3Q 2023 | Economic & Markets Review

"Everything is unprecedented until it happens for the first time." — Sully Sullenberger

“If you have to forecast, forecast often.” — Edgar Fieldler

The narrative driving the strong recovery in the investment markets in the first half of 2023 flipped in the third quarter, sending bond yields higher and stock prices lower. During the first half of the year bad news for the economy was good news for stocks as slower economic growth and a cooler U.S. job market fueled optimism that inflation was moderating and would allow the Fed to nail the elusive soft landing without triggering a recession. That optimism faded over the course of the summer and better-than-expected economic news was bad news for the markets, pushing interest rates higher and resetting expectations about the magnitude, direction, and timing of future Fed action. The mantra became "higher for longer," and stocks responded by declining across all sectors and geographies, with selling pressure intensifying in September as interest rates jumped.

The U.S. economy is estimated to have grown at a healthy 3.5% annual rate in the third quarter, driven primarily by resilient consumer spending, but in coming months consumers and businesses will begin to feel the impact of higher interest rates as loans reset and new debt becomes more expensive. Borrowing costs have continued to rise in early October with the yield on the all-important benchmark 10-year Treasury bond touching a 16-year high of 4.9%, up from 3.3% in April, and the average 30-year fixed-rate mortgage rate rising to 7.3%, the highest in 25 years. Given this backdrop, economic growth is expected to slow to under a 1.0% annual rate in the fourth quarter.

The key questions facing investors now are how much growth will slow (and whether growth will actually turn negative, i.e., will we have a recession?) and whether the markets will interpret slower growth as good news or bad. If inflation continues to moderate, giving the Fed some breathing room and relieving the pressure on longer term yields, equity investors will cheer. On the other hand, if the economic slowdown persists or deepens into a recession consumer spending and corporate earnings will be impacted, especially if the slowdown is coupled with stubborn inflation. With valuations still relatively high equities will likely respond poorly to lower earnings. But, for now at least, good news is good news, and the markets are betting on a soft landing for the economy. A reasonable gauge of the outlook for the economy and its effect on businesses is the trend in corporate earnings estimates, and the consensus estimate for the S&P 500 calls for 10% growth in 2024 despite the headwind of higher interest rates.

Rising interest rates and changes in the dynamics of the bond market grabbed the headlines in the third quarter, and rightly so. Bonds are generally considered the safe, boring part of a portfolio, but as many investors learned in 2022, bonds are anything but safe in rising rate environments. And as we’ve been reminded this year, the fixed income markets are definitely not boring! We'll focus on the opportunities presented by today’s bond market in the section below, but first we turn to the economic implications of the Fed's efforts to dampen inflation. As we have discussed in prior letters, it is easy to see in hindsight the Fed stayed too accommodative for too long with the massive infusion of liquidity during and after the COVID crisis. The Fed’s short-term interest rate policy and its purchases of Treasury and mortgage bonds under its quantitative easing program led to the stubborn inflation it’s fighting now. Chairman Powell’s characterization of inflation as “transitory” in 2021 will be remembered as one of the worst misjudgments in Fed history.

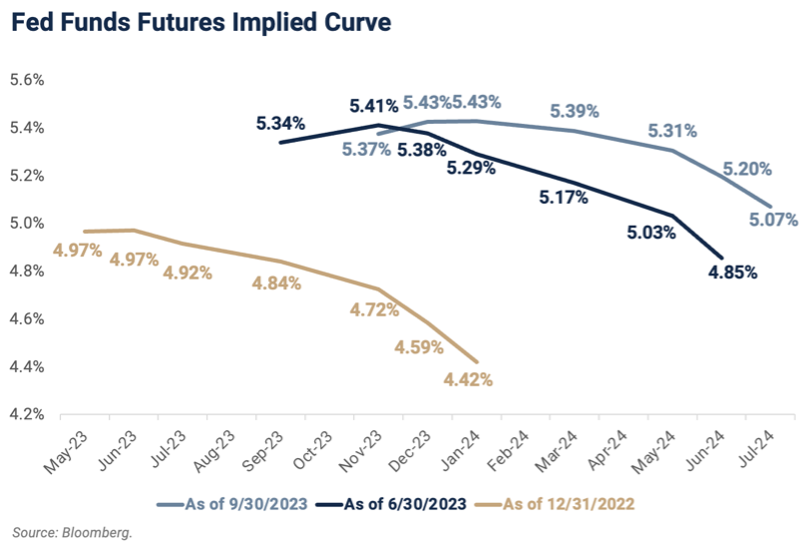

Now, after 525 basis points of rate hikes in 18 months, the fastest rate hike cycle in history, the Fed runs the risk of raising rates too much just as the impact of quantitative tightening begins to filter through. The graph above reveals the evolution in the expectations for Fed policy over the course of the year. At the end of 2022 the market thought the Fed would be cutting rates by now and was projecting a Fed funds rate of 4.42% in January 2024. Today the market expects another rate hike before year-end and forecasts a Fed funds rate above 5% through at least mid-2024.

As we consider the resilience shown by the U.S. economy this year despite the Fed’s hawkish policy, it's important to realize that large segments of the economy have been insulated from the Fed’s efforts to dampen growth. For example, as former Federal Reserve Board member Kevin Warsh points out in a Wall Street Journal editorial, 90% of single-family residences in the U.S. are financed by existing fixed-rate mortgages with low rates, and two-thirds of automobile loans are similarly situated with loans originated before 2022. Warsh also reminds us the majority of investment grade corporate borrowing is structured as fixed rate debt. So while today’s higher borrowing costs have definitely impacted the housing market by freezing in place homeowners reluctant to sell and lose the benefit of their existing low-rate mortgages, the bulk of interest payments made by individuals and companies have not changed materially as the Fed has pushed rates higher. However, when those loans mature or need to be refinanced, and as new loans are made for ongoing consumption and investment, borrowers will be facing much more onerous terms.[1

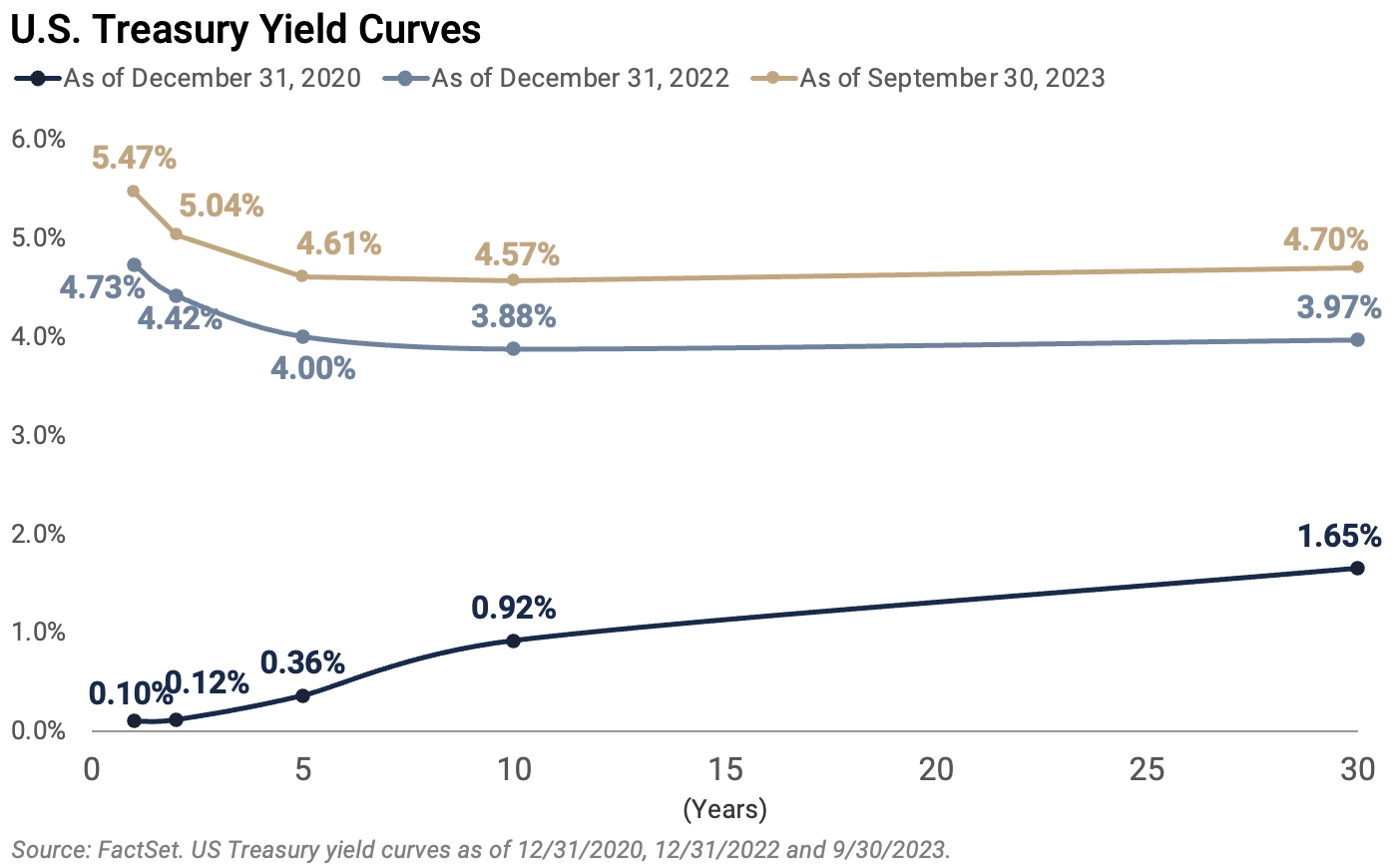

Investors and the media tend to focus on the Fed’s short-term interest rate policy, but the term structure of interest rates as reflected in the Treasury yield curve is an important part of the economic story from the third quarter. As the Fed pushed short rates higher in 2022 the yield curve inverted, and since July of last year short-term yields have exceeded those on longer maturity bonds. An inverted yield curve is generally acknowledged to be a reliable predictor of a coming recession. With the exception of very short-term yields the inversion largely corrected in the third quarter, and a week into October yields are essentially flat in the two-year to 10-year range with 30-year yields roughly 20 basis points higher. At first glance the normalizing yield curve could be interpreted as good news, and that would be the case if the curve steepened because short-term rates retreated. In industry jargon a yield curve inversion that resolves because short-term rates decline is known as a "bull steepener" because the circumstances in which that occurs, slowing inflation with expectations of Fed rate cuts, are bullish for equities. This time, however, the resolution came because longer-term yields rose so quickly, a scenario known as a "bear steepener" because it anticipates continued inflation and higher-for-longer interest rates. Those factors create more restrictive financial conditions and are generally negative for the equity markets.

EQUITY MARKET OVERVIEW

A glance back at our second-quarter commentary reminds us how quickly things can change! Going into the summer the tailwinds of lower inflation, stable interest rates, healthy but unspectacular economic growth, and the promise that AI would transform the technology sector had pushed the global equity markets strongly into positive territory and left the carnage of 2022 a distant memory. The storms in the bond market changed everything in the third quarter. The surge in Treasury yields, particularly in the long end of the curve, sapped the energy from the equity markets as investors came to terms with the new “higher-for-longer” reality.

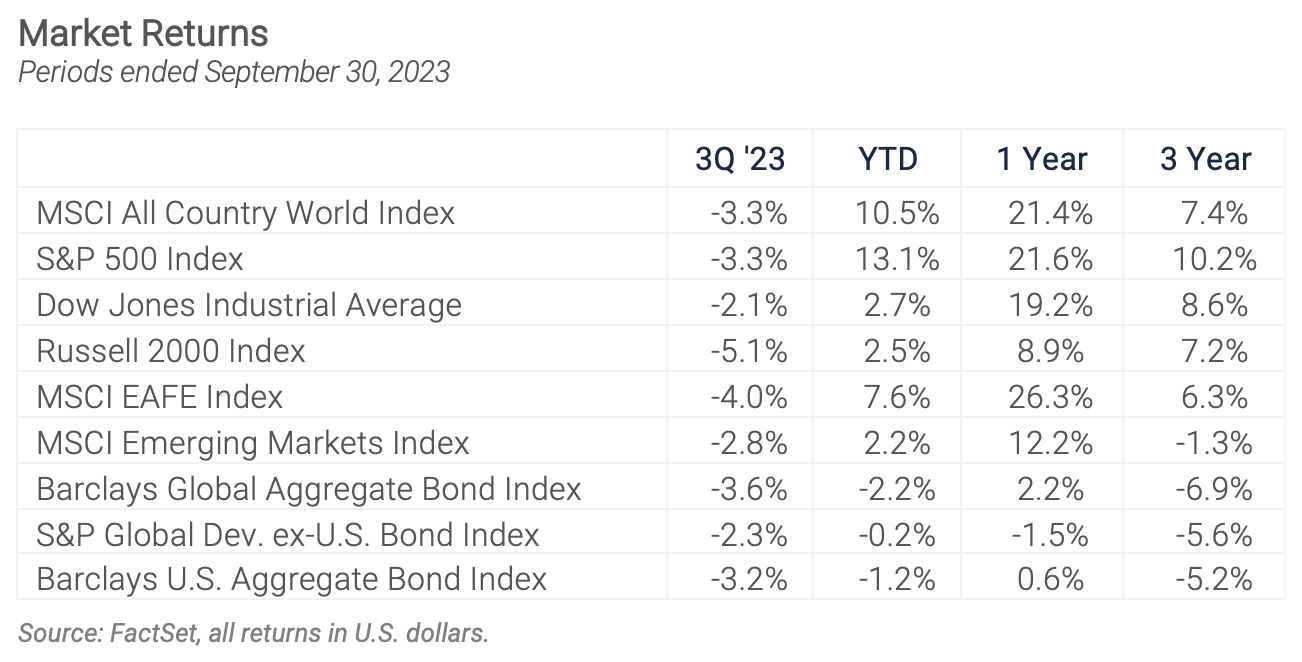

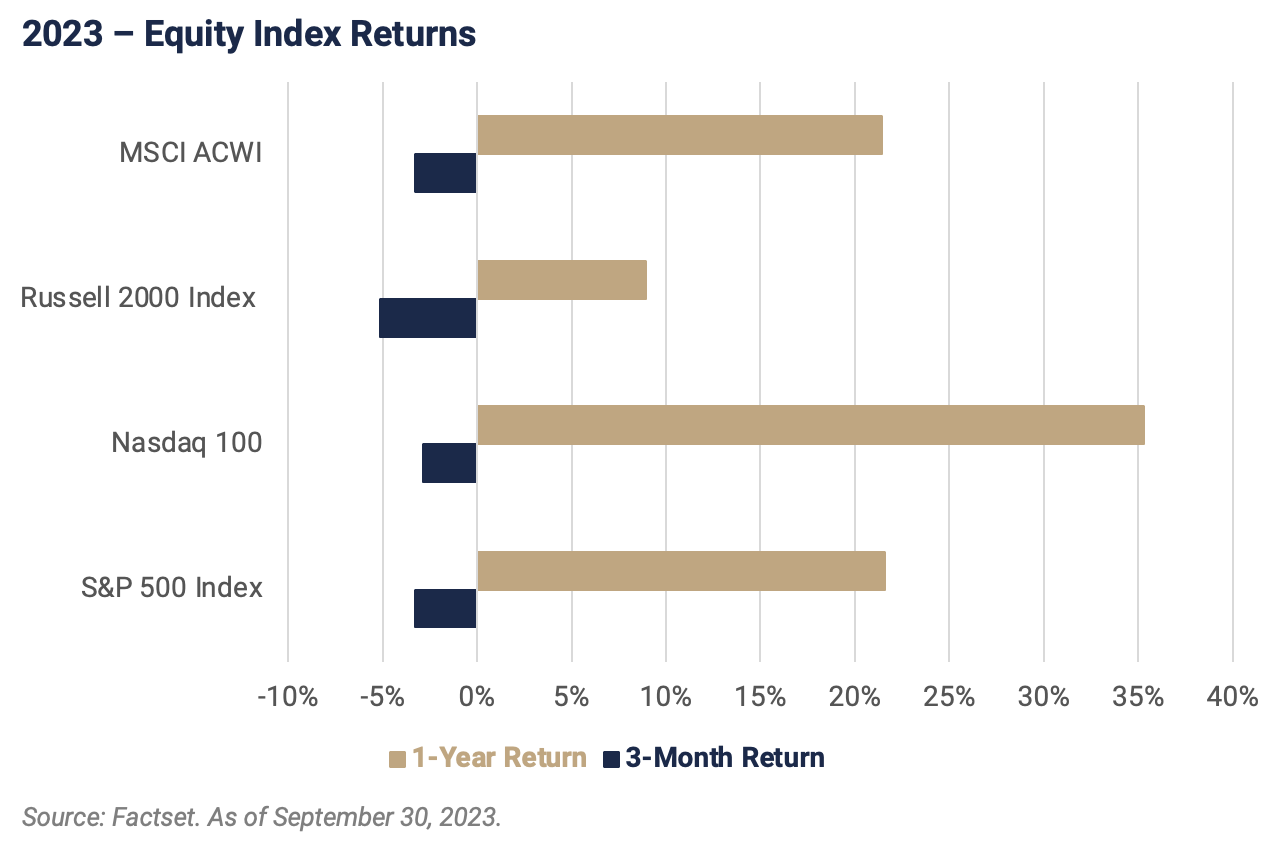

Still, as the preceding chart reveals, the time frame of reference makes all the difference in a review of equity market performance at the end of September. Despite September’s weakness the 12-month returns for stocks remain strongly positive. The broadest gauge of the global market, the MSCI All Country World Index (ACWI), was up over 20% for the 12 months ending September 30, as was the S&P 500. Small cap stocks as represented by the Russell 2000 index continue to lag large companies but still ended the quarter with a respectable 12-month return of almost 10%. The year-to-date numbers covering the first nine months of 2023 also remain palatable, with the S&P 500 up 13.1% and the MSCI ACWI up 10.5%. Zeroing in on the more recent data, the numbers turn negative for the third quarter, when both the S&P 500 and the ACWI were down 3.3% and the change in sentiment really comes into view when we zoom in to the month of September, when concerns about "higher for longer" interest rates kicked in and the S&P 500 fell 4.8% while the global benchmark ACWI fell 4.1%. With rising interest rates emerging as the key concern, interest rate sensitive segments of the market declined most in September, with large cap growth stocks falling 5.4% and small-cap stocks falling 5.9%.

The potential impact of higher interest rates on the equity markets is heightened by the extreme concentration of the composition and performance of the capitalization-weighted index in a small number of growth stocks. When interest rates are low, investors are willing to pay up for long duration assets, including those stocks expected to generate high earnings growth, because future earnings are worth more on a present value basis. As of the end of September, seven mega-cap U.S.