed officials are aware of the risks that come with tighter monetary policies, but the level of support provided by central banks since 2009 is unprecedented, so there is no playbook to guide its removal. If the global economy continues to improve central bank policy will become an even bigger source of uncertainty and risk for fixed income investors, and by extension investors in all other asset classes where valuations are linked to bond yields.

Summary

Given the bullish consensus view on the global economic fundamentals our chief concern is that the positive economic and earnings news is already priced into the markets. High valuations suggest that asset prices may be ahead of fundamentals, and support from central banks has provided liquidity to fill the gap. That liquidity has allowed the markets to shrug off political, geopolitical and fundamental risks and deliver the strong, consistent, low volatility returns that we’ve enjoyed in 2017.

The most important question facing investors now is how the global economy and markets will respond to the end of the extended period of central bank support. If the current economic momentum is sustained the fundamentals could improve quickly enough to validate current asset prices and drive them higher. In fact historical data indicate that some of the strongest returns in the stock market occur in the final stages of an economic recovery. However if economic and earnings growth fail to validate recent market performance then valuations will likely contract and asset prices will converge down to meet the fundamentals, with the risk of an overshoot in the markets that would weaken the global economy and trigger a downward cycle.[5] With most assets priced for perfection (or at least continued strength) any glitch or missed estimate will be magnified in the markets’ response.

From a portfolio management perspective our only answer to the questions raised in this letter is to be sure that each portfolio is aligned with our clients’ needs. Over the long term stocks remain the asset class of choice for wealth creation, but for many clients capital preservation is a primary objective. Even in growth oriented portfolios we are investing new money cautiously with risk management in mind. We’re confident that at some point volatility will increase creating an opportunity to invest more aggressively. Asset allocation policy is the tool we use to address our clients’ needs and goals, and the mix of stocks, bonds, and cash will always be the most important decision we make. The only way for us to make good allocation decisions is to communicate with you, so we look forward to a conversation in the near future!

Wayne F. Wilbanks, CFA

Lawrence A. Bernert III, CFA

D.J. Kyle Elliott, CFP

Mark R. Warden

Roger H. Scheffel Jr., CPA, PFS

Thomas F. X. McNally, CMT, CFA

Wade A. Monroe, CIMA

Paul A. Ferwerda, CFA

Dan F. Powell, CFA, AIF

[1] Low Volatility Is Here To Stay, Byron Wein, Blackstone Market Commentary, October 2017

[2] The Bull Market In Everything, The Economist, October 7, 2017

[3] https://lplresearch.com/2017/10/02/where-did-all-the-big-moves-go/

[4] Randall W. Forsyth, “The Melt up Before the Storm?” Barron’s, October 7, 2017

[5] http://www.wealthmanagement.com/fixed-income/mohamed-el-erian-investing-journey-not-destination

Unless otherwise indicated, performance information for indices, funds and securities is sourced from FactSet as of September 30, 2017. This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC that are subject to change and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable, but cannot be guaranteed for accuracy. Some portions of this letter were written in conjunction and collaboration with Capital Markets Consultants Inc. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. It is made available on an "as-is" basis without warranty. There are no guarantees investment objectives will be met.

This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC and are subject to change from time to time, and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty. There are no guarantees investment objectives will be met.

The information contained herein has been obtained from sources believed to be reliable, but cannot be guaranteed for accuracy. Some portions of this letter were written in conjunction and collaboration with Capital Markets Consultants Inc. Past performance is no guarantee of future results.

Market indices are unmanaged and do not reflect the deduction of fees or expenses. You cannot invest directly in an index such as these and the performance of an index does not represent the performance of any specific investment strategy. We consider an index to be a portfolio of securities whose composition and proportions are derived from a rules based model. Market indices are unmanaged and do not reflect the deduction of fees or expenses. You cannot invest directly in an index such as these and the performance of an index does not represent the performance of any specific investment strategy.

The S&P 500 Index is a market capitalization weighted index, including reinvestment of dividends and capital gains distributions that is generally considered representative of U.S. stock market.

The Dow Jones Industrial Average (DJIA) is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange (NYSE) and the NASDAQ.

The MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI ex USA Index is designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies

The MSCI EAFE Index is a stock market index that is designed to measure the equity market performance of developed markets outside of the U.S. & Canada. It is maintained by MSCI Barra, a provider of investment decision support tools; the EAFE acronym stands for Europe, Australasia and Far East.

The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. EM countries include: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Russia, Qatar, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates. With 845 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The Russell 2000 index measures the performance of the 2,000 smallest companies in the Russell 3000 index.

The Bloomberg Barclays U.S. Aggregate Bond Index covers the USD-denominated, investment-grade, fixed-rate, taxable bond market of SEC-registered securities. The index includes bonds from the Treasury, Government-Related, Corporate, MBS, ABS, and CMBS sectors.

The BofA Merrill Lynch U.S. High Yield Index tracks the performance of U.S. dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million. The BofA Merrill Lynch 1-3 US Year Treasury Index is an unmanaged index that tracks the performance of the direct sovereign debt of the U.S. Government having a maturity of at least one year and less than three years

The S&P/Citigroup International Treasury Bond ex-U.S. Index measures the performance of treasury bonds, with maturities greater than or equal to one year, issued by non-U.S. developed market countries.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.