July 2021 | Global Equity Market Review

July was another positive month for U.S. equities, with the S&P 500 Index producing a total return of 2.38%. Broader market domestic indices lagged with S&P Mid Cap 400 Index returning just 0.35% and the S&P 600 Small Cap Index falling into negative territory for the month at -2.39%. The gap in returns between large and small cap indices was unusually wide in a rising market. This pattern reflects a sharp narrowing in market breadth, reminiscent of the early days of pandemic.

Cyclical sectors were hit especially hard during July with Financials and Energy sectors trailing more defensive sectors such as Health Care and Utilities. Leadership in economically sensitive sectors is rarely consistent, especially at moments of high uncertainty like now, with the economy still battling the COVID-19 virus. Further advances without support from cyclical sectors would indicate diminished confidence in the overall health of the economy and would not be not a healthy sign for the market overall. For now, the lack of participation among broad market benchmarks casts a shadow on a remarkable string of positive months in the S&P 500 Index.

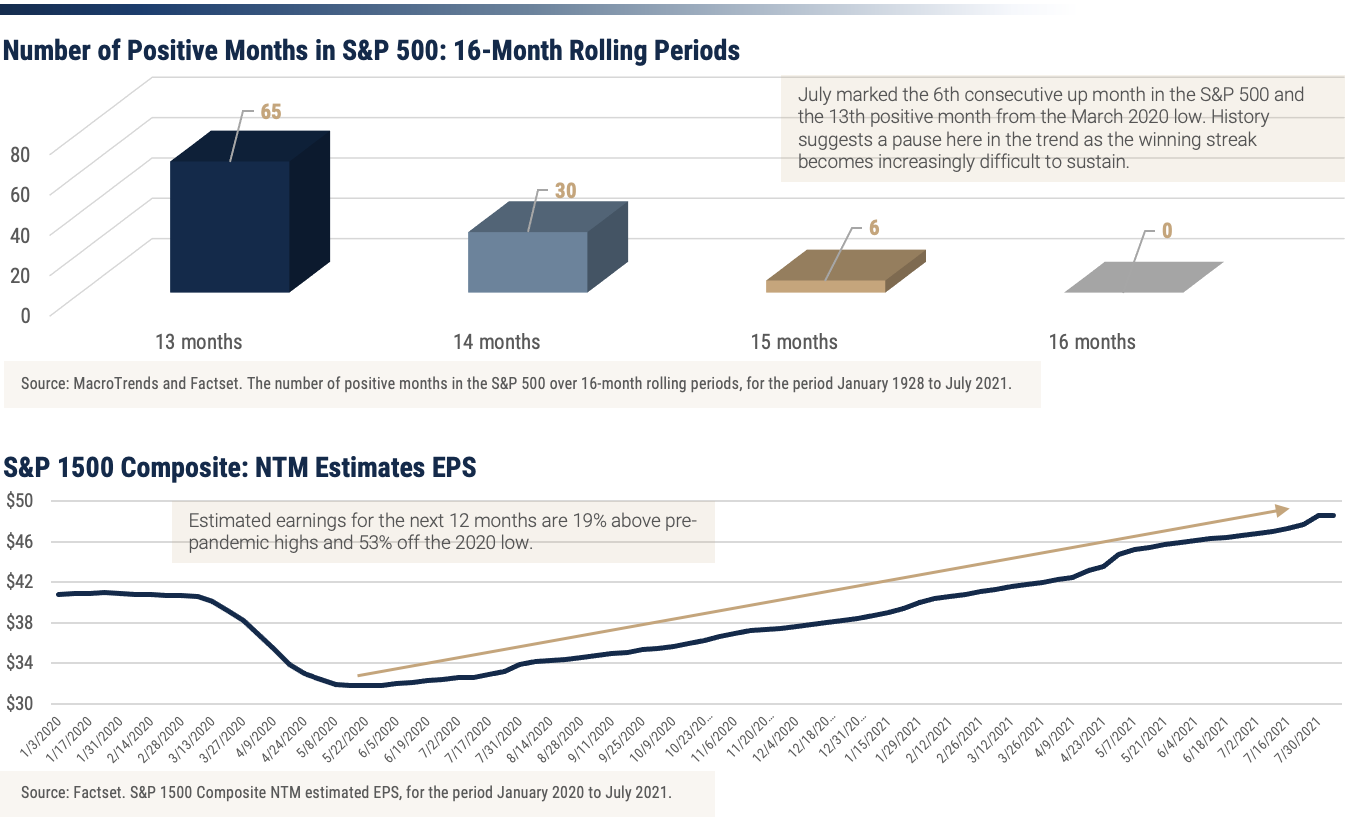

July marked the 6th consecutive positive month for the Index and the 13th advance in 16 months since the March 2020 low. As the below chart illustrates, continuing the winning streak over periods of this length becomes increasingly rare and unlikely in the face of narrowing leadership. The cumulative price gain in the S&P 500 over the past 16 months adds to the challenge with a 70% advance — the largest such gain in 85 years.

