2Q 2020 Economic & Market Overview

As we pass the halfway point in the year, New Year's Day seems a distant memory. 2020 began with optimism and high expectations for the economy and markets, but that optimism has given way to a general sense of unease and anxiety about the future. That melancholy is reflected in the line above from a song by music legend John Prine, who died of complications of COVID-19 in April.

That's the way that the world goes 'round,

You're up one day, the next you're down,

It's half an inch of water and you think you're gonna drown,

That's the way that the world goes 'round…

- John Prine

Over just a few months the coronavirus redefined all areas of life including work, school, social and family interactions. From an economic standpoint it cost 30 million people their jobs, shuttered thousands of businesses and triggered the worst recession since 2008.

As if that weren't enough, we are also facing the most tumultuous strain on the social fabric of the US since the 1960s in the wake of the killing of George Floyd, and possibly the most divisive Presidential election in modern history. From a global perspective the pandemic has intensified our rivalry with China - a dynamic that becomes more important as Asia's share of global GDP approaches that of the West. Nationalist and protectionist sentiments have intensified, affecting supply chains at the expense of efficiency.

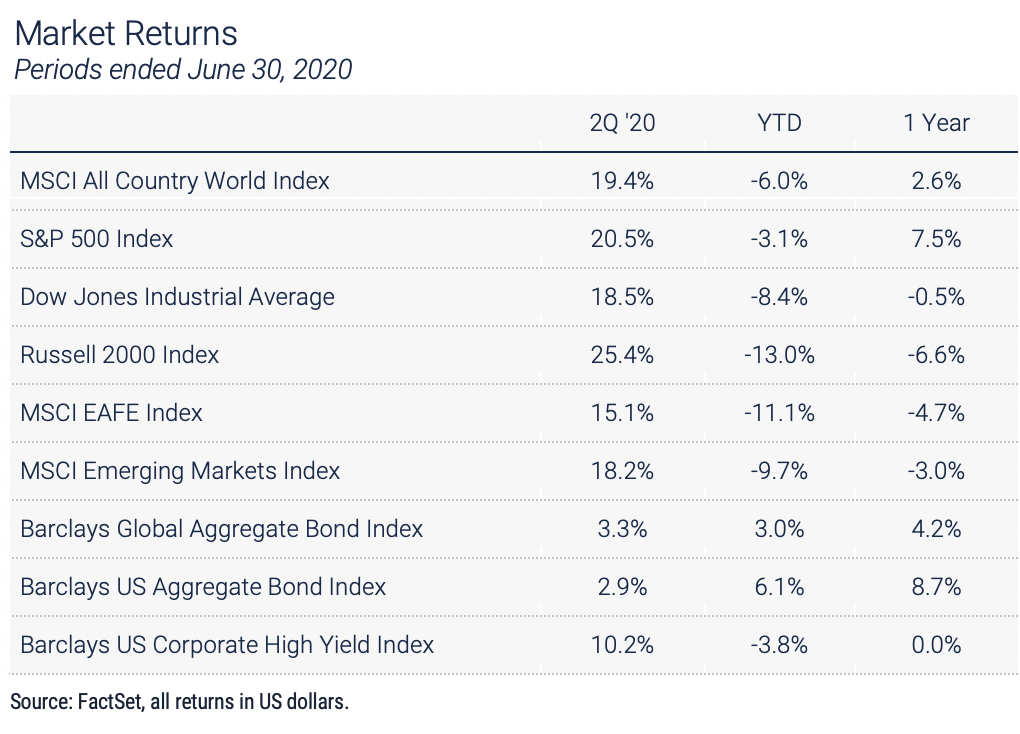

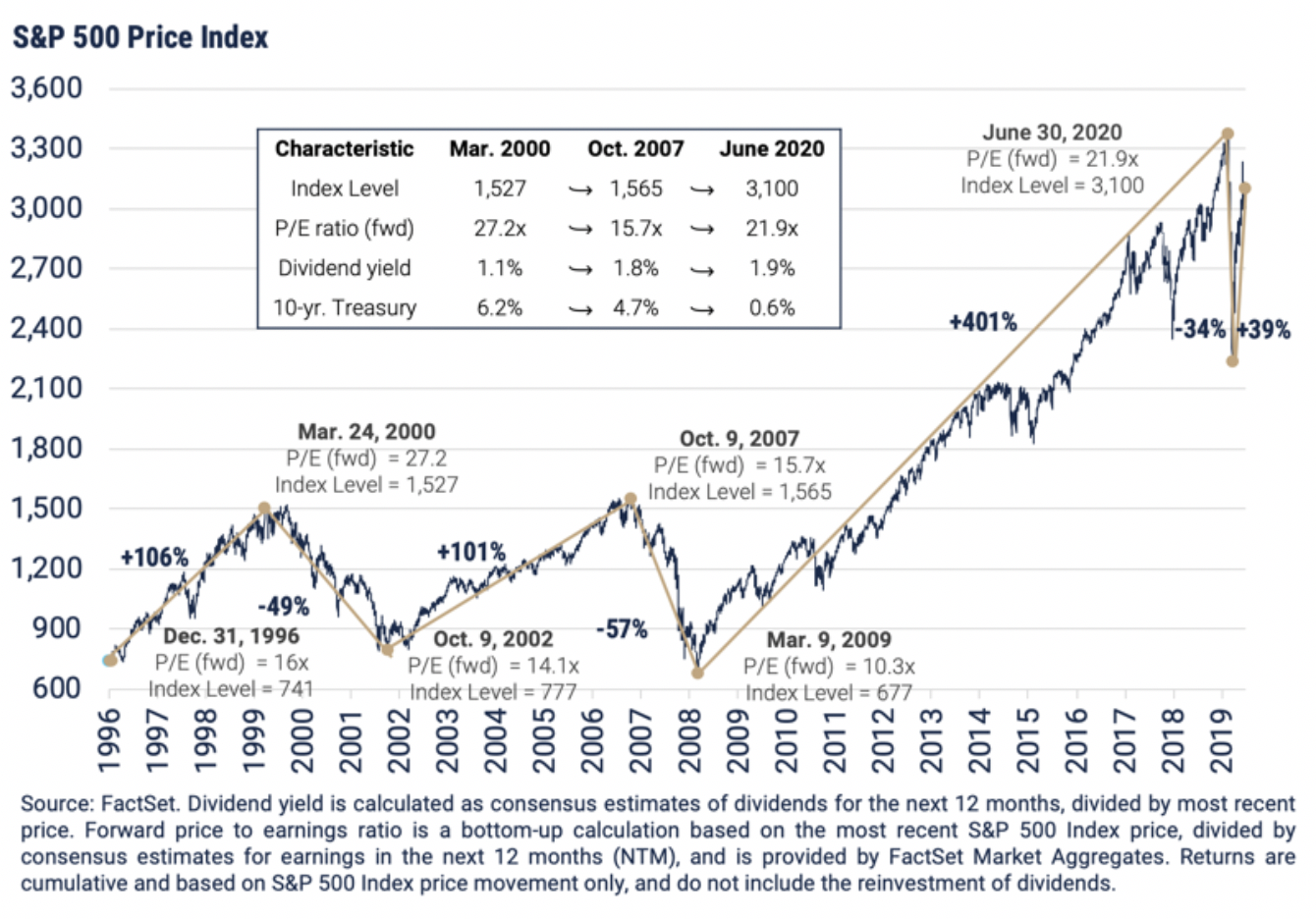

If we had foreseen these challenging circumstances 12 months ago, we wouldn't have predicted that the stock market would be higher today than it was then, but the S&P 500 is up 7.5% over the last year.

In fact, U.S. stocks produced their best quarterly returns in more than 20 years in the second quarter with the S&P 500 up 20% - its best percentage gain since the fourth quarter of 1998.

