4Q 2020 Economic & Markets Overview

“How did I get into this and how do I get out of it again, how does it end?” - Soren Kierkegaard

“Sooner or later everyone sits down to a banquet of consequences.” - Robert Louis Stevenson

2020 is finally behind us, and the fourth quarter brought important transitions in the war against COVID and the global economy and investment markets. Most striking was the shift in sentiment as good news and optimism about vaccines and the promise of more government stimulus offset spiking COVID case counts and the bitter U.S. political picture. The improved mood led to solid returns for investment assets in all categories. While the pandemic still looms large, investors can finally see a light at the end of the tunnel, and the transition from a bunker mentality to the emerging focus on the "next normal" occurred so quickly that markets likely borrowed some of 2021's return during the fourth quarter.

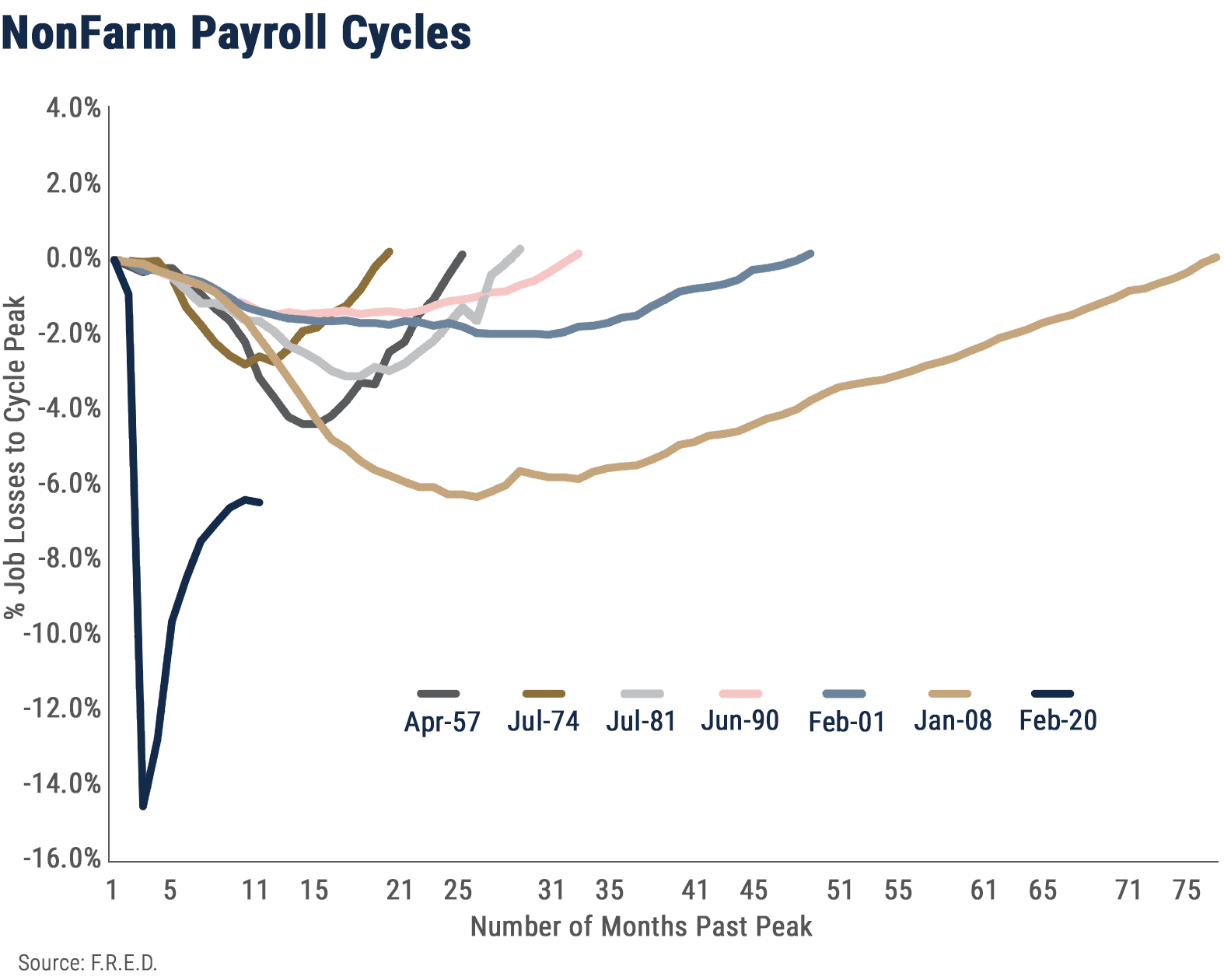

Of course, risks and uncertainty abound as the distribution and acceptance of vaccines gets under way, and the path of the economy remains tied to the course of the pandemic. As we write this letter the healthcare system is struggling to get vaccines into arms, and the seven-day rolling average of new cases in the United States continues to exceed 250,000. With large segments of the economy still operating below capacity the employment picture, while much improved from the March and April nadir, projects a long, slow path to full recovery. Payrolls remain 9.8 million or 6.5% below the February 2020 peak, and employment growth has slowed meaningfully in the past two months. At this pace it will take until November 2023 to reach the prior peak, making it the longest recovery in modern times other than the great financial crisis of ’08-’09.

