1Q 2021 | Economic & Markets Overview

“The party is just getting started. This is where the fun starts.” - Kobe Bryant

“The Fed’s job is to take away the punch bowl just as the party gets going.” - William McChesney Martin, Former Fed Chairman

The global economic recovery picked up steam in the first quarter as optimism grew that the darkest days of the COVID pandemic are behind us. Growth surged in the U.S. as encouraging progress on vaccinations, continued monetary support from the Fed, and another dose of fiscal stimulus in the form of the $1.9 trillion American Rescue Plan Act boosted confidence about the pace and breadth of the reopening of the domestic economy. Based on current trends the U.S. economy is expected to regain its pre-pandemic size this year after contracting 3.5% in 2020. While the definition and timing of herd immunity remain open questions, it seems clear the current pace of vaccinations coupled with the growing proportion of the population that has recovered from COVID will support a continued pick-up in economic activity in the second half of the year. As we will discuss below the new round of stimulus brings long-term risks, but in the short term it's expected to boost 2021 U.S. economic growth into the 6% to 7% range, a much more robust recovery than almost anyone envisioned six months ago.

Looking around the world we see uneven recoveries but positive trends in nearly all zones. Regional differences are attributable to the pace of vaccine rollouts, varying government policies, and fundamental factors like reliance on commodity trade or tourism. Only China has recovered as quickly as the U.S., and the International Monetary Fund (IMF) expects 8.5% year-over-year growth there in 2021. Europe on the other hand has stumbled in its vaccine programs, prompting more restrictions and slowing the recovery in the Euro area. We remain optimistic the progress in the developed economies will bleed over into emerging markets despite the logistical challenges they face getting their populations vaccinated.

As sentiment improved over the course of the quarter risk assets rallied, especially in beaten-down cyclical and economically sensitive sectors like value and small-cap stocks. The accelerating recovery and associated inflation fears created a challenging environment for duration-sensitive assets including long-maturity fixed income and growth stocks. Bonds took a drubbing in the quarter as investors took note of the rising inflation indicators and outlook.

As we reflect on the amazing scientific and economic progress since the market low on March 23, 2020, we remain wary of the potential challenges ahead. Other than unforeseen problems with vaccines or a major outbreak of a new strain of COVID, the most important risk we see is an unexpectedly strong uptick in inflation that forces the central bank to tighten monetary conditions abruptly. The juxtaposition of the quotes at the top of this letter frames the most important question investors face today. Clearly, the economic expansion is picking up momentum, but how long will the expansion be allowed to run before the Fed steps in to quell inflation?

