WST 2Q 2017 Commentary

We hope your summer is off to a good start. Even in this world of always-on communications, texts, tweets, emails, etc., the long days of late June and July have a special feel, and we hope you’re able to pause and enjoy them. With the pace of life slowing just a bit the midpoint of the year is a good moment to review the big picture and to take stock of progress. From an investment perspective that means refocusing on long-term goals and assessing portfolio strategy and performance to be sure we’re on track toward those goals. Midyear is also an appropriate time to reflect on what we expected during 2017 when we wrote our December 2016 letter and to consider how any surprises from the first six months might affect our view and strategy. Some of our forecasts were spot on (stocks over bonds and the continued rally in international and particularly emerging markets equities) while others haven’t turned out as expected (continued outperformance of large cap growth stocks over value and small cap stocks). Over the course of this letter we’ll review the progress of the economy and markets in the first half of 2017 and look ahead at the factors impacting our strategy and allocations. As always the most important consideration in portfolio construction is each clients’ individual financial situation, so communication is the key to success.

We hope your summer is off to a good start. Even in this world of always-on communications, texts, tweets, emails, etc., the long days of late June and July have a special feel, and we hope you’re able to pause and enjoy them. With the pace of life slowing just a bit the midpoint of the year is a good moment to review the big picture and to take stock of progress. From an investment perspective that means refocusing on long-term goals and assessing portfolio strategy and performance to be sure we’re on track toward those goals. Midyear is also an appropriate time to reflect on what we expected during 2017 when we wrote our December 2016 letter and to consider how any surprises from the first six months might affect our view and strategy. Some of our forecasts were spot on (stocks over bonds and the continued rally in international and particularly emerging markets equities) while others haven’t turned out as expected (continued outperformance of large cap growth stocks over value and small cap stocks). Over the course of this letter we’ll review the progress of the economy and markets in the first half of 2017 and look ahead at the factors impacting our strategy and allocations. As always the most important consideration in portfolio construction is each clients’ individual financial situation, so communication is the key to success.

At risk of overdoing the weather symbolism the financial markets enjoyed a mild spring in 2017. The global economic climate remained balmy, the dark clouds on the horizon seemed distant and unthreatening, and the occasional squalls passed quickly. Positive fundamentals supported the benign disposition of investors around the world and sentiment remains strong as the synchronous global economic expansion continues. Optimism generally prevails in the U.S. where hopes for tax reform and the boost in fiscal spending promised by the Trump administration remain despite legislative and political challenges. For now European economies are buoyed by support from the European Central Bank, although as we discuss below ECB president Mario Draghi’s statement in late June that “deflationary forces have been replaced by reflationary ones” may be a turning point in policy. Still, even that hawkish comment can be interpreted as positive from a fundamental standpoint because it reflects the new-found strength of the European economy. Eurozone business and consumer sentiment jumped to its highest level since before the financial crisis according to a survey released during the last week in June, and even Japan seems to be turning the corner with growth boosted by the weaker yen and the generally strong global environment. China, the world’s second largest economy and the source of much concern among economists and investors 18 months ago, is benefiting from financial liberalization measures and should and grow 6-7% this year.

With global growth and trade near multi-year highs, stock markets around the world enjoyed their best first half in years. It was all gain and no pain as 26 of the world’s 30 biggest markets rose in the first half, among the five best first-half rallies in the past 20 years according to an analysis by the Wall Street Journal.[1] Investor confidence, and perhaps complacency, are revealed by the markets’ low volatility. The average intra-year decline in the S&P 500 is 14.6%,[2] but it’s been over a year now since the market experienced even a 5% drop. “Smooth seas do not make skillful sailors,” according to an old proverb quoted in Barron’s by Brian Singer of William Blair & Co., and while the economic outlook is good and the likelihood of recession is low, investors’ current willingness to shrug off risk is unusual. Events that might be expected to shatter the calm, for example the appointment of a special counsel to investigate allegations of corruption related to the presidential election, North Korea’s nuclear threat, and terrorism in Europe have passed with barely a blink from the markets. As we discuss below the only factor to awaken investor anxiety this year has been concern about central bank policy.