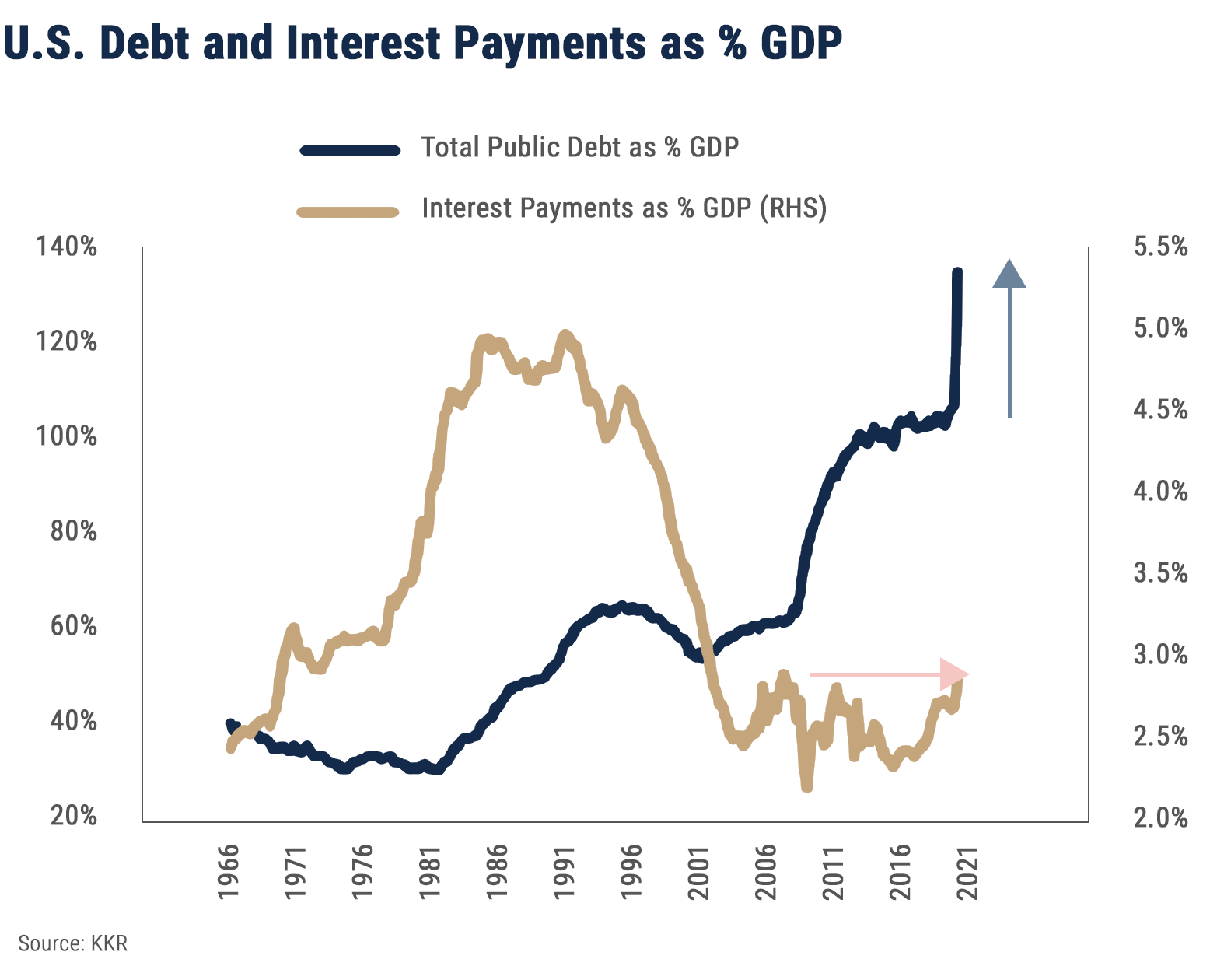

Looking back a year, economists were concerned the global expansion was aging, but while many expected a normal cyclical slowdown none foresaw the coming abyss. The speed and magnitude of both the collapse of the global economy and the response from policymakers were unprecedented. Governments around the world, and particularly the U.S. Federal Reserve and Congress, responded with a flood of stimulus roughly three times the size of the government response to the 2008-2009 financial crisis. As positive as the market response to that fiscal stimulus has been, the debt incurred to fund it will have consequences in coming years. Most estimates indicate that in the G-20 alone the COVID-related fiscal packages will exceed $10 trillion, and the U.S. relief effort puts us in uncharted fiscal territory with the national debt projected to surpass our annual economic output in 2021 for the first time since World War II. While the new debt is manageable over the short term as long as interest rates remain low, if rates rise as the economy improves the day of reckoning could be painful. The following chart from KKR reveals the extent to which low interest rates have mitigated the financial impact of our burgeoning debt, with interest expense as a percent of GDP basically flat while the total debt as a percent of GDP has exploded.