One clear positive for the market continues to be earnings. Estimates have been rising sharply and widely for companies making up U.S. indices. With the 2nd quarter earnings season coming to a close, the advance is remarkable as seen in the chart above. Earnings forecasts for the next year are already well above the level before the onset of COVID-19 and have advanced sharply off the 2020 low. Release of pent-up demand, as well as perhaps a pull forward of future demand, are contributing to the impressive results. However, cost pressures from labor and materials are evident in management’s narrative during quarterly earnings calls and the ability to sustain the impressive earnings rebound will become more difficult in the coming quarters. For now, equity investors are moving stocks higher and pushing aside potential risks of sustained price pressures on earnings and downside risk of the Delta variant on the economy.

International markets trailed most U.S. benchmarks in July with the S&P Developed ex-U.S. Index up 0.40% and the S&P Emerging Index down 5.98%. Highlights were in many developed European markets while weaker areas of the world were seen in emerging markets including Latin America and Asia. After a strong run-up in the dollar in June, the dollar was relatively quiet in July, retreating slightly from end-of-June levels. This performance gap is not unexpected as a result of the narrow breadth of U.S. markets discussed above, differences in vaccination rates across the globe, and the continued major disruption of international shipping routes, especially between Asia and the U.S. We should observe better results versus domestic indices going forward and would note the valuation advantage in non-U.S. markets makes a compelling argument for patience.

Notes & Disclosures

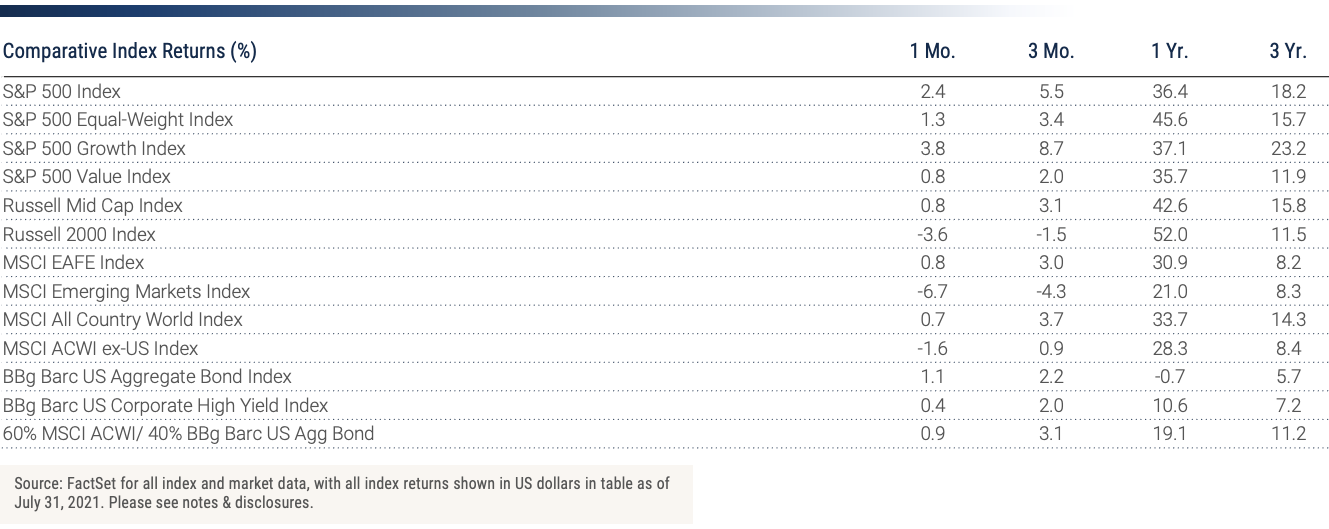

Index Returns – all shown in US dollars

All returns shown trailing 7/31/2021 for the period indicated. “YTD” refers to the total return as of prior-year end, while the other returns are annualized. 3-month and annualized returns are shown for:

- The S&P 500 index is comprised of large capitalized companies across many sectors and is generally regarded as representative of US stock market and is provided in this presentation in that regard only.

- The S&P 500® Equal Weight Index (EWI) is the equal-weight version of the widely-used S&P 500. The index includes the same constituents as the capitalization weighted S&P 500, but each company in the S&P 500 EWI is allocated a fixed weight - or 0.2% of the index total at each quarterly rebalance. The S&P 500 equal-weight index (S&P 500 EWI) series imposes equal weights on the index constituents included in the S&P 500 that are classified in the respective GICS® sector.

- The S&P 500 Growth Index is comprised of equities from the S&P 500 that exhibit strong growth characteristics and is weighted by market-capitalization.

- The S&P 500 Value Index is a market-capitalization weighted index comprising of equities from the S&P 500 that exhibit strong value characteristics such as book value to price ratio, cash flow to price ratio, sales to price ratio, and dividend yield.

- The Russell 3000 Index tracks the performance of 3000 U.S. corporations, determined by market-capitalization, and represents 98% of the investable equity market in the United States.

- The Russell Mid Cap Index measures the mid-cap segment performance of the U.S. equity market and is comprised of approximately 800 of the smallest securities based on current index membership and their market capitalization.

- The Russell 2000 Index is a market-capitalization weighted index that measures the performance of 2000 small-cap and mid-cap securities. The index was formulated to give investors an unbiased collection of the smallest tradable equities still meeting exchange listing requirements.

- The MSCI All Country World Index provides a measure of performance for the equity market throughout the world and is a free float-adjusted market capitalization weighted index.

- The MSCI EAFE Index is a market-capitalization weighted index and tracks the performance of small to large-cap equities in developed markets of Europe, Australasia, and the Far East.

- The MSCI Emerging Markets Index is a float-adjusted market-capitalization index that measures equity market performance in global emerging markets and cannot be purchased directly by investors.

- The S&P Global BMI sector indices are into sectors as defined by the widely used Global Industry Classification Standards (GICS) classifications. Each sector index comprises those companies included in the S&P Global BMI that are classified as members of respective GICS® sector. The S&P Global BMI Indices were introduced to provide a comprehensive benchmarking system for global equity investors. The S&P Global BMI is comprised of the S&P Emerging BMI and the S&P Developed BMI. It covers approximately 10,000 companies in 46 countries. To be considered for inclusion in the index, all listed stocks within the constituent country must have a float market capitalization of at least $100 million. For a country to be admitted, it must be politically stable and have legal property rights and procedures, among other criteria.

- The Barclay’s US Aggregate Index, a broad-based unmanaged bond index that is generally considered to be representative of the performance of the investment grade, US dollar-denominated, fixed-rate taxable bond market.

- The Bloomberg Barclay’s US Corporate High Yield Index, which covers the USD-denominated, non-investment grade, fixed-rate, taxable corporate bond market.

An index is a portfolio of specific securities, the performance of which is often used as a benchmark in judging the relative performance to certain asset classes. Index performance used throughout is intended to illustrate historical market trends and performance. Indexes are managed and do not incur investment management fees. An investor is unable to invest in an index. Their performance does not reflect the expenses associated with the management of an actual portfolio. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. All investing involves risk including loss of principal. Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market. Past performance is no guarantee of future results.

Key Indicators

Key Indicators correspond to various macro-economic and rate-related data points that we consider impactful to equity markets.

- The US 10-Year Treasury Yield (%)/bps, is the return on investment for the U.S. government’s 10-year debt obligation and serves as a signal for investor confidence.

- SPDR Gold Trust Price ($), is an investment fund that reflects the performance on the price of a gold bullion, less the Trust’s expenses.

- West Texas Intermediate, which is an oil benchmark and the underlying asset in the New York Mercantile Exchange’s oil futures contract.

- CBOE Volatility Index (Level)/% Change, which uses price options on the S&P 500 to estimate the market's expectation of 30-day volatility.

General Disclosure

Wilbanks, Smith & Thomas Asset Management (WST) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. This material is not intended to replace the advice of a qualified tax advisor, attorney, or accountant. Consultation with the appropriate professional should be done before any financial commitments regarding the issues related to the situation are made.

This document is intended for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty and does not represent the performance of any specific investment strategy.

Some of the information enclosed may represent opinions of WST and are subject to change from time to time and do not constitute a recommendation to purchase and sale any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.