The NASDAQ composite, which is heavily weighted toward big technology companies (Microsoft, Apple, Amazon, Google and Facebook are its five largest components), was up even more with a 31% gain. These numbers lead to several questions: why has the stock market performed so well in the face of the challenging backdrop, can that performance continue, and most importantly what are the implications for investors with varying investment objectives?

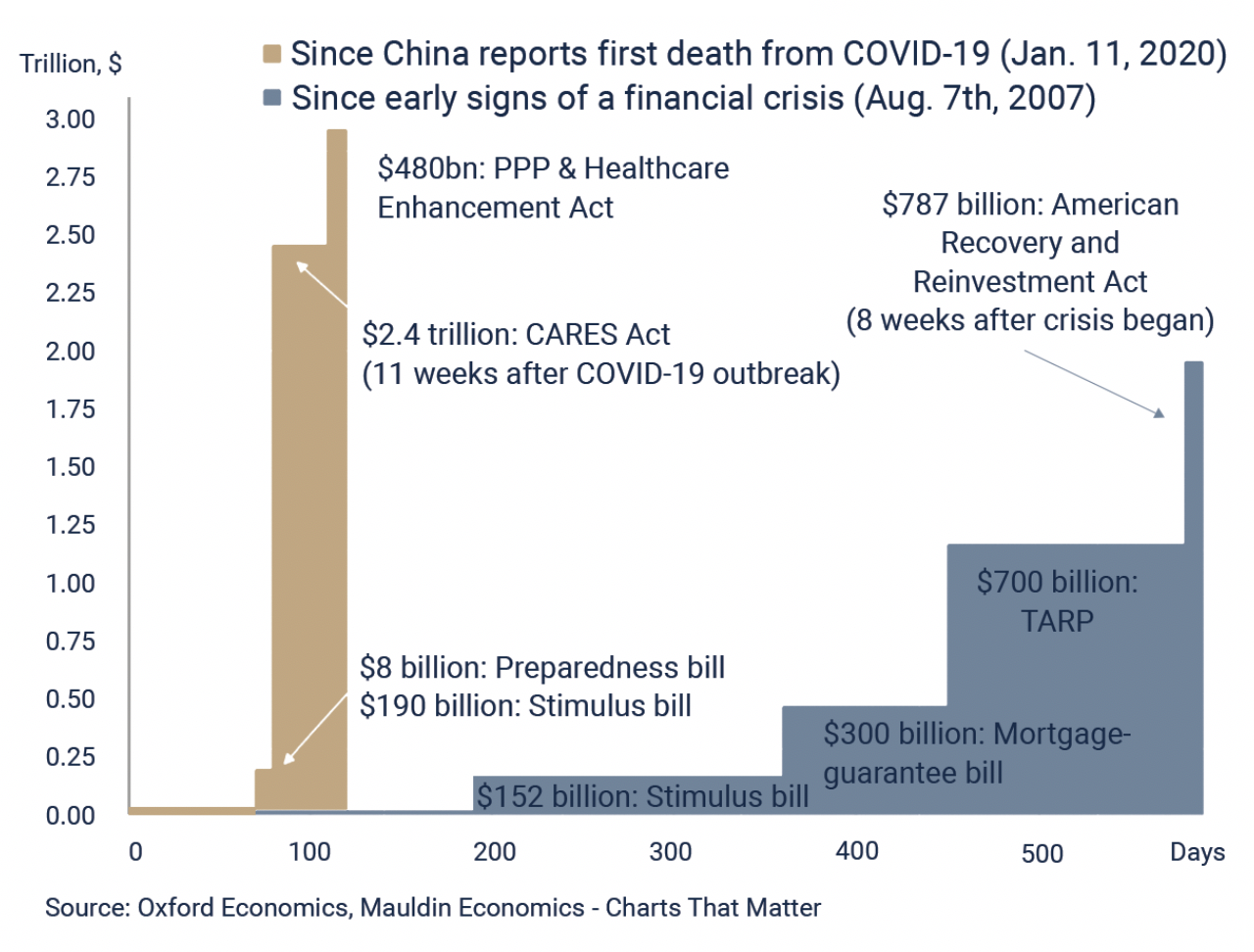

The answer to the first question is relatively straightforward: liquidity. The massive monetary stimulus by the Fed coupled with the huge fiscal boost provided by the Paycheck Protection Program (PPP) and Health Care Enhancement Act (combined $480 billion), the Coronavirus Aid, Relief and Economy Security Act (CARES Act) ($2.4 trillion) and the Families First Coronavirus Response Act ($198 billion) together served as a bolus of adrenaline right in the heart of the U.S. economy.

To put those numbers in context the government injected almost 50% more money into the US economy in the three months following the onset of the coronavirus than it did in the first two years of the financial crisis beginning in 2008. Very importantly the majority of the support this time went directly into the pockets of consumers while most of the support after the financial crisis was used to shore up the banking system and never made its way into the real economy.

The second question is more difficult to answer. Certainly, there is a disconnect between the pace of the markets’ recovery and that of the economy. Despite the surprisingly strong initial snapback in the employment figures it will probably take years for the US workforce to return to the record levels we enjoyed in late 2019. While virtually all economists agree the second quarter was an economic disaster, with GDP declining at a 30% - 40% annual rate, forward-looking estimates vary widely based upon the unpredictable factors that will drive the pace of economic reopening and subsequent recovery. Those factors include not only the medical issues: course of the disease, changes in mortality rates for those who catch it and the progress of scientists seeking treatments and vaccines, but also policymakers’ responses to the data and individuals’ choices about the tradeoffs between returning to “normal life” and risking infection.

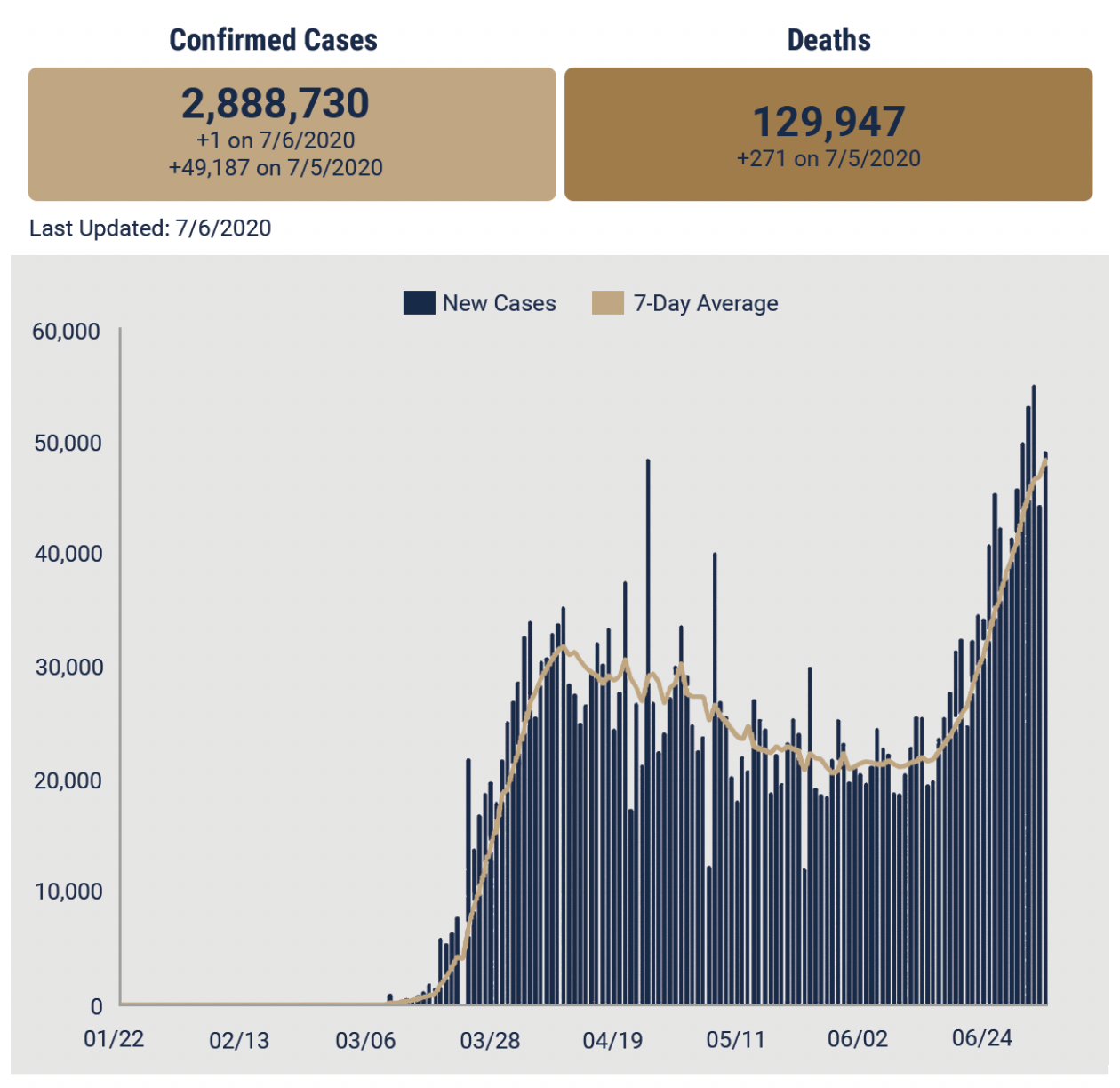

The trajectory of new cases in the U.S. continues to rise and states that were quick to reopen are seeing spikes in infections and hospitalizations - increasing the risk of more shutdowns and a slower recovery. Other potential risks to the US economy are the end of the enhanced unemployment benefits scheduled this month and the threat of austerity at the state and local government level if tax revenues continue to decline. The importance of US consumption to the global economy and the role that our capital markets play in global finance suggest that the domestic policy response will play a crucial role in determining the pace and shape of the global macroeconomic recovery and financial markets performance.

POSITIONING & OUTLOOK

On the heels of the unprecedented rally in the stock market and given the backdrop of risk and uncertainty, we remain cautious in our portfolio positioning. Our guiding theme since the pandemic began has been resilience. The theme of resilience applies most importantly at the portfolio policy level, where the overall mix of assets in each client's account is calibrated to meet that client's needs for income, portfolio appreciation and capital preservation. With stocks back near record highs and interest rates back at record lows, those objectives seem to run counter to each other, and resilience in the form of capital preservation moves to the forefront at moments of high volatility. Within each portfolio, the resiliency theme manifests in our selection of asset classes and individual securities.

For now, it is still all about COVID-19. The shape of the longer-term economic recovery depends upon the path of the disease and policymakers’ responses. Governments continue to provide massive amounts of stimulus, but government support of economies has strings attached and can’t last indefinitely.

Important Disclosures

Unless otherwise indicated, performance information for indices, funds and securities as well as various economic data points are sourced from FactSet as of June 30, 2020.

Wilbanks, Smith and Thomas, LLC (WST) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. This material is not intended to replace the advice of a qualified tax advisor, attorney, or accountant. Consultation with the appropriate professional should be done before any financial commitments regarding the issues related to the situation are made. The opinions expressed herein are those of WST and may not actually come to pass. This information is current as of the date of this material and is subject to change at any time, based on market and other conditions. Although taken from reliable sources, WST cannot guarantee the accuracy of the information received from third parties

An index is a portfolio of specific securities, the performance of which is often used as a benchmark in judging the relative performance to certain asset classes. Index performance used throughout is intended to illustrate historical market trends and performance. Indexes are managed and do not incur investment management fees. An investor is unable to invest in an index. Their performance does not reflect the expenses associated with the management of an actual portfolio. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. All investing involves risk including loss of principal. Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market. Past performance is no guarantee of future results.

This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.