President-elect Biden's appointee for Treasury secretary, Janet Yellen, has supported the relief programs but has also bluntly voiced her concerns about the dangers of the ballooning federal deficit and debt. In February, even prior to the crisis, Yellen said "the U.S. debt path is completely unsustainable under current tax and spending plans." Since then, we’ve borrowed trillions of additional dollars to fund the relief effort, and with the new administration promising to ramp the spending up even more this year, the outlook for inflation and interest rates will remain in focus.

Equity Market Overview

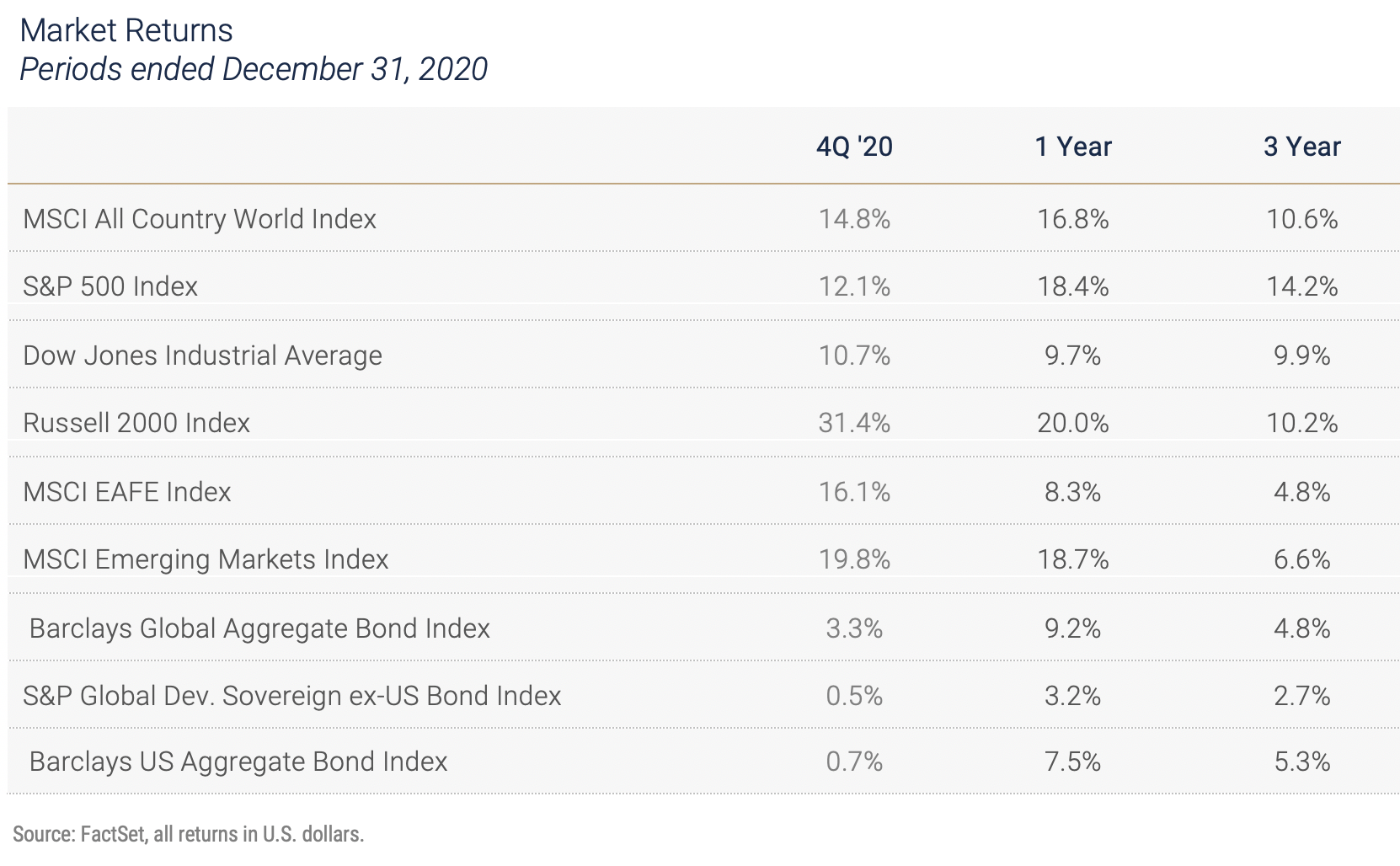

Given the backdrop of optimism about vaccines and stimulus, global equity markets ignored the debt explosion and ended the year on a very positive note. Sector performance within the U.S. reflected the improving economic outlook as beaten-down cyclical stocks rallied strongly. In the fourth quarter the S&P 500 Index returned 12.1% while the Russell 2000 Small Cap Index surged 31.4% and the Russell 1000 Value Index posted a 16.3% return, generously rewarding patient investors in those asset classes after the long stretch of dominance by large-cap growth stocks.