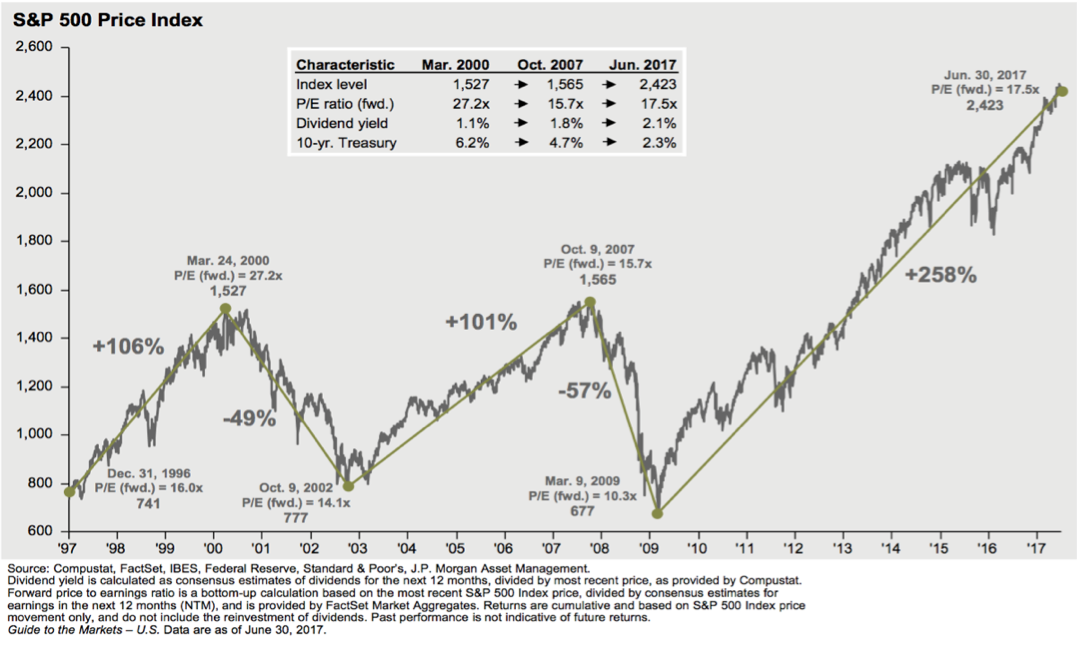

J.P. Morgan’s chart above of the S&P 500’s 20-year performance is one of our favorites, and the story it tells is straightforward: since the low in March of 2009 the U.S. stock market has almost tripled in value with only minor corrections and pauses along the way. That long stretch of strong returns and low volatility doesn’t suggest that a decline is imminent, but it does open the door to a discussion about return expectations in the context of asset allocation. Building portfolios with the right mix of stocks and bonds to meet a client’s needs for growth while appropriately limiting risk is the biggest challenge we face. The time to prepare for the inevitable return of volatility is now. We’ll return to that discussion after an overview of the economy and market performance.