-based growth companies dubbed the Magnificent Seven: Apple, Microsoft, Amazon, Google, Nvidia, Tesla, and Meta (Facebook), made up just under a third of the S&P 500 by size and accounted for almost all of its gain in 2023. Those results came despite the retreat in tech stocks in the third quarter, which saw the biggest companies in the index, Apple and Microsoft, decline 12% and 7.3%, respectively.

The chart above depicts the difference between the cap weighted S&P 500’s 13.1% gain so far this year and the return on the equal weighted index, which is roughly flat for the year.

The catalysts driving equity returns this year will remain in play in the fourth quarter: inflation, interest rates, and economic/earnings growth. The next several months will reveal whether the Fed can navigate a soft landing, and while there is no precedent for 525 basis points of Fed tightening without a recession, “everything is unprecedented until it happens for the first time.” The most hopeful sign of a soft landing is the health of the U.S. labor market, which added 336,000 jobs in September while the unemployment rate remained unchanged at 3.8%. That is as close to a “Goldilocks” report as we could’ve hoped for, and Bankrate’s October survey of U.S. economists indicates the likelihood the U.S. economy can avoid a recession is improving. According to the survey the odds of a recession between now and September 2024 have dropped to 46%, significant but well below the forecast probability of 59% last quarter and the 65% probability estimated by the same survey coming into the year.

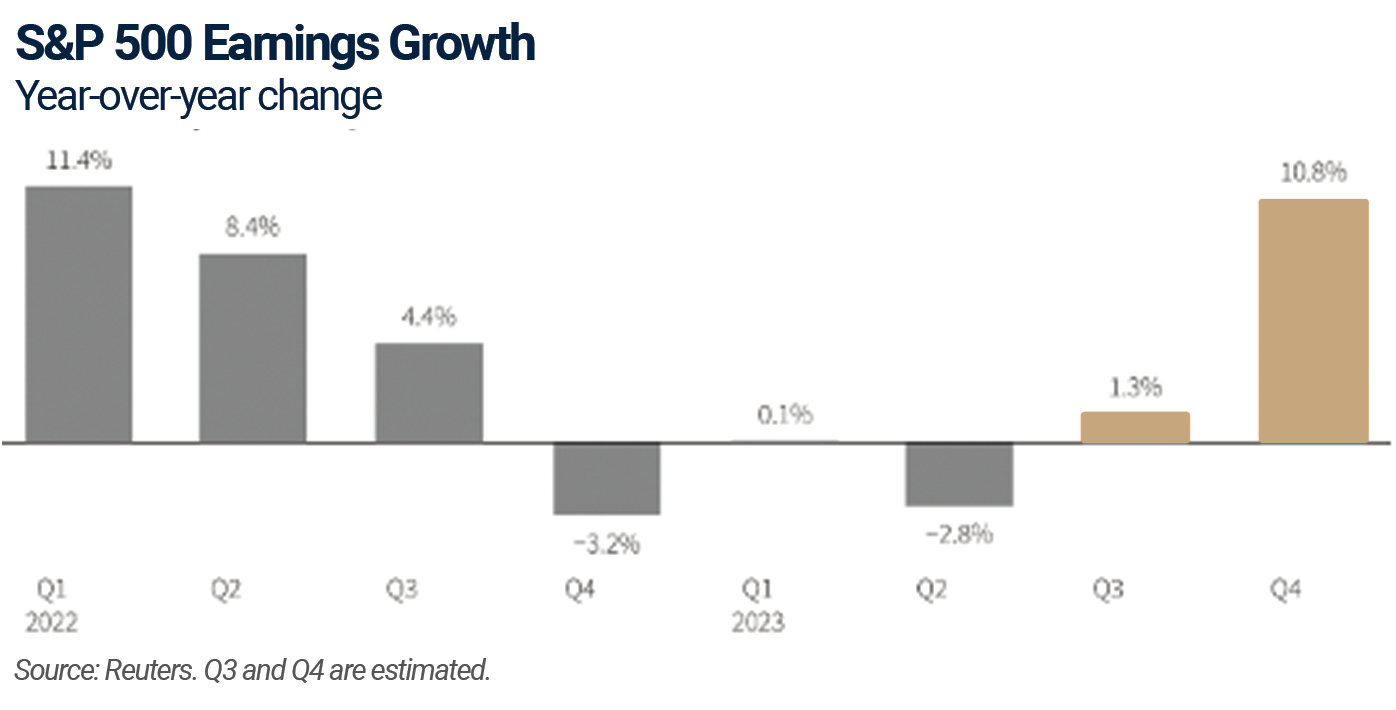

Optimism about the economic outlook has also fueled hopes for improved corporate earnings, which are now expected to have risen slightly in the third quarter, and which could breathe life into the equity markets. After three quarters of flat or declining profits even a small increase would be encouraging.

As companies report their third quarter profits in late October and early November investors will be listening closely to the commentary on the outlook for the fourth quarter. As it stands today, fourth-quarter profits for S&P 500 companies are expected to grow at a robust 10.8%, and changes in those estimates will determine the direction of sentiment as the end of the year approaches. Even after its third quarter price declines the S&P 500 is trading at 17.8 times expected earnings, well above the 25-year average of 16.7 times, so there is not much margin for error in today’s valuations. If there is any bad news about the improved outlook it’s simply the heightened risk of disappointment, but for now we will take the good news as good news.

BOND MARKET OVERVIEW

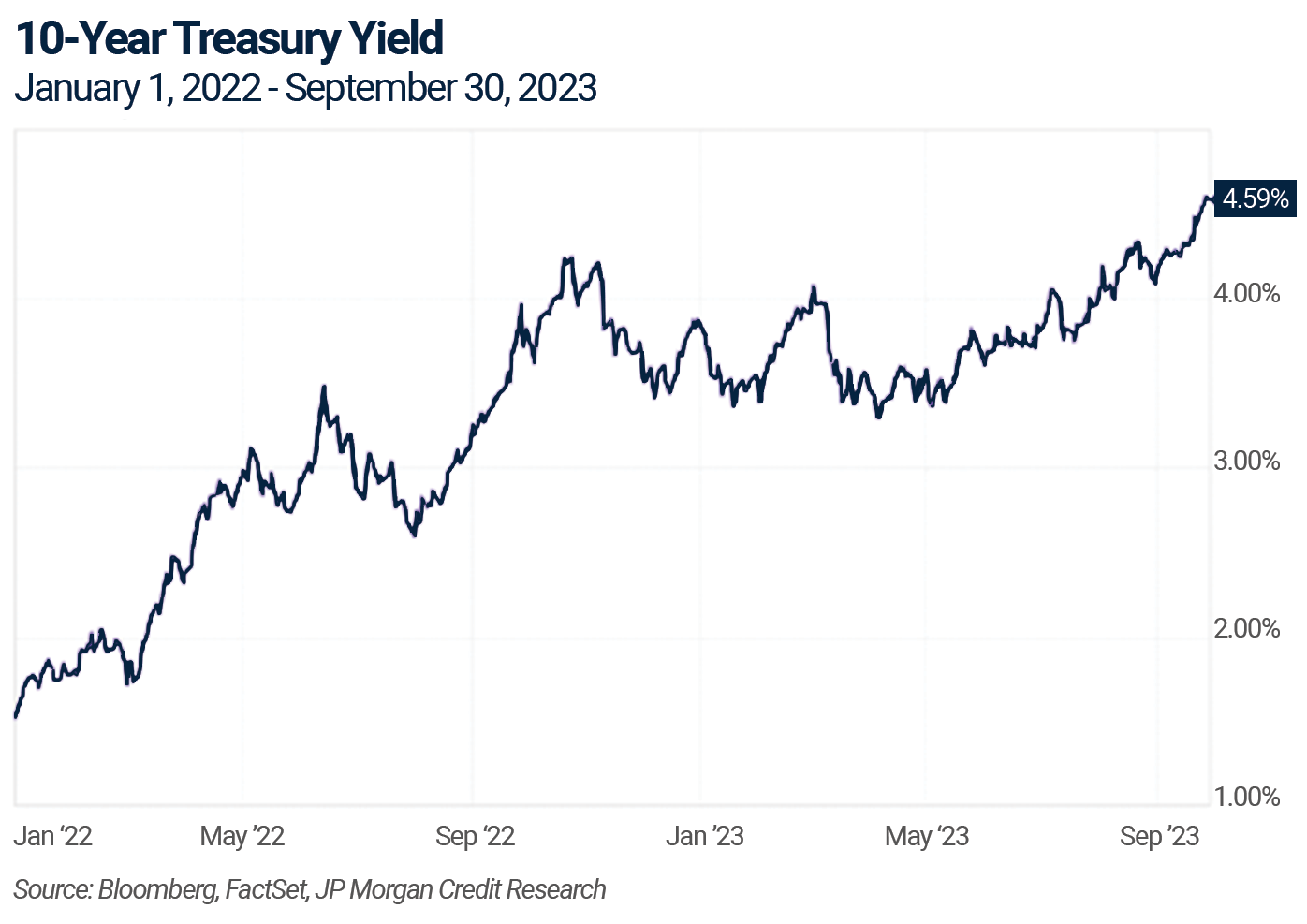

The message from the bond market at the end of the third quarter is clear: the era of disinflation and low interest rates has ended. That era began with the Fed’s efforts to save the economy after the 2008 Great Financial Crisis and continued through the zero interest rate policy during the pandemic. The 75 basis point (three quarters of a percent) run up in the yield on the benchmark 10-year Treasury in the third quarter reveals the market’s newfound conviction that, despite the Fed’s determination, inflation will not fall to its 2% target anytime soon. At its current level of 4.8%, the 10-year Treasury yield rests at its highest point since just before the GFC, and because so many financial instruments price off the 10-year the implications for investors are huge.

Unlike the first half of the year when yield increases were most pronounced in the short end of the curve where security prices are least affected by higher rates, intermediate and long-term Treasury yields rose the most in the third quarter, resulting in losses for institutions and investors holding longer-term securities. As we predicted in the previous commentary cash and short-term Treasuries turned out to be a remarkably good hiding place in the third quarter because of their higher yields and limited duration risk. The iShares 1-3 Year Treasury Bond ETF enjoyed a positive return of 0.6% in the quarter, earning it the dubious distinction of representing the only segment of the bond market to generate positive returns. The iShares 3-7 Year Treasury Bond ETF was down 1.2% for the quarter and the iShares 20+ Year Treasury Bond ETF fell 13.1% bringing its year-to-date return to -9.0%. Since December 31, 2021 that fund has lost over 40% of its value; so much for the safety of fixed income! More broadly the Barclays U.S. Aggregate Bond Index was down 3.2% for the quarter, erasing its first half gain and leaving it down 1.2% YTD.

As we approach the end of the Fed rate hike cycle we've reached an inflection point in the bond market that some are calling a historic, once in a generation opportunity for fixed income investors. We won't overstate things, but with both the futures market and Fed projecting the peak in policy rates by the end of next year, and because longer-term yields have risen so quickly, we see an opportunity to extend modestly the duration of bond portfolios to lock in today's attractive yields without excessive volatility risk. Cash was an excellent holding as interest rates were rising, but history shows cash yields decline rapidly following the final rate hike in a Fed tightening cycle. As the following chart demonstrates after years of paltry returns virtually all segments of the fixed income market offer their best yields in a decade. In some cases today’s yields are double or triple the returns earned on those asset classes over the past ten years.

Importantly these yields are available with an attractive risk profile. For example, the yield to maturity of the Aggregate Bond Index is 5.5% and the duration of the index is 5.9 years, so if interest rates rise 100 basis points an investor holding that index will almost break even in a year, realizing 5.5% in income and absorbing a 5.9% price decline. Putting that scenario in context the 10-year Treasury yield would have to approach 6% for bonds to fall that much, not impossible but not likely given the picture today. For now we are comfortable accepting the yields available on short and intermediate duration bonds, which offer strong income and protection of capital.

SUMMARY

Heading into the last quarter of the year investors are navigating a murky macro-economic and geopolitical environment. Inflation is slowing but economic growth is also slowing, and the indicators are inconsistent. The U.S. job market remains healthy and consumption remains strong, but the impact of the Fed's aggressive tightening is yet to be felt in most of the economy because so much outstanding debt remains locked in at attractive rates. Overall sentiment remains optimistic about the prospect of a soft landing for the economy, but there is no precedent for rate hikes in the range the Fed has implemented without a subsequent recession.

We recognize the possibility that despite the seemingly favorable trajectory of the economy and earnings over the past year investors may be too sanguine about how the cycle ultimately ends. The lagged impact of monetary policy may be felt just as other challenges come into play. Possible economic headwinds include higher energy prices, the resumption of student loan payments and the depletion of household savings after the post-COVID surge in "revenge consumption." The geopolitical picture seems more precarious by the day with Hamas’ terror attack on Israel adding complexity as the U.S. tries to evolve its policy for involvement in the Russia/Ukraine war and contend with China’s chest-thumping over Taiwan. All the while our dysfunctional Congress ignores big challenges including our burgeoning Federal deficit and the impending escalation in the cost of servicing our massive Federal debt after the recent interest rate increases.

The Fed remains in a difficult position. The FOMC will be reluctant to give any ground until they are certain inflation is under control, but the factors needed to quell inflation, most importantly weaker economic growth, could disappoint investors expecting a soft landing and healthy corporate profits. After the steepest rate hike cycle on record it’s unlikely the Fed has done just the right amount of tightening to stem inflation without triggering a recession, but we have no way of estimating the margin for error the Fed was working with. As we mentioned earlier, we do believe it likely that the Fed will err on the side of caution and hike too much rather than too little to be sure we’re not left with residual or resurgent inflation after this cycle of rate hikes ends.

Notes & Disclosures

Wilbanks, Smith & Thomas Asset Management (WST) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation, or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. This material is not intended to replace the advice of a qualified tax advisor, attorney, or accountant. Consultation with the appropriate professional should be done before any financial commitments regarding the issues related to the situation are made.

This document is intended for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred, or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty and does not represent the performance of any specific investment strategy.

Some of the information enclosed may represent opinions of WST and are subject to change from time to time and do not constitute a recommendation to purchase and sale any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy.

[1] Warsh,K. (2023, October 5). The Bond Market’s Message. WSJ pA17

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.