Factor investing is the process of diversifying equity portfolios using attributes that tend to perform consistently and which, over time, are expected to generate favorable risk and return patterns when combined in a portfolio. Our implementation of factor investing is accomplished through allocations to small-cap and value stocks in addition to our core holding of US large-cap stocks, which is generally invested in the S&P 500. We have written in the past about the patience required to stay invested in the more volatile segments of the market, including small cap and value stocks, where the long-term return premiums have historically been generated from short bursts of strong relative performance. The timing of those bursts of performance is inconsistent and difficult to predict, so long-term strategic allocations to these market segments are necessary to capture the returns when they occur.

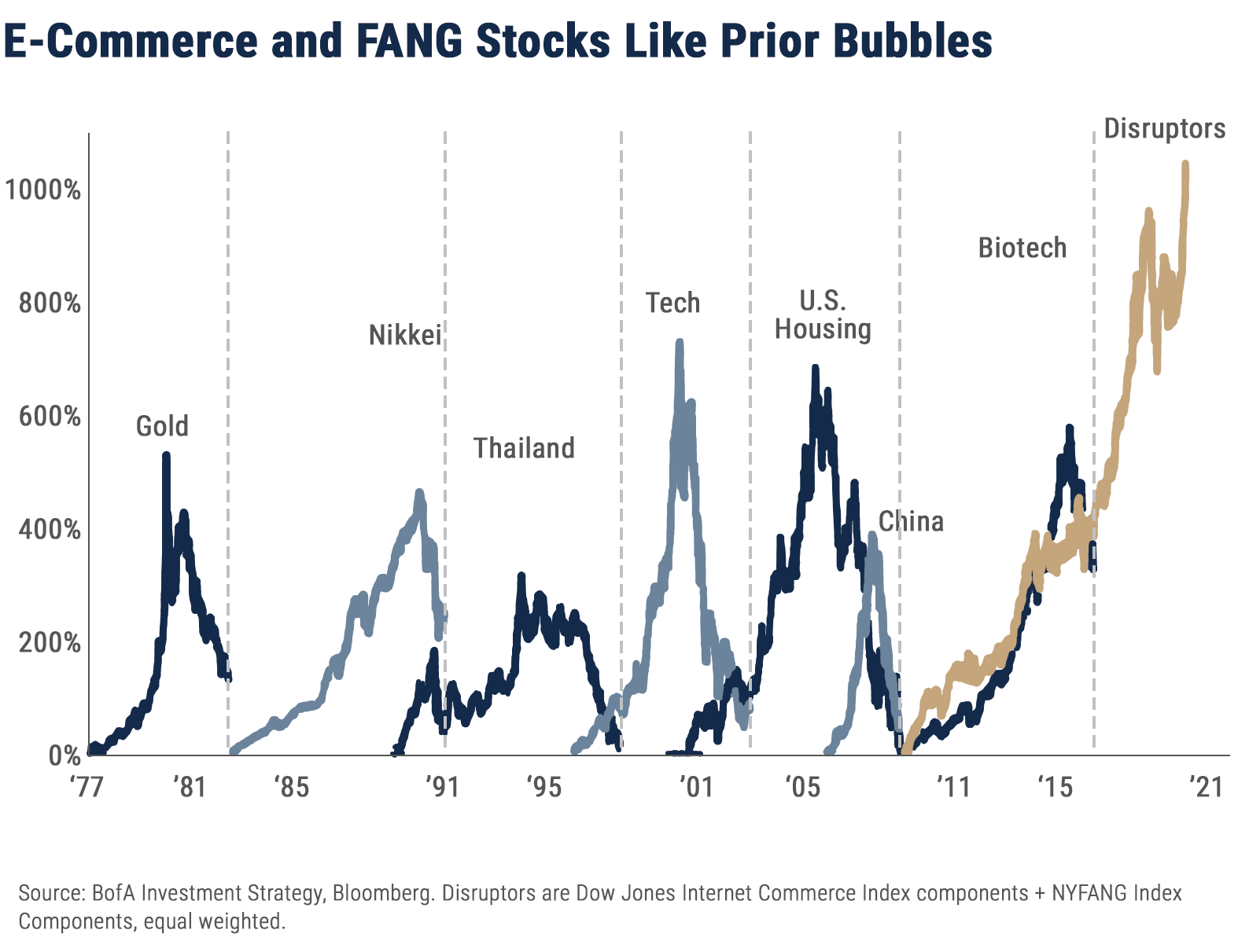

Investor patience with a well-diversified portfolio strategy is tested in a year like 2020 when one segment of the market captures headlines. Probably the most-watched story for equity investors last year was the convergence of factors that led to the hyperbolic price performance of e-commerce and FANG stocks. Those companies benefited from the accelerated transition to online work, education, shopping and entertainment, and their stocks took off as investors shifted from market segments with dimmer prospects. Now those stocks look vulnerable, especially as investors begin to anticipate a normalizing business climate, and the "Disruptors," as BofA Investment Strategy calls them, have, as a group, reached levels reminiscent of other asset class bubbles from the last 40 years.