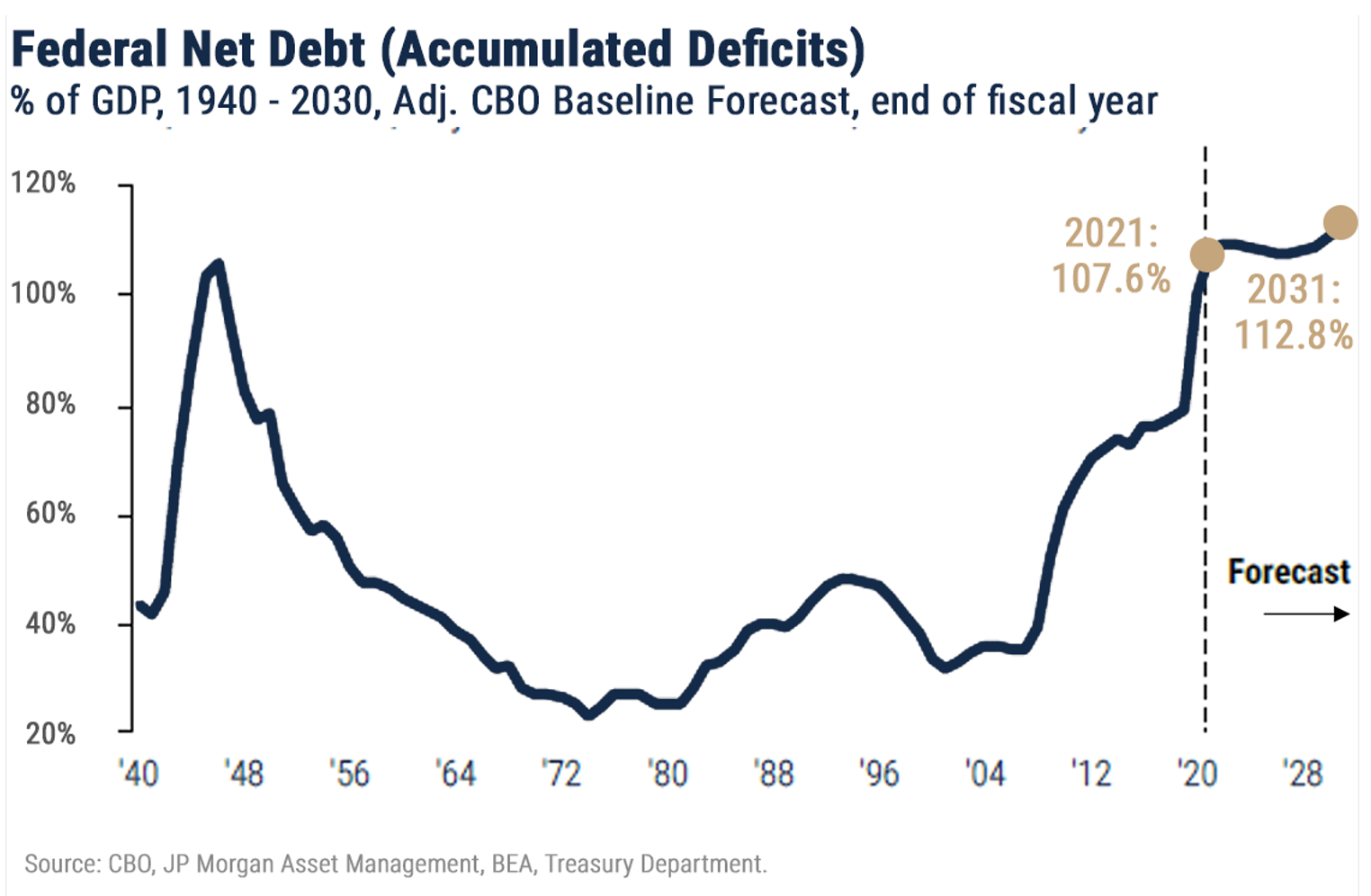

The unprecedented infusion of liquidity into the economy by the Fed and Treasury department in response to the COVID pandemic has been the catalyst for the domestic economic rebound and, to a large extent, the global recovery. Now the risk of an overshoot in the most recent stimulus package in light of already-robust global growth, and the burgeoning debt needed to fund the package’s initiatives, could have unintended results. Government stimulus over the past year has massively increased our already daunting national debt, forcing the Treasury and Federal Reserve to print trillions of dollars and buy the bonds issued to finance that borrowing. The prospect of a budget surplus in the foreseeable future is dim, but Washington seems unconcerned about our ever-expanding liabilities. As Blackstone market strategist Byron Wein points out, you hardly ever hear anyone say "we can't saddle our grandchildren with this debt burden" anymore. Instead, and without having directly acknowledged it, our policymakers have adopted Modern Monetary Theory, the risky premise that we can print money endlessly without triggering inflation.

At some point, excess liquidity should spur inflation, but so far that hasn't happened. If it does, and if the Fed finds itself in a position where it's forced to raise interest rates, our deficits and debt will be very expensive to support. As it stands Federal indebtedness will exceed GDP for the first time since World War II in 2021, and while low interest rates have kept the cost of servicing that debt manageable, the budgetary implications of higher interest costs could be staggering.

