1Q 2023 | Economic & Markets Commentary

“Anyone who isn't confused really doesn't understand the situation.” ― Edward R. Murrow

"When you find yourself in a hole, stop digging." -Will Rogers

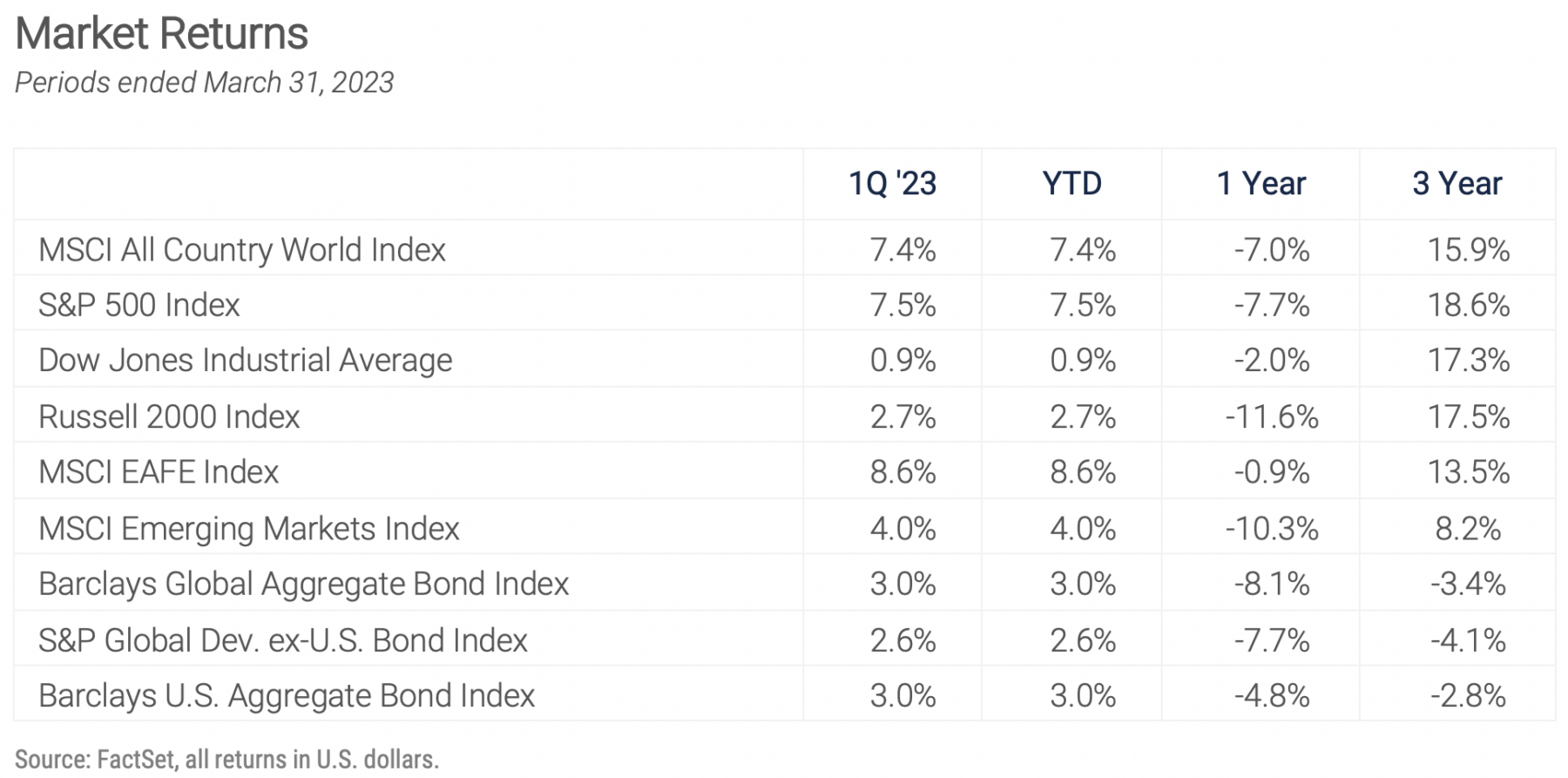

Global investment markets generated broadly positive returns in the first quarter, shaking off a banking crisis and continued concerns about the economy and interest rates. When the dust settled on March 31, the S&P 500 was up 7.5% for the quarter, the EAFE index of international stocks had gained 8.6%, and bonds had bounced back from the drubbing suffered in 2022 with the U.S. Aggregate Bond index up 3.0%. While those positive stock returns mask lots of intra-quarter volatility and a huge dispersion of performance across sectors, they also reflect modest optimism about the overall economic outlook. So far, the widely anticipated recession has failed to materialize and inflation, while still well above the Fed's long term target, continues to ease.

We pick up the commentary this quarter where we left off in January: with a focus on inflation, the Fed, and the economic risks associated with the Fed's commitment to containing inflation. Those risks were exacerbated and complicated by the (hopefully momentary) instability of the U.S. banking system in March following the failures of Silicon Valley Bank and Signature Bank. Despite those increased risks investors chose to focus on the hope that any economic drag created by tighter bank lending standards following the crisis would allow the Fed to pause the rate hike cycle, creating a "bad news is good news" moment for the markets and pushing stocks strongly higher in the last week of the month.

The expectations for the economy expressed by the stock and bond markets diverged this quarter. After starting on a strong note, stocks traded in a fairly narrow range before the late-quarter surge, indicating a sanguine outlook for the economy and corporate profits despite the banking crisis and the Fed's determined tightening. Rapidly declining bond yields, on the other hand, reflected concerns about the increasing likelihood of a recession. There is a case to be made for each side of the debate. Job openings, while still plentiful, declined unexpectedly in February to under 10 million, the lowest level since May 2021. Headcount reductions at big technology companies have been in the headlines for several months and are now spreading to consumer giants Walmart and McDonalds. Similarly, capital spending by S&P 500 companies is expected to increase 6% this year with boosts coming from the Inflation Reduction Act and the onshoring trend we discussed last quarter, but recent announcements from Disney, Meta, Amazon, and others indicate an increasingly cautious approach to big projects. Each of those companies has rolled back the size and timing of previously announced capital investments. So, while the longer term trends remain positive, the short term indicators on employment and cap ex have turned decidedly negative.