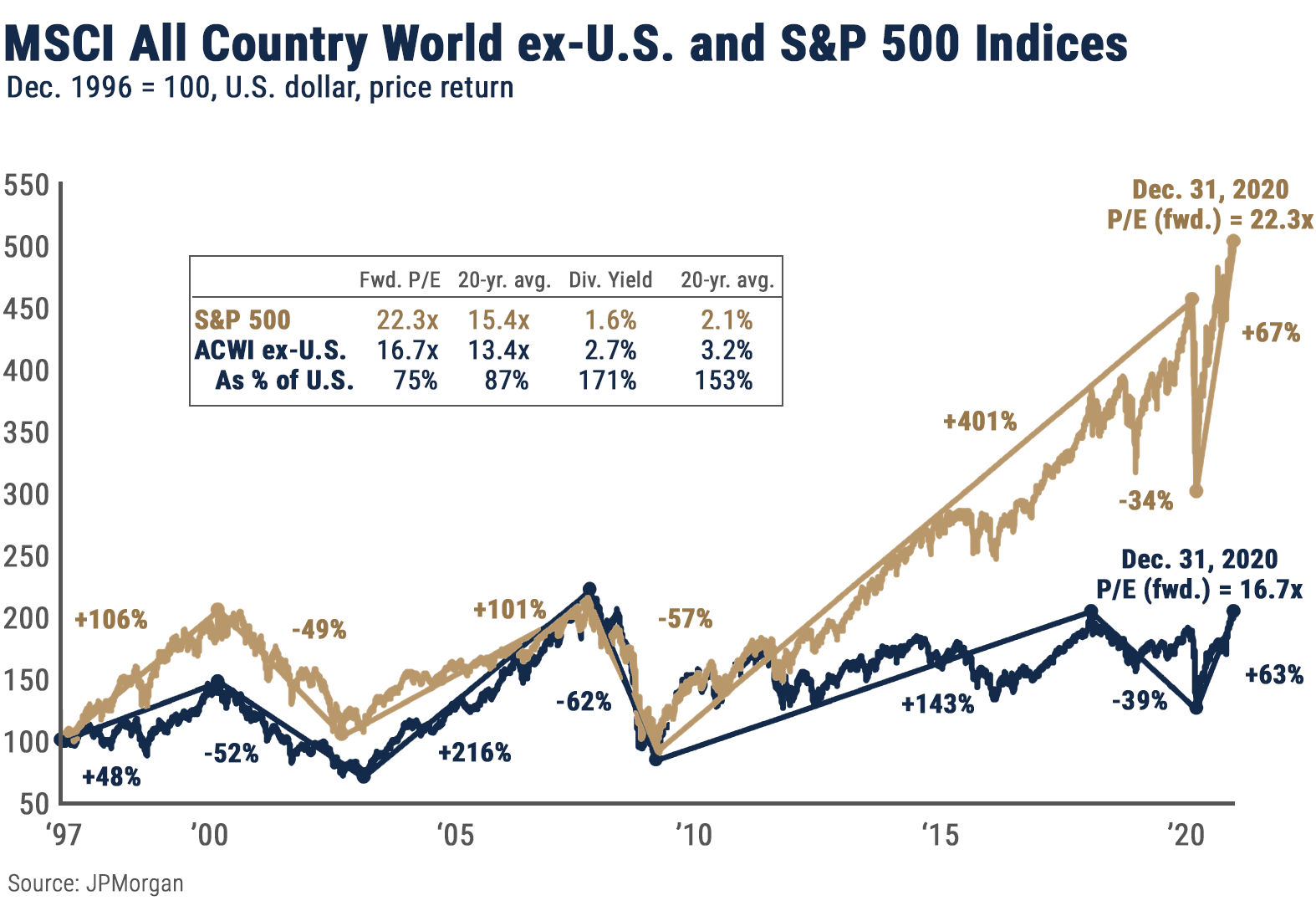

Maintaining an allocation to international stocks is another fundamental of our strategy, and Non-U.S. equity markets, both developed and emerging, outperformed the U.S. in December to finish off a strong quarter. Admittedly, there was a lot of catching up to do in that comparison, and the U.S. still finished the year ahead of most foreign equity markets. Looking ahead valuation metrics favor overseas equities which, despite the recent outperformance, remain at attractive discounts to domestic stocks. As the chart below, courtesy of JPMorgan, reveals, the forward P/E ratio for the S&P 500 is 30% higher than the ACWI index of non-U.S. stocks, and the dividend yield on the international index is over 1% higher.

Foreign equity returns were buoyed by the declining U.S. dollar in the fourth quarter. The dollar is generally considered a safe-haven asset in times of market and economic stress, and the value of the dollar peaked in mid-March amid the panic-driven flight from risk. More recently the economic recovery in the U.S. has slowed relative to other parts of the world, particularly the emerging markets, and the value of the dollar has now declined about 10% since the March peak. Dollar volatility is likely to continue this year. The varied timing and magnitude of stimulus packages around the world and the differing trajectories of local economies as they emerge from the pandemic suggest currency movements will be larger than normal, with a bias toward a weaker dollar.

Bond Market Overview

2020 was a rollercoaster ride for bond portfolios as the COVID-19 angst reverberated throughout the fixed income markets. Bonds were whipsawed during the market volatility earlier in the year, but the major fixed income sectors finished with positive returns.

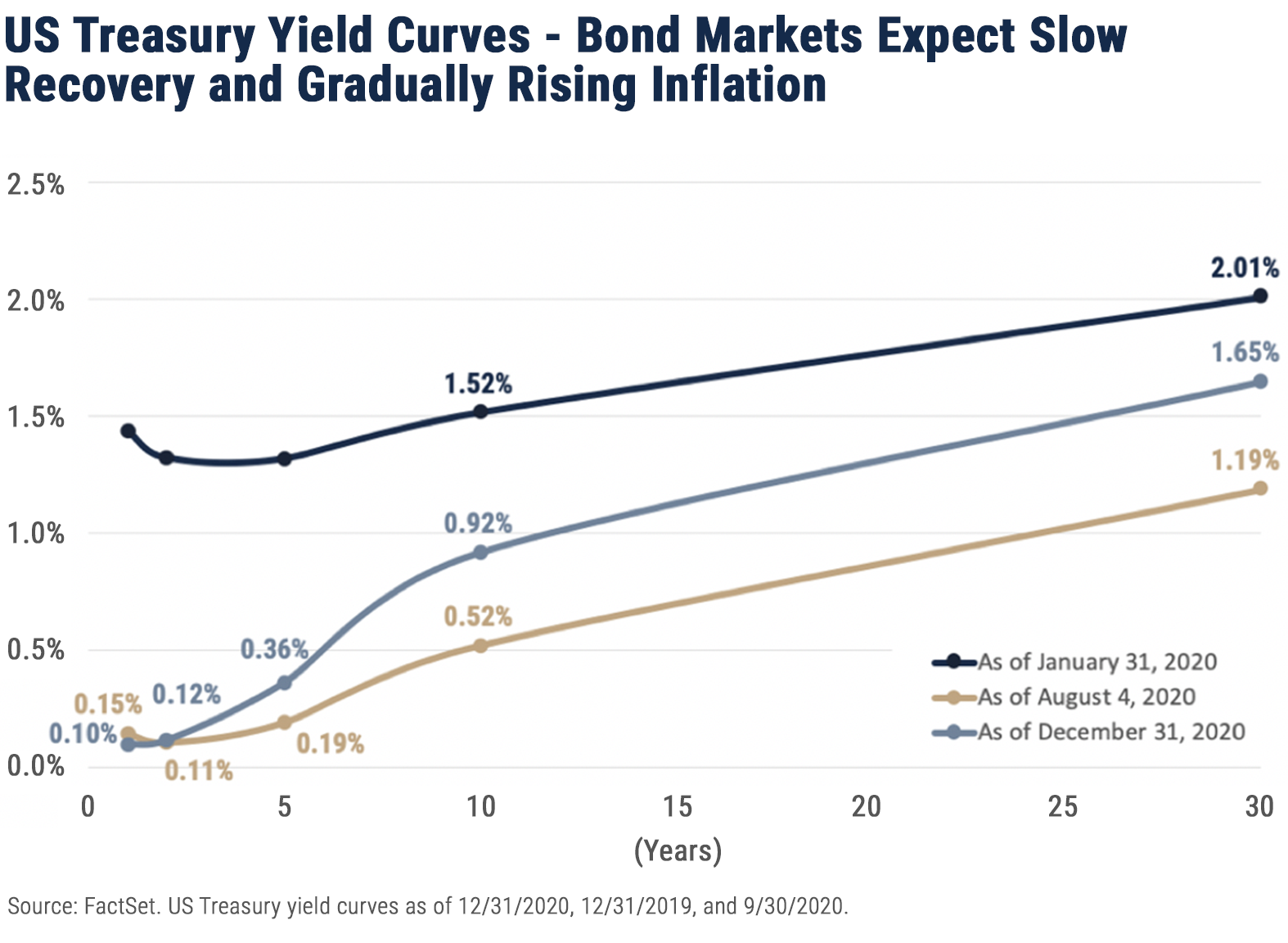

Looking ahead the challenges facing fixed income investors are daunting. The COVID crisis and the government’s response drove Treasury bond yields to new lows even as spreads on credit-sensitive bonds blew out in March, and once the Fed aimed its massive spending power at the markets for municipal bonds, corporate debt and mortgages, those sectors rallied back to pre-crisis levels. Bonds in general ended the year at yields that reflect market expectations for a gradual recovery and moderate inflation, leaving little margin for error, especially in light of the bullish consensus expectations for the paths of the pandemic and the global economy.