Equity Market Overview

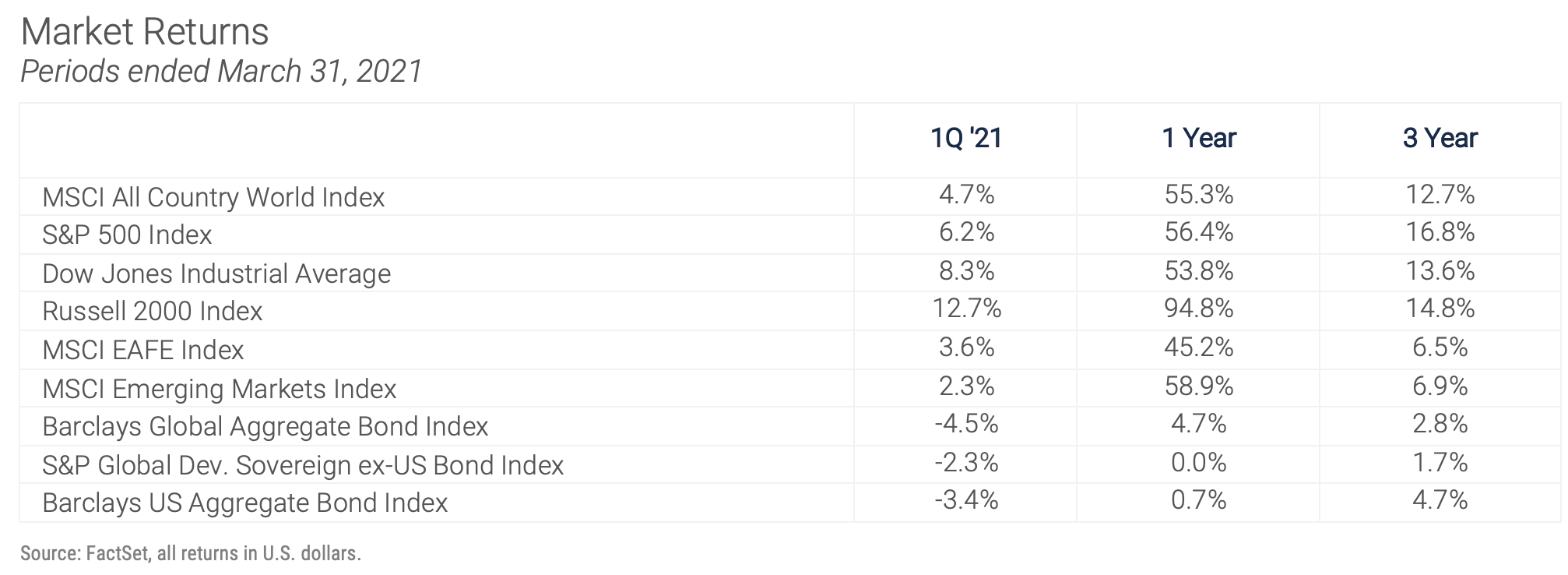

While the good news on the economy heightens the risk of inflation and higher interest rates, equity investors remained focused on the positives during the first three months of 2021. The market rotation away from technology-heavy growth stocks and into more cyclical small cap and value stocks continued. The S&P 500 Index returned 6.2% for the quarter while the Russell 2000 Small Cap Index surged 12.7%, and the Russell 1000 Large Cap Value Index posted an 11.3% return. Those strong returns compare very favorably with the meager 0.9% increase in the Russell 1000 Large Cap Growth Index. Those return differentials, following on the heels of similar trends in the fourth quarter of last year, closed the performance gaps that opened during the market freefall in the first quarter of 2020 and the subsequent blastoff of large-cap growth stocks in the second and third quarters of last year. Over the trailing 12 months ended March 31, 2021, small-cap stocks as measured by the Russell 2000 are up 95% versus a 62% return for the Russell 1000 U.S. large-cap index.

Returning to the central theme of this letter, the performance of the equity markets for the remainder of this year will depend upon the interplay among the reopening of the economy, inflation, and interest rates. As Fed Chairman Jerome Powell has pointed out the economy is at an inflection point. The "just right" scenario, and the one the Fed currently views as most likely, would see a short-term bump in price levels this summer as pent-up demand is released but no secondary effects or sustained inflation above the 2% level during the fourth quarter and into 2022. That environment would be positive for equities and, as we discuss below, defensively postured bond portfolios.