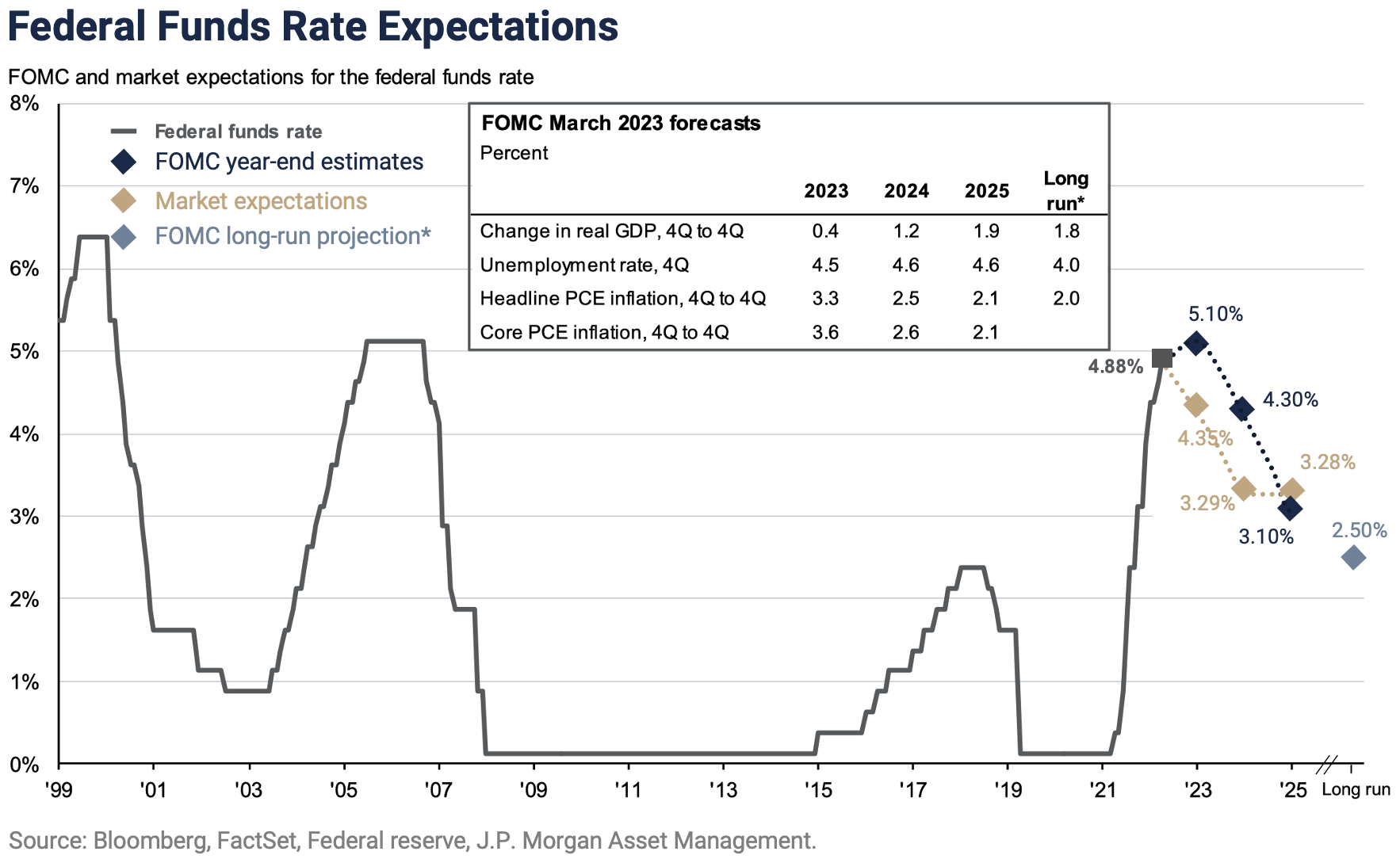

Despite concerns about the stability of the financial system and the health of the economy, the Fed continued tightening at its March meeting, raising the Fed funds rate another 25 basis points to a range of 4.75% to 5%, the highest level since 2007. The choice confronting the Fed comes down to living with higher inflation versus risking crushing the economy, and Fed policy has come under increasing scrutiny this year.

Critics contend they waited too long to begin raising rates in 2021 after wrongly asserting inflation would be "transitory" and are compounding the mistake by overtightening now despite the economic clouds on the horizon. Applying Will Rogers' advice to the matter, those critics contend the Fed is in a hole and needs to stop digging.

The graph above reveals the widening gap between market expectations for the Fed funds rate and FOMC guidance. The market now clearly expects rate cuts before the end of 2023, with the futures market calling for a 4.4% rate at year-end versus the FOMC's terminal rate estimate of 5.1%. The conundrum facing Fed policymakers is reflected in the revisions to their economic outlook after the March meeting. Looking back as far as 2021 the Fed has consistently reduced its expectation for economic growth for the remainder of 2023 and 2024 while increasing its inflation estimates for both headline inflation and core inflation for both years. The Fed believes the war on inflation has yet to be won, even at the cost of economic growth.

For years, the economy and financial markets enjoyed a tailwind of low interest rates and abundant liquidity (provided by the Fed's quantitative easing) which served to dampen volatility and inflate asset values. Now, with higher interest rates increasing the cost of capital for companies and raising the cost of borrowing for consumers, the resilience of the economy is in question. Virtually all economists, including Chairman Powell, agree monetary policy works with a lag; in fact, in a November briefing, the Atlanta Fed indicated it could take 18 months to two years for tighter monetary policy to materially affect inflation. Many believe the Fed should have paused in March to give the prior hikes time to work through the system.

From our perspective, the twin supply shocks caused by the pandemic and the war in Ukraine were the main factors contributing to inflation last year but are behind us now, and with supply chains returning to normal, we don't foresee additional supply-side shocks. Tighter credit conditions resulting from central bank tightening are also dampening the inflation outlook. That combination of improving supply and decreasing demand should lead to diminished price pressures, which should, in turn, give the Fed some breathing room.

All things considered, we think the likelihood of a mild recession this year remains high, particularly if the Fed maintains its current course. The crucial question that will arise is whether in the event of a recession the financial markets experience a soft or hard landing. While the economy might manage a relatively smooth downturn, we recognize that a different outcome is possible for the financial markets.

EQUITY MARKET OVERVIEW

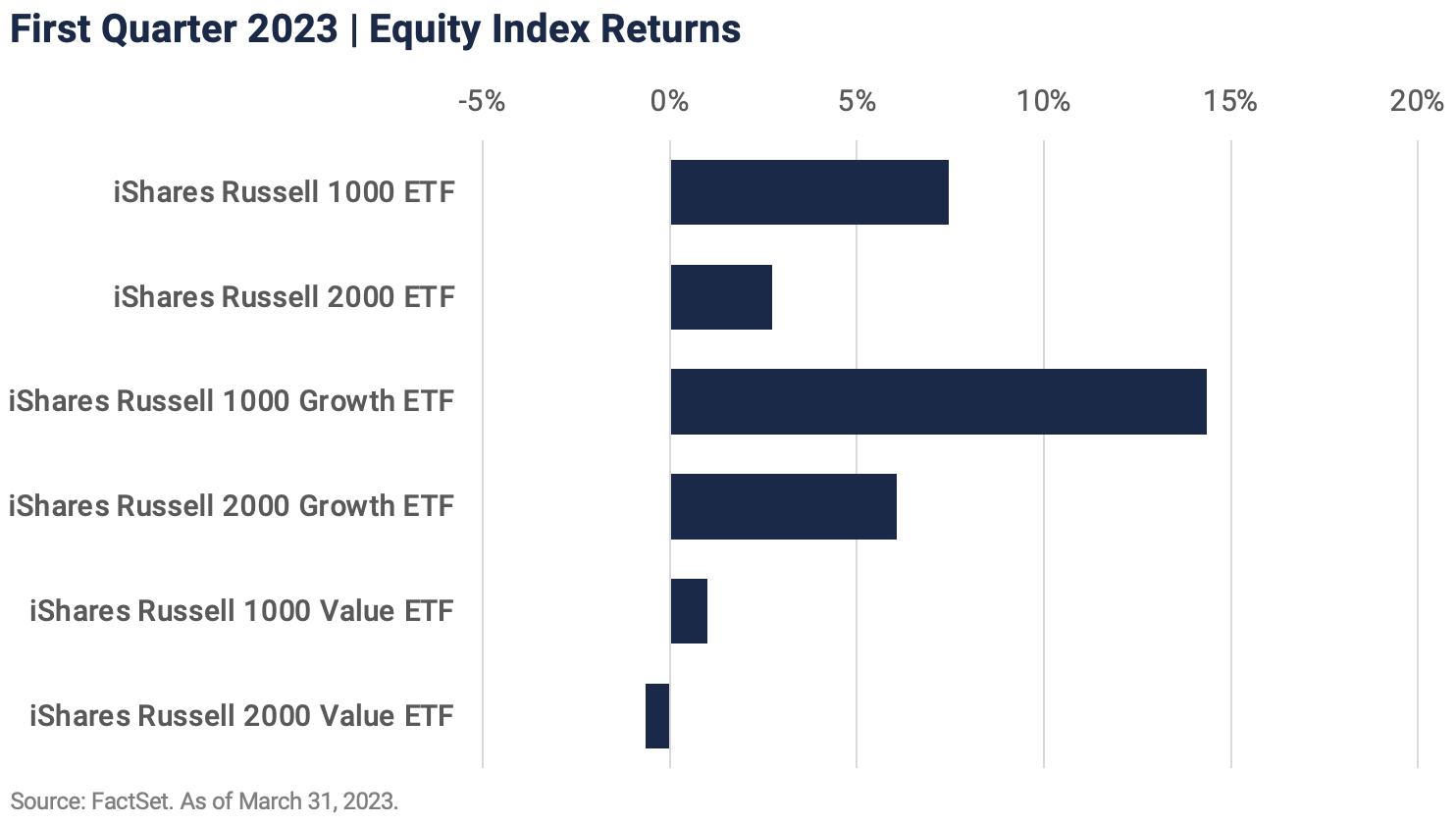

As we mentioned at the outset, the strong performance of the broad stock indexes in the first quarter masked significant volatility and variability of returns across equity asset classes. Short-term returns were driven almost exclusively by the shifting expectations for Fed policy, so market volatility tracked the release of economic data. The S&P 500 gained 6.3% in January, fell 2.4% in February, and finished March up 3.7%, ending the quarter with a total return of 7.5%. A look below the surface reveals that most of the return in the equity markets over the first quarter was driven by a rebound in the large-cap growth sector as interest rates declined. After falling almost 30% last year, the Russell 1000 Growth index rose 14.4% in the first quarter, far outpacing the 1.1% gain in the Russell 1000 Value index and the 2.7% increase in the small cap Russell 2000 index. The six largest stocks in the S&P 500, all technology-focused growth stocks, made up 20% of the index and accounted for 70% of the return last quarter: Apple, Microsoft, Amazon, Alphabet, Nvidia and Tesla. Financial stocks, on the other hand, reflected the concerns surrounding the banking system and finished the quarter down 5.9%. Despite those healthy returns, U.S. stocks remain 13.5% below their record high set on January 3, 2022, and will have to overcome significant headwinds to regain that level this year. Valuations are more reasonable than at the market peak, but stocks are still not inexpensive because projected earnings continue to fall. Even a mild recession would weigh on corporate profits, and expectations have been falling. In fact, corporate earnings have already entered a recession.

According to Yardini Research S&P 500 earnings are expected to grow just 1% in 2023 over 2022, and both the first and second quarters are expected to see earnings declines. To the extent this year's earnings estimates are back-end loaded those expectations are particularly vulnerable to economic weakness in the coming months. The one-year forward price-to-earnings ratio for the S&P 500 has declined from 22 times projected earnings in January 2022 to 17 times earnings at the end of March, still high by historical standards and particularly in light of the reduced earnings estimates and today's higher interest rates. In the coming weeks, corporate earnings reports will reveal how companies and consumers have been impacted by the changing economic fundamentals.

BOND MARKET OVERVIEW

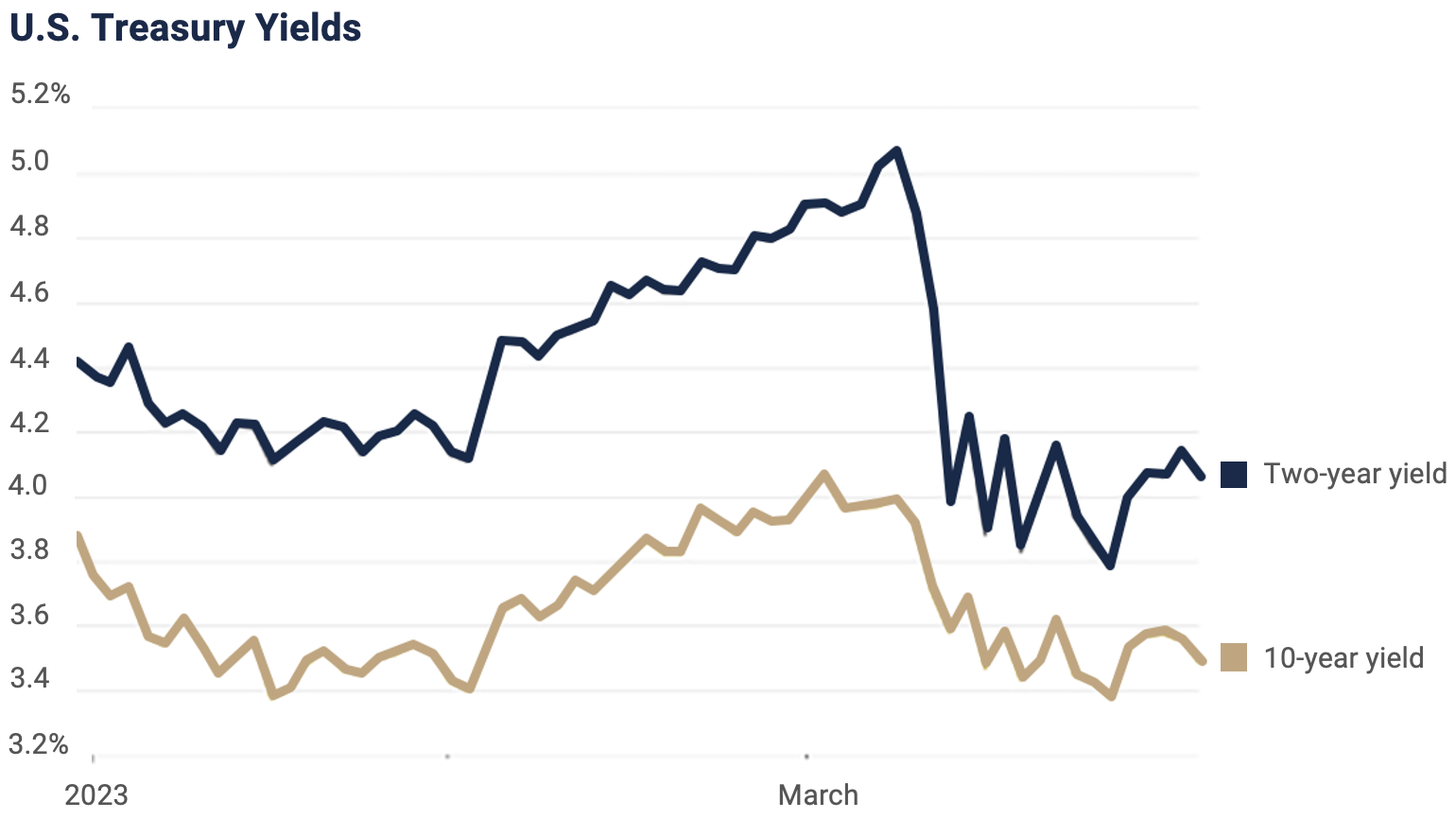

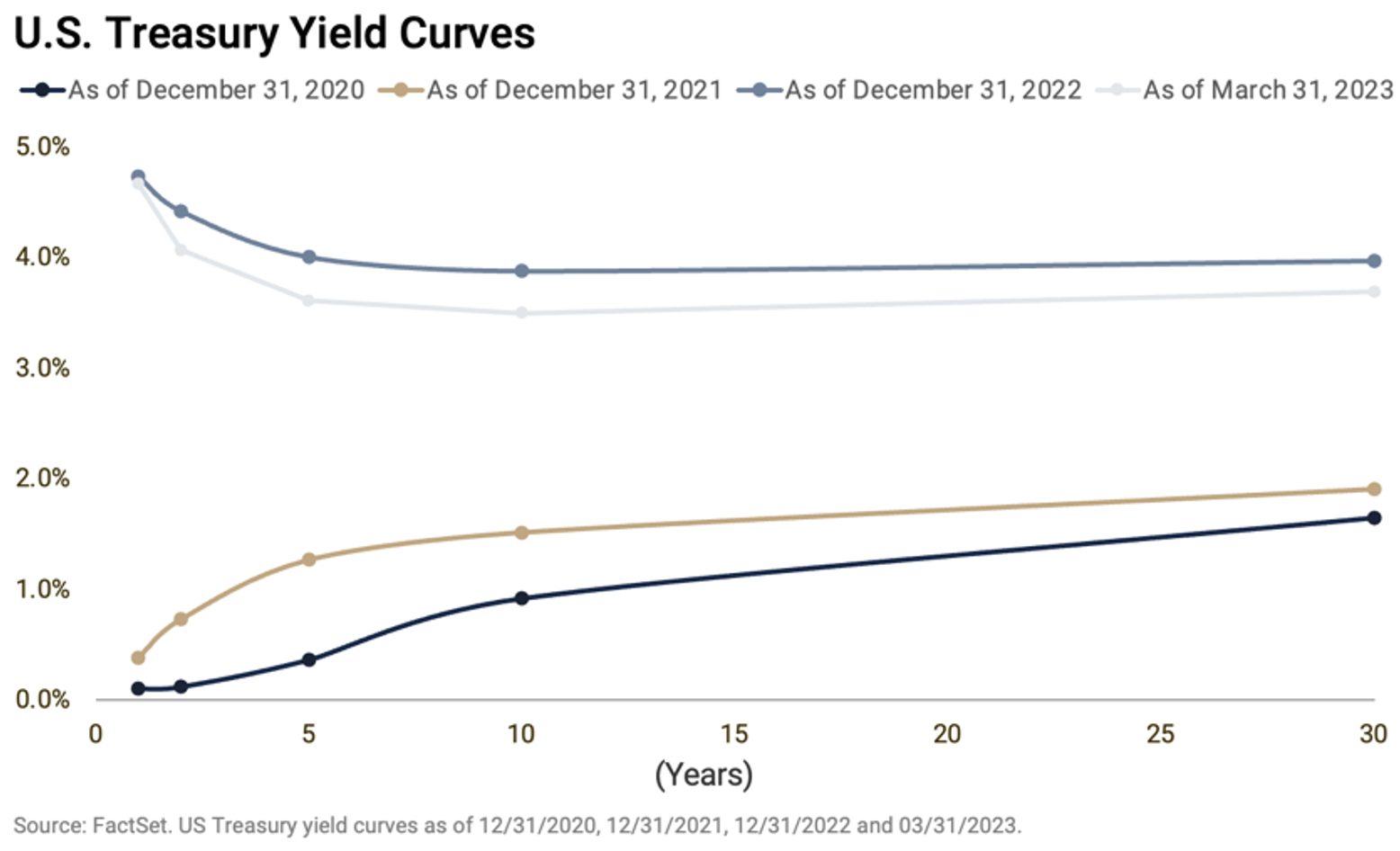

On the heels of the bond market's worst year in history in 2022, yields continued to drift higher for the first two months of the quarter. That trend ended abruptly in March when the failure of SVB left investors scurrying for the safety of Treasury bonds and reset expectations for the path of Fed policy. The speed and magnitude of the rally in rates was unprecedented, as shown below.

The net result for the quarter was a roughly parallel shift in the yield curve, with rates dropping about 30 basis points on 3, 5, and 10-year Treasuries and a bit less on longer maturities. The curve continues to price in nearly a full percentage point of rate cuts beginning in June, reflecting the bond market's forecast of additional stress on the banking system requiring more central bank support and/or a recession later this year. That assumption could change quickly if inflation remains stubbornly high, a possibility investors need to prepare for. The market is definitely not expecting the Fed to continue tightening in the second half, despite its consistently hawkish guidance.

The best news for bond investors today is that while fixed income investments tend to perform well in environments of uncertainty, bonds are particularly appealing now after last year's repricing drove interest rates up to today's attractive levels. At these levels, short duration bonds provide both income and volatility protection, and with the yield curve inverted, we are able to maintain a very conservative portfolio structure and still enjoy the best of both worlds, low risk, and reasonable income. Blackrock's Rick Rieder summed up the opportunity available to today's bond investors: by maintaining a short maturity, high-quality portfolio, we are able "to make a little bit of money a lot of times without a lot of risk." That's a significant change from the last decade-plus, which saw paltry yields across the spectrum of fixed income assets, a situation that forced investors to increase portfolio risk to achieve reasonable returns.

Corporate bonds play an important role in our portfolios and were impacted by the issues in the banking sector last quarter. While credit spreads widened on concerns about the health of the economy, those wider spreads were more than offset by the general decline in interest rates. Intermediate-term corporate bonds returned over 2.5% for the quarter. Overall, we believe corporate bonds continue to look attractive at today's yield levels, and we remain focused on high-quality, liquid bonds and funds.

Municipal bonds also started the year on a strong note, with a total return on the S&P Municipal Bond index of over 3%. Sharply higher yields in 2022 created an attractive starting point for investors seeking tax-protected income, and with revenue and credit quality improving for state and local bond issuers, the risk-reward balance for muni bonds looks positive. Unlike the U.S. Treasury yield curve, the tax-exempt municipal bond curve remains upward-sloping, so we are able to extend the duration of muni portfolios a bit longer than we can in taxable accounts, locking in today's higher yields.

ASSET SAFETY

The failures of Silicon Valley Bank and Signature Bank shocked investors and raised concerns about the overall stability of our financial system. For many of our clients, those events led to understandable worries about the safety of their investment accounts held at institutional custodial firms. Undoubtedly, the problems facing U.S. banks have broad implications for the global economy and investment markets. Even so, investment assets (stocks, bonds, mutual funds, and money market funds) held in custody at reputable brokerage firms are not at risk of loss in the unlikely event that one of those firms goes out of business.

In response to our inquiry, the risk management department at one of our custodial partner firms sent us a reassuring overview of the security measures in place to protect client assets. The most important thing to remember is that securities held at a brokerage firm are owned by the client and are not part of the firm's balance sheet assets. This means that client assets are safeguarded by the SEC's Security Protection Rule, which prevents brokerage firms from using customer assets to finance their own business activities. Client assets are kept separate from the firm's assets and are generally held at a third-party depository institution, such as the Depository Trust Company or the Bank of New York. Brokerage firms are required to comply with reporting and auditing regulations that ensure they abide by the requirement to segregate client assets. In the unlikely event that a brokerage firm becomes insolvent, these segregated assets are not available to creditors and are protected from other creditor claims. They remain the client's assets.

In addition to the provisions of the Security Protection Rule, brokerage firm client assets are also safeguarded by the Securities Investor Protection Corporation (SIPC). SIPC insurance is activated in the event a broker-dealer goes bankrupt, and client assets are missing due to fraud or other causes. According to Schwab and the SIPC, 99% of eligible investors have fully recovered their assets in cases where brokerage firms have failed. In summary, we are confident your assets are held by a strong, stable, reputable custodian, are segregated as required by the Security Protection Rule, and are protected by the SIPC. So, while there is much to consider in terms of risks facing portfolios, custodial asset safety is not a concern.

SUMMARY

Heading into the second quarter, the drivers of the investment markets remain unchanged: inflation, the Fed, and their impact on the economy. So far, the Fed has remained true to its commitment to reduce inflation even at the expense of economic growth. With inflation easing and the economy slowing, the Fed's handling of this stark trade-off will remain front and center, and the stakes are high.

We witnessed last quarter the difficulties banks face in holding deposits as interest rates on Treasury bills and money market funds surge ahead of the rates the banks can afford to pay for their inventory, cash on deposit. So far, it appears a bank crisis has been averted, but credit will continue to tighten as banks are forced to either pay more for deposits or raise the interest rates on their loans. Tighter credit means slower economic growth.

The first quarter's volatility reinforced the benefits of diversification and a long-term view. Investors who bet that interest rates had to continue to rise or that equities would continue to fall were caught flat-footed last quarter. As always, volatility and uncertainty create opportunity. We remain conservatively allocated in balanced accounts but have taken advantage of higher short-term interest rates and rebalancing of equity portfolios where appropriate.

Notes & Disclosures

Wilbanks, Smith & Thomas Asset Management (WST) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation, or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. This material is not intended to replace the advice of a qualified tax advisor, attorney, or accountant. Consultation with the appropriate professional should be done before any financial commitments regarding the issues related to the situation are made.

This document is intended for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred, or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty and does not represent the performance of any specific investment strategy.

Some of the information enclosed may represent opinions of WST and are subject to change from time to time and do not constitute a recommendation to purchase and sale any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.