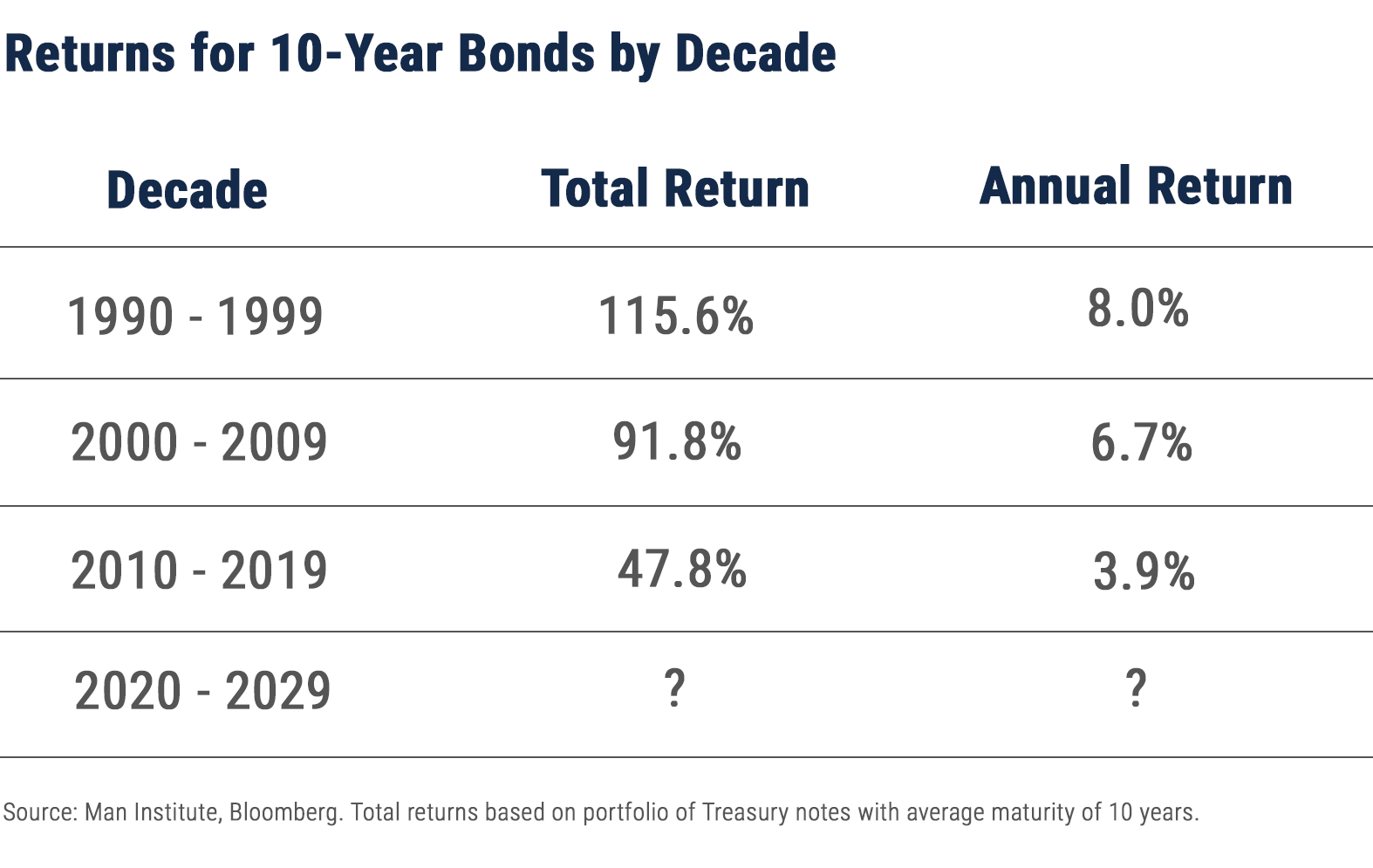

Bonds play a dual role by providing reliable income on a regular basis and stabilizing portfolios during market crises. Now, given the low yields on bonds and the high valuations for stocks, investors are questioning the logic of hedging expensive equities with expensive bonds. Because the return on a bond is determined by the yield at which the bond is purchased, returns earned by investors have declined as interest rates have fallen since their peaks in the 1980s. During the 1990s 10-year Treasury bonds provided an annual return of 8% for the decade; that figure dropped to 6.7% for the 2000-2009 period, then fell to under 4% for the decade beginning in 2010. With the 10-year Treasury note languishing under 1% at the beginning of this year, that figure is the best estimate of the prospective return on that security.

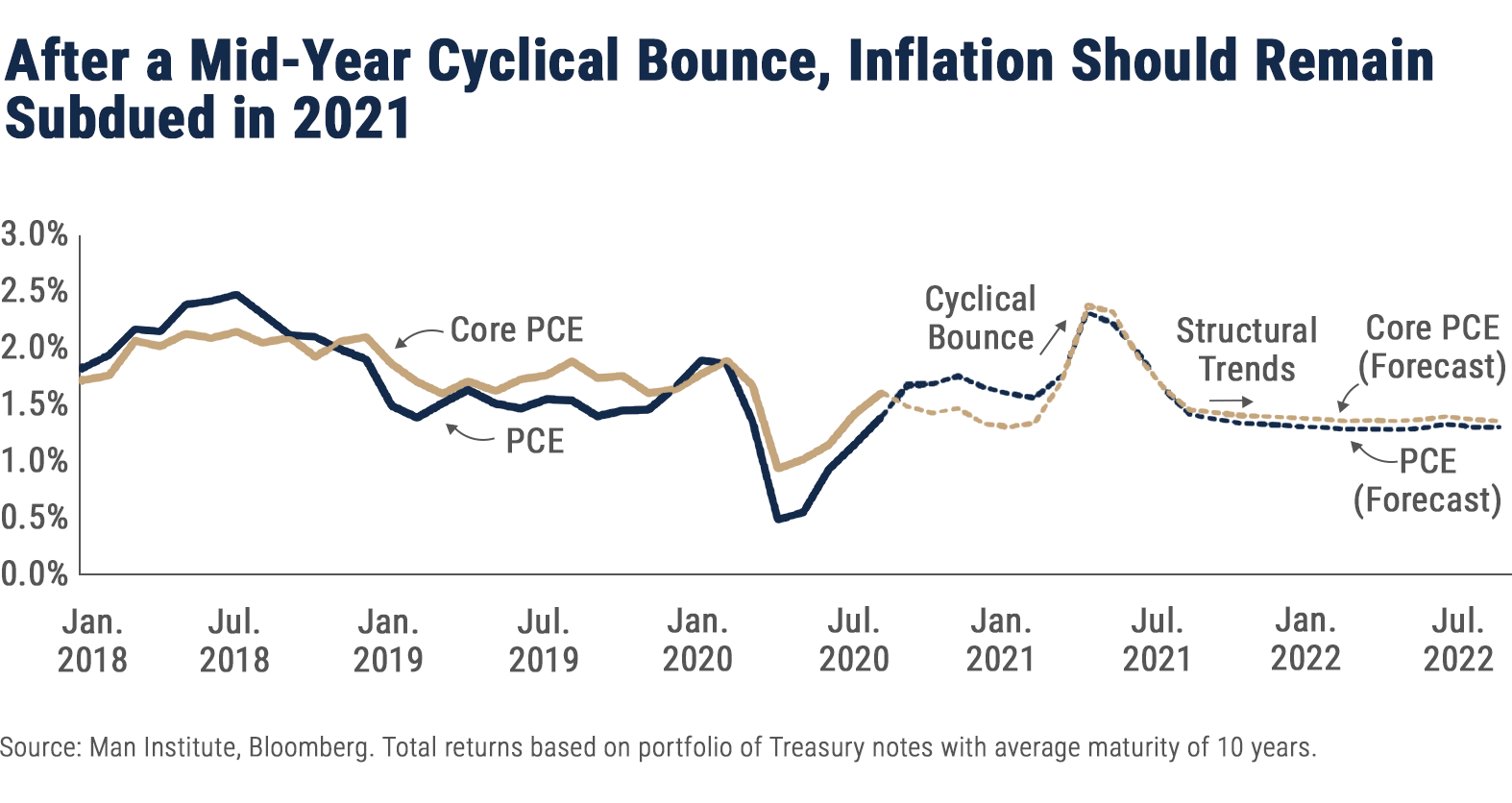

By avoiding long maturity, high duration holdings we can mitigate the risk of rising rates and maintain the flexibility to respond to opportunities. For the moment at least, the bond market remains relatively sanguine about the outlook for inflation and therefore interest rates. The chart above depicts the recent benign inflation environment and reveals the likelihood of a cyclical bounce in inflation this summer as the world reopens and unleashes the glut of savings now held on household and corporate balance sheets.

As we discussed last quarter the Fed gave itself new leeway in August when it changed its framework for addressing inflation. By softening its hard 2.0% inflation target into a comfort range of 2.0-2.5% average inflation, the Fed revealed that job creation remains its central focus. Most agree that the emphasis on employment is appropriate as we emerge from the pandemic, especially given that we remain far below full employment in the U.S. Even so, as the global economy shifts into a higher gear and the “flight to safety” trade is unwound, the risk of an upside surprise in inflation is worth watching.

Outlook

As 2021 unfolds the financial markets remain optimistic, but as we’ve outlined, we see lots of uncertainty around the key drivers of the global economy and markets. With the presidential election behind us, the political picture is clearer, and the likelihood of another round of stimulus is a positive, at least in the short run. Longer term the impact of our existing debt plus the new administration's fiscal policies is a concern. The progress of the COVID vaccine is on track, but distribution remains a challenge, and any setback on that front will disappoint the market.

Important Disclosures

Unless otherwise indicated, performance information for indices, funds and securities as well as various economic data points are sourced from FactSet as of December 31, 2020.

Wilbanks, Smith & Thomas Asset Management (WST) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. This material is not intended to replace the advice of a qualified tax advisor, attorney, or accountant. Consultation with the appropriate professional should be done before any financial commitments regarding the issues related to the situation are made.

This document is intended for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty and does not represent the performance of any specific investment strategy.

Some of the information enclosed may represent opinions of WST and are subject to change from time to time and do not constitute a recommendation to purchase and sale any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.