Setting aside the possibility of a major resurgence in COVID, which would obviously have widespread negative implications for the global economy and markets, the other two scenarios we envision both include faster than expected economic growth and higher than expected inflation. In that environment, the Fed will face an important fork in the road. If the central bank remains accommodative and allows inflation to drift higher than the current 2% target, market forces will likely push interest rates higher. Stocks generally navigate rising interest rates reasonably well if the driver of higher yields is improvement in the fundamental economic picture, so modest increases in yields in the context of healthy growth and supportive Fed policy could extend the equity rally. It's a different story if interest rates rise because the market anticipates tighter monetary policy. If, later in the year, central banks decide they need to act aggressively to head off inflation by withdrawing liquidity, then the adage "don't fight the Fed" will apply and many investors will “derisk” portfolios, selling stocks and moving money to the sidelines, creating challenging conditions for both stocks and bonds.

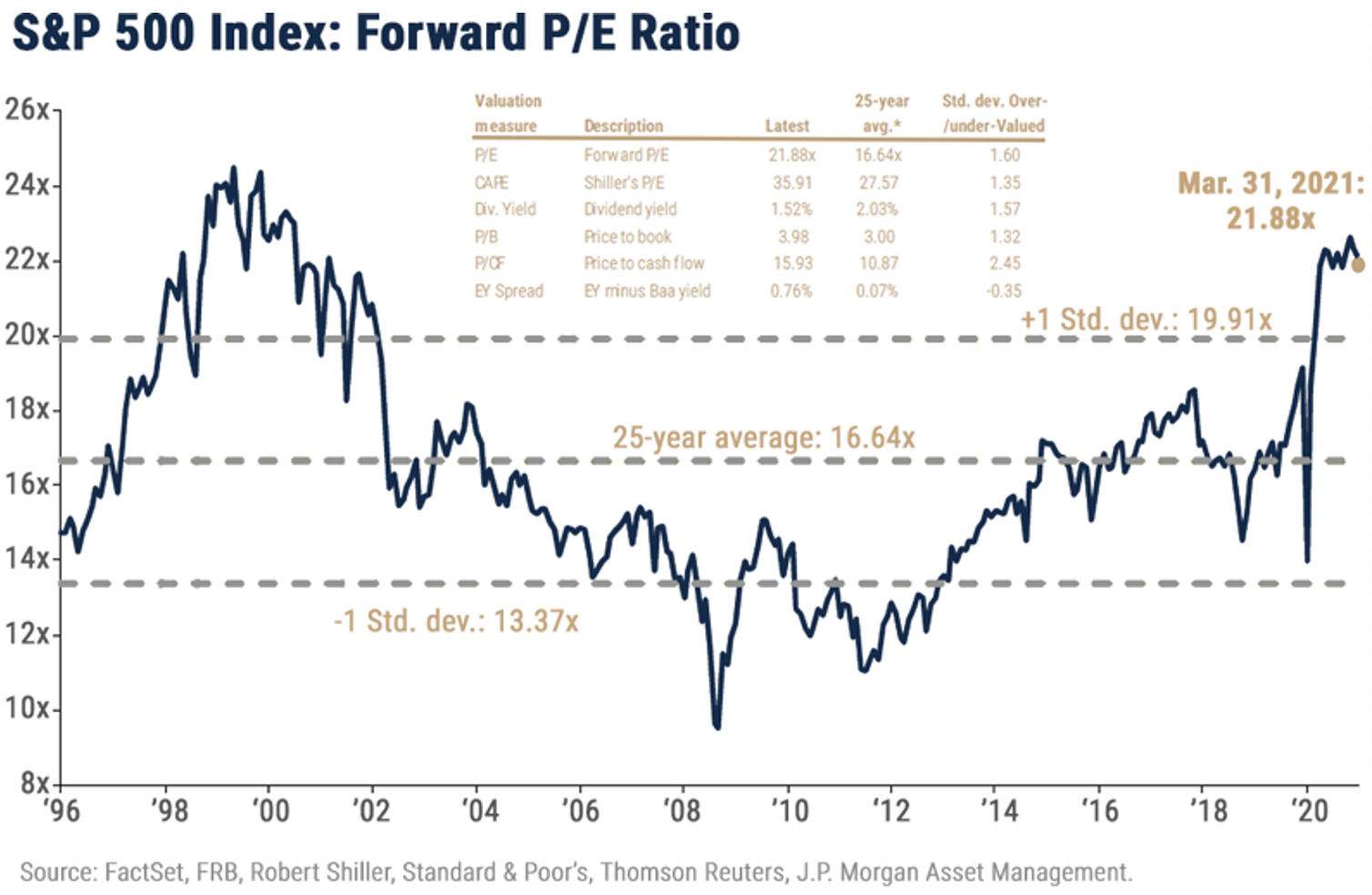

Even in the first scenario, the risk of stock market volatility is higher than normal because stock valuations are higher than normal. As the chart below demonstrates, the forward P/E ratio of the S&P 500 is in risky territory, not unprecedented, but we have to look back to the Internet bubble to find a time when valuations were as high as they are today.