Economic Overview

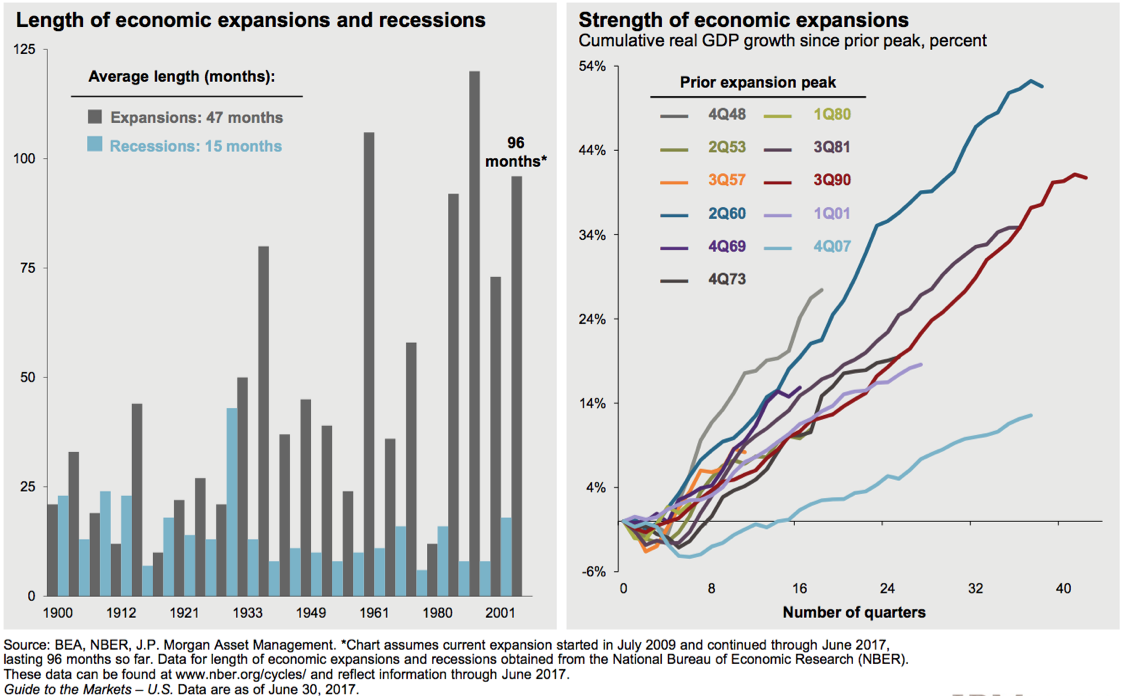

With global growth in a cyclical upturn the U.S. economic expansion remains on track, and first quarter real GDP growth was officially confirmed at 1.4% when the final revisions were made, up from earlier estimates of 0.7% and 1.2%. In what has become an annual occurrence the year got off to a slow start due to temporary seasonal factors that are expected to reverse and reveal a rebound to around 2.5% on an annualized basis when the government releases its first official estimate of second quarter growth on July 28th. The consensus estimate for the pace of growth in the U.S. for the full year is above the economy’s estimated longer-term growth rate of around 2.0%, but remains far from the 4% rate once projected by the Trump administration. As the third quarter unfolds questions about the strength and longevity of the current expansion will remain central to investor concerns. GDP growth ultimately drives corporate earnings, and the path of Fed policy will be determined by the FOMC’s views on growth and inflation. As its stands we’re 96 months into this expansion, third longest in history, but it’s by far the least vigorous recovery on record.

In previous letters we’ve written about the headwinds facing the U.S. economy including, most importantly, lackluster consumer spending and the unwillingness of corporations to unleash the capital investments that their strong balance sheets would support. At this point in the economic cycle most of the pent-up consumer demand from the financial crisis has been satisfied. Housing and related expenditures remain an exception and still have plenty of room to run, but achieving another cyclical spurt in consumer spending will be difficult given the mature economic cycle. Looking ahead, consumer spending growth will be driven by underlying wage gains and will likely grow in the 2%-2.5% range, a healthy pace and in line with overall GDP growth but below the 3% pace enjoyed in 2014-16. Frugality is in style among consumers just as it has been since the financial crisis. The household savings rate stands at 5.5% today versus 2.2% during the housing bubble,[3] and many families are holding back on discretionary purchases because of rising health insurance premiums, burdensome student loans, and lack of confidence in the stability of their jobs. The gap between consumer confidence, which is rising with the strong job market, and consumer spending continues to widen.

The improving global growth outlook and the strong housing market are driving gradual improvements in U.S. manufacturing activity and investment. Business investment accelerated at an 11.4% annualized rate in Q1 due to a rebound in the oil and gas sector and spending on equipment and software. While Q2 investment won’t match that rate, it is expected to have sustained a healthy pace of about 4% in real terms. That would represent a marked improvement over recent years and should help improve productivity growth. The manufacturing sector has gained traction as spending on durable goods like machinery and computers has rebounded after a weak stretch in 2015 and 2016. The month-to-month data is uneven reflecting the surge of optimism that followed the presidential election and the subsequent realization that big infrastructure projects and tax reform will take time to achieve. Very importantly the expectation of incremental deregulation appears already to be driving growth at small and midsize companies through increased investment and lending.

Central Bank Policy – Actions Speak Louder Than Words

Paradoxically the strengthening global economy is the root of the most immediate risk to the investment markets, and that is the possibility of a misstep or overstep as central bankers begin normalizing monetary policy after almost a decade of easy money. We tasted volatility during the last week of June when Draghi’s comments, along with similar statements by officials at the Federal Reserve, the Bank of England, and the Bank of Canada sparked investor fears of an imminent shift in central bank policies. The Fed said the market can expect “gradual adjustments in the stance of monetary policy” as it continues down the path of “balance sheet normalization,” and Draghi’s statement renewed concern about the ECB’s policy path. Together their comments raised concerns the Fed will raise rates too fast and the ECB will taper its asset purchases too soon, removing the massive liquidity support that began in the wake of the financial crisis in 2008 and 2009. Those concerns led to a selloff in the bond market that bled over into the global equity markets, inducing a spike in volatility in the final days of June that has continued into July. Investors fear an echo of the “taper tantrum” that shook the U.S. bond market in 2013 amid indications the Federal Reserve was slowing its bond-buying program. With Central Bank interest rate policies and asset purchase programs having fueled the economic recovery for years, it’s understandable the markets are unsettled by the prospect of tighter policies.

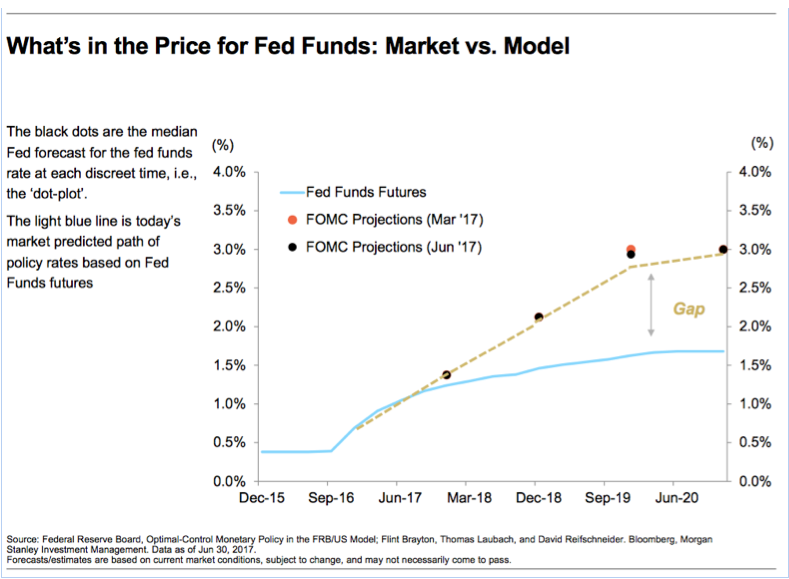

While the Fed has been raising rates based upon the tight labor market and other indications of strength, the market remains skeptical. Inflation remains well below the Fed’s 2% target range and as Nelson Schwartz pointed out in the New York Times “the promise of faster economic growth has become a study in the triumph of hope over experience.” The following chart reveals the gap between the Fed funds futures, which reflect the market’s predictions about the direction of interest rates, and the rate of increases the Fed is publicly projecting with its dot plots. The market anticipates a more dovish Fed than its guidance suggests. Central banks in general have proven responsive to the evolving data on the health of the global economy, and we’re hopeful and optimistic they’ll remain supportive and take measured steps along the path to policy normalization.

Equity Market Overview

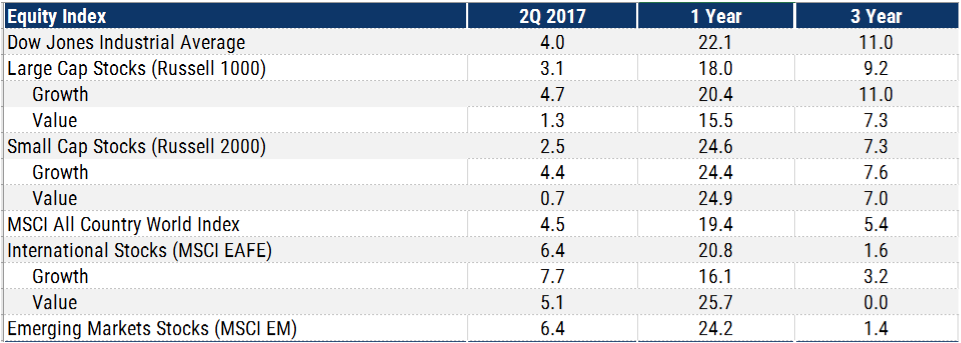

The Dow, S&P 500 and NASDAQ all set new records in the second quarter as improving corporate earnings trumped the new administration's legislative challenges. Investors began the year with high hopes for tax reform, deregulation, and a surge in infrastructure spending, none of which materialized in the first six months of 2017. However, accelerating earnings growth in the U.S. and abroad shifted the focus (temporarily at least) from the macroeconomic and policy perspectives to a bottom-up assessment of improving corporate fundamentals, and drove the markets higher. The final revisions to the first-quarter earnings numbers for the S&P 500 revealed a 14% increase over the first quarter of 2016, the best performance since 2011, and estimates for the remainder of 2017 and 2018 now call for double-digit EPS growth through the end of next year. The news was equally good in other parts of the world including Asia Pacific (ex-Japan) and Europe as corporate earnings expanded at double-digit rates in the first half of the year.[4] Money flows into global stocks reveal continued strong investor interest this year with passive investment vehicles like index funds and ETFs seeing the largest inflows.

The sunny economic climate and strong corporate performance lifted the S&P 500 3.1% during the quarter, bringing its year-to-date total return to 9.3%. The Dow rose 4.0% in the quarter and matched the S&P 500’s year to date number. The technology heavy NASDAQ 100 Index has enjoyed a total return of 16.8% this year.

Mid- and small-cap stocks lagged large-cap stocks in the quarter but still posted positive total returns. The Russell Mid-Cap Index rose a solid 2.7% in the quarter and the Russell 2000 Index of small company stocks rose 2.5%, bringing their year-to-date total returns to 8.0% and 5.0%, respectively.

Growth maintained its edge over Value in the 2nd quarter. The Russell 1000 Growth Index had a total return of 4.7% while the Russell 1000 Value Index came in at 1.3% for the quarter. Similar margins were seen in the Russell Mid Cap and Russell 2000 Growth and Value indexes. Sector performance drove the style divergence as Health Care and Technology are weighted more heavily in Growth indexes. Financials performed better this quarter but weakness in Energy and Telecommunications weighed on results. We stand firmly behind our style tilts of Value and small cap as continued economic expansion combined with reasonable expectations of growth within these market segments should turn the 1st half laggards into market leaders in the quarters ahead.

Stocks outside of the U.S. in both developed and emerging markets remained the sweet spot for equity investors during the second quarter. The MSCI EAFE rose 6.4% bringing its year-to date return to 13.8%, and the MSCI Emerging Markets Index rose 6.3% for the quarter and is up 18.4% for the year. Foreign stocks were out of favor for several years and we’ve written at length about the importance of discipline in maintaining a diversified portfolio. Even as 2017 began analysts looking at non-U.S. equities were concerned about the health of the Chinese economy, the viability of the Eurozone as a populism spread across the continent in the wake of the Brexit vote in Great Britain, and the likelihood of higher interest rates and a stronger dollar in response to Trump’s aggressive spending plan. As it turned out China has improved as it transitions from investment to consumption-led growth and the Eurozone looks stable in light of Emmanuel Macron’s victory in France. Most surprisingly, the improving economic situation around the world coupled with concern that the Fed will stall U.S. growth by tightening too fast led to the worst stretch for the dollar in six years during the first half of 2017. Each of these forces was a tailwind for foreign stocks, and both developed and emerging market equities have outpaced U.S. stocks over the past quarter, six months and year. Even so, as the returns table on the previous page reveals, foreign equities have a large gap to fill before their three-year returns are in line with domestic stocks. We are maintaining our allocations to foreign stocks and expect them to continue to be a key driver of returns within equity portfolios.

Looking ahead our primary concerns for the equity markets are the obvious ones. Stock valuations, while not extreme, are high by historical standards, and if interest rates rise stocks will be less attractive to income investors as dividend yields on equities will decline relative to bond yields. The dynamic between economic growth, corporate earnings, and central bank policy around the world will be the most important variable for equity investors in the second half of the year.

Bond Market Overview

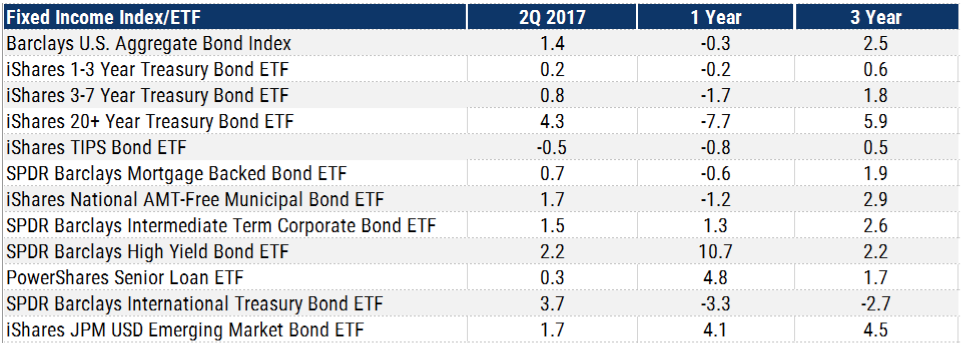

Bonds pivoted in the second quarter as last year’s “reflation trade” in the fixed income markets reversed. Interest rates rose after the presidential election because investors expected faster growth and higher inflation under Trump, but declined during the second quarter as the pro-growth policy initiatives slid into a political quagmire. Despite the flurry of comments from central bankers at the end of June the fixed income markets are now pricing in continued low inflation, and while the sentiment shift during the quarter was driven partially by the Trump administration’s inability to implement its policies on tax reform and fiscal spending, the most recent data reveal stubbornly low CPI despite the apparent vigor of many parts of the economy. Last quarter we wrote that the Fed’s path and the direction of interest rates would be dependent upon the success of the Trump economic agenda and the path of the economy. We indicated the timing of fiscal stimulus would be an important factor, and the upward pressure on interest rates from higher growth and expectations about government stimulus would be balanced by uncertainty about the timing and success of the agenda. That guidance remains appropriate, and while the implementation of Trump’s growth agenda has been delayed we believe the decline in yields during the second quarter, particularly on the long end of the yield curve, leaves long maturity bonds unattractive and vulnerable to a pick-up in growth and inflation later this year. We continue to emphasize relatively short durations in our fixed income portfolios.

Looking at performance, the Barclays U.S. Aggregate Bond Index rose 1.4% in the quarter with its component returns ranging from virtually nil (0.2%) for 1-3-Year Treasuries to 4.3% for 20+ Year Treasuries. The benchmark U.S. 10-Year Treasury closed the quarter at a 2.31% yield, down slightly from March 31 and year-end 2016. These declines in yields occurred despite the Federal Reserve’s 25 basis point hike in June, and the flattening yield curve is an indicator we’ll watch closely. The Federal Reserve controls only the very short-term interest rates; the market sets rates further out. Seeing long term rates falling while short-term rates are rising tells us the market believes the threat of inflation is declining and the economy softening. The current situation in the fixed income markets suggests bond investors are not as optimistic about economic growth as are the Fed and equity investors.

Complacency and Calm Markets

In closing we return to the topics of market volatility, asset allocation, and complacency. Our colleagues at Dimensional Fund Advisors (DFA) recently highlighted the role communication between advisors and clients plays in ensuring portfolio allocations are aligned with the clients’ needs and expectations. Dimensional's 2017 Investor Feedback Survey, which polled almost 20,000 clients of 436 investment advisory firms around the world, revealed the greatest fear of almost 1/3 of investors is "experiencing a significant investment loss in a market downturn” a response second only to "not having enough money to live comfortably in retirement." (37%).[5] Those concerns frame the challenges we face in our role as advisors in guiding our clients and setting strategy in the current market environment. Given the paltry returns available on low risk investments like short-term treasury bonds, most investors need exposure to equities to have a reasonable chance of achieving their goals. However if “experiencing a loss” equates to seeing a decline in one’s portfolio value, then any client owning stocks will inevitably face a significant loss at some point in the market cycle.

Our task then is to establish investment policies that maximize the likelihood our clients achieve their objectives within a range of volatility and risk the clients can accept. Individual, family and institutional clients each have unique aspirations, fears, goals and concerns. Each of these attributes require attention. The process of setting policy requires us to understand not only our client’s current financial situation (assets, liabilities, income, and expenses) but also their time horizons and temperaments.

Communication and thinking about long term issues is inevitably influenced by current events. “Recency bias” leads us to believe that an event or outcome is more likely because it occurred in the recent past, and the longer it has been since an event took place, the less likely we are to believe it will happen in the near future. In today’s market environment of strong returns and low volatility recency bias has manifested as complacency: in this case the belief that the market will keep going up without a meaningful correction. We believe refocussing on our clients’ plans and tracking progress toward their goals is the best defense against complacency. The asset allocation targets we set for our clients’ portfolios reflect their long term goals and risk tolerance, and our short term or tactical management around those targets are based upon their time horizons and liquidity needs.

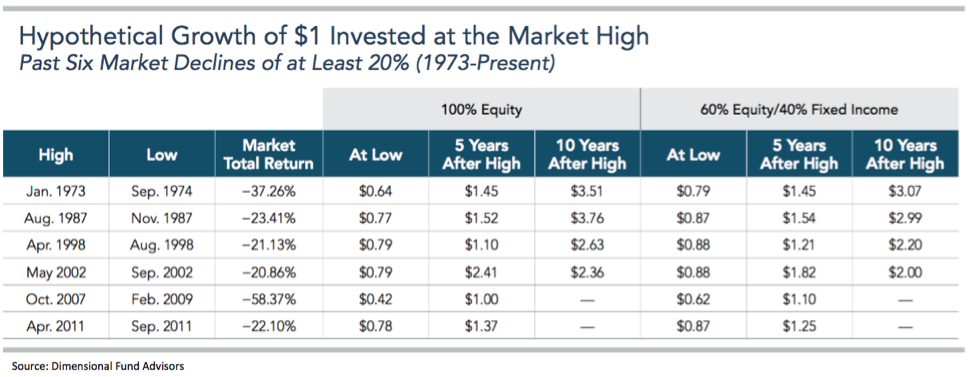

Knowledge is a powerful ally in effective investing. Certainly it’s important to acknowledge what is not knowable, including most importantly the direction of the markets in the short term. However, we believe history has taught two important lessons that guide intelligent investing, and together they form the foundation of our investment strategy and process. First, while stocks are volatile at times, global capitalism and the world’s equity markets have been remarkably resilient, and equities are the asset class of choice for long term wealth creation. The equity markets are calm now, but over just the past 20 years markets have seen precipitous declines following the bursting of the internet bubble and the global finacial crisis, not to mention the war on terror and a litany of other challenges. After each crisis stocks have recovered to post new highs. The second lesson is that diversification reduces portfolio volatility and allows skilled investors to set reasonble ranges of expectations for long-term returns while smoothing the ride in the short term. The table on the following page, courtesy of DFA, demonstrates both the resileince of the market after bouts of volatility and the benefit of diversification in reducing portfolio volatility.

The table shows how a hypothetical 100% equity strategy and a hypothetical 60% equity/40% fixed income strategy would have fared in the past six global stock market downturns of at least 20%. On average, a decline of this magnitude has occurred about once every seven or eight years since 1973 and the last occurrence was in 2011. The addition of bonds would have helped to mitigate the decline in the 60/40 strategy relative to 100% equity strategy; for example, during the 58% drop in stocks between October 2007 and February 2009 the 60/40 blend portfolio declined 1/3 less than the all-equity portfolio. For many investors that moment in time is a vague memory after nine years of good market performance, but we remember well the fear that gripped investors who saw more than half of their net worth erased in less than two years, and the reassurance felt by clients with appropriate allocations. So now, during this “perfect young summer,” is the time to “build barns” and be sure that portfolios are allocated to endure the next winter. To that end we look forward to a conversation or meeting soon.

Summary

As always we appreciate the opportunity to serve you and the confidence you’ve expressed in us. At $2.7 billion in assets under management, WST is the 88th largest Registered Investment Advisory firm in the country according to July rankings in Financial Advisor Magazine.[6] We understand that every dollar of that money is entrusted to us by clients who count on us to guide good decisions and help them achieve their goals. We’ll continue to work hard to earn that trust every day!

Wayne F. Wilbanks, CFA

Lawrence A. Bernert III, CFA

D.J. Kyle Elliott, CFP

Mark R. Warden

Roger H. Scheffel Jr., CPA, PFS

Thomas F. X. McNally, CMT, CFA

Wade A. Monroe, CIMA

Paul A. Ferwerda, CFA

Dan F. Powell, CFA, AIF

Unless otherwise indicated, performance information for indices, funds and securities is sourced from FactSet as of June 30, 2017. This newsletter represents opinions of Wilbanks, Smith and Thomas Asset Management, LLC that are subject to change and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable, but cannot be guaranteed for accuracy. Some portions of this letter were written in conjunction and collaboration with Capital Markets Consultants Inc. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. It is made available on an "as-is" basis without warranty. There are no guarantees investment objectives will be met.

[6] Financial Advisor Magazine, “2017 RIA Survey and Ranking,” http://www.fa-mag.com/financial-advisor-magazine/issues/2017/07.

[5] “Complacency and Calm Markets” (Issue Brief, Dimensional Fund Advisors, June 2017)

[4] Russolillo, Steven “Global Stocks Post Strongest First Half in Years, Worrying Investors,” The Wall Street Journal, June 30, 2017.

[3] Schwartz, Nelson, “Hopes of a “Trump Bump” For US Economy Shrink As Growth Forecasts Fade,” New York Times, July 6, 2017.

[2] “Guide to the Markets,” JPMorgan Research, July 2017, p. 12

[1] Russolillo, Steven, “Global Stocks Post Strongest First Half in Years, Worrying Investors,” Wall Street Journal, June 30 2017.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.