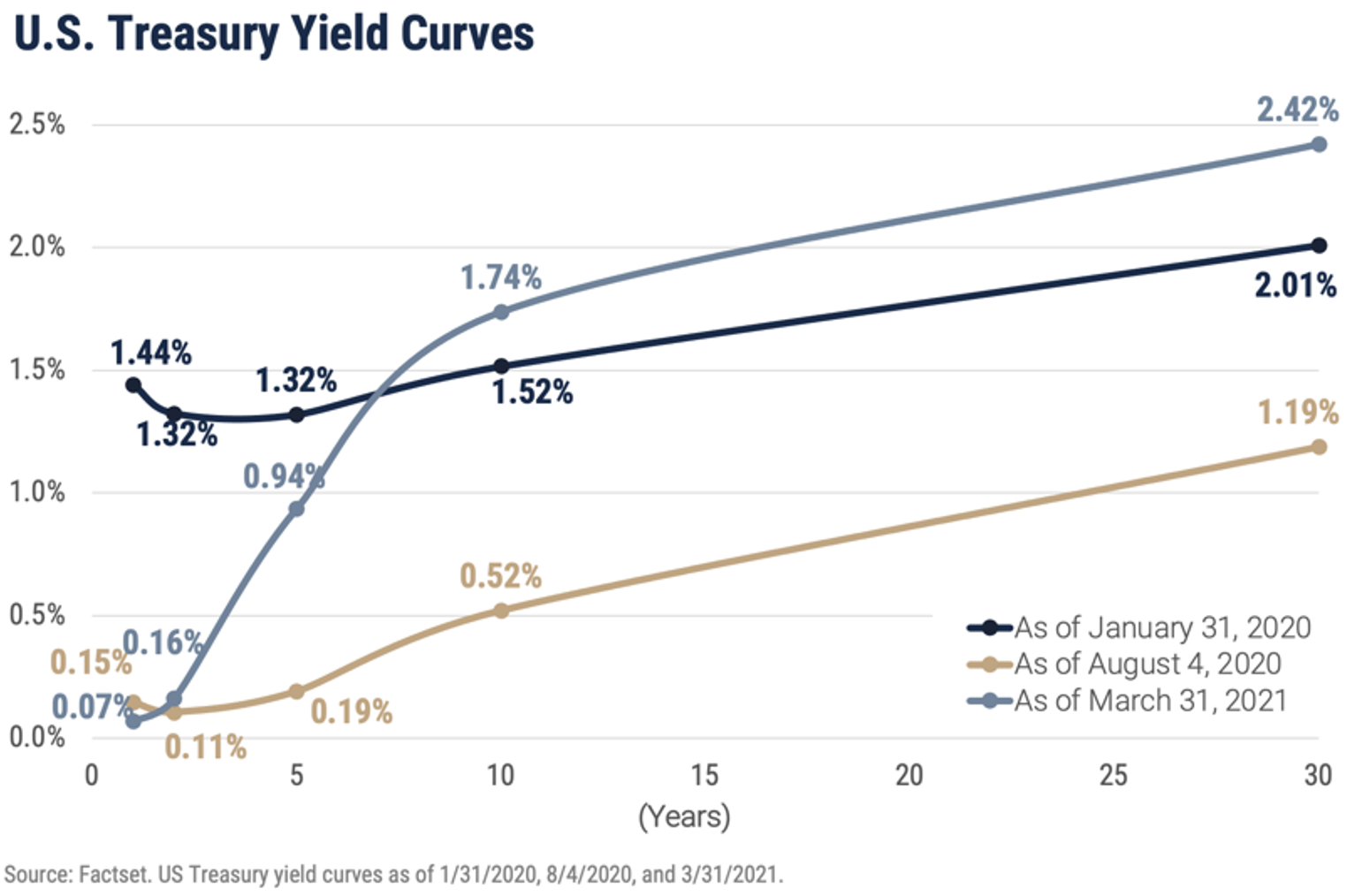

Maybe more important for equity investors as we look forward and acknowledge the possibility that interest rates will continue to rise is the comparison between the dividend yield on stocks and the income available on bonds. As it stands now the yield on the S&P 500 is about 1.5%, which was very attractive in August when the yield on the 10-year Treasury note was 0.5%. We wrote at the time about the "TINA trade" (There Is No Alternative) which meant that investors were willing to buy risky assets like stocks and accept the inherent volatility in return for the income, which although paltry by historical standards was generous relative to bonds. With the 10-year Treasury yield having risen to its current 1.75% level there is indeed an alternative to that 1.5% dividend yield, and the bond alternative will be increasingly attractive if rates continue to rise.

In summary, the powerful recovery of the global equity markets over the past 12 months was driven by the surprisingly strong economic bounce back, which in turn was driven to a large extent by government intervention. While central banks remain committed to accommodative and supportive monetary policies, at some point the world's economies and markets will need to stand on their own feet as stimulus is withdrawn. Certainly, much if not all of the good news about the economy is already baked into stock prices, so progress from here will be more challenging.

Bond Market Overview

Bond yields leaped higher during the first quarter as the recovery accelerated and investors grew leery of rising inflation. Again, the market’s primary concern is a sustained uptick in inflation in the second half of the year, and inflation expectations continued to trend higher throughout the quarter. The resulting weakness in fixed income markets over the course of the quarter was widespread, and long duration Treasuries suffered the most with double-digit price declines. Even short-term government bonds saw slightly negative returns.

The broad bond benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, finished the quarter down 3.4%, giving back almost half of last year’s total return. The only segments of the market to generate positive returns in the first quarter were those most sensitive to economic fundamentals: high-yield bonds and bank loans. Because assumptions about default rates are a key driver in those segments an improving economy provides a lift for them even as interest rates rise.

Given the current consensus that the global economy will continue its robust recovery through the second half of the year, the bond market’s focus on the risk of inflation is understandable. Adding uncertainty to the outlook for interest rates is the gap between the Fed’s rhetoric and market expectations for the Fed Funds Rate. Powell and other members of the Fed Open Market Committee are explicit about their focus on achieving maximum employment and have committed to holding policy rates at zero until average inflation tracks above 2%. The so-called dot plot, where Fed officials present their forecasts for interest rates, showed after the March meeting that the FOMC does not expect to raise rates until at least the end of 2023. Market expectations, as revealed by the pricing of short-term bonds and futures, reflect an expectation that the Fed will begin raising rates in 2022.

To close that gap either the Fed or the market will recalibrate expectations over the next two quarters as the path of the recovery is revealed. Supply chain bottlenecks have already driven big increases in the prices of some raw materials, most notably steel, but also intermediate and finished goods including computer chips, car parts, and appliances. Over the next few quarters, these bottlenecks should ease and supply should adjust bringing markets back into balance and mitigating the inflationary pressures. This is the scenario Fed Chairman Powell predicted when he indicated that the Fed will not respond immediately to short-term inflationary pressures but instead will allow inflation to run a bit above the 2% level in the interest of supporting the jobs market.

A more troubling inflation picture, and a more challenging environment for bonds, could play out if the extraordinary fiscal stimulus planned by the Biden administration, on top of Trump’s massive efforts last year, leads to a more robust and prolonged uptick in prices. Cash holdings by U.S. households now total over $4.4 trillion, an increase of almost 15% over the pre-pandemic levels at the end of 2019. If the economic expansion continues to accelerate and employment levels continue to rise as COVID cases decline, that cash hoard could be unleashed in the form of a big increase in demand while supply chains and productivity are still recovering.

The 2013 "Taper Tantrum" offers an interesting perspective on the market’s response to the withdrawal of central bank stimulus following an economic crisis. As the Great Financial Crisis unfolded in 2008-2009 the Federal Reserve embarked on Quantitative Easing under which it purchased large sums of bonds, providing liquidity to the financial system and supporting the prices of assets of all types. The Fed's response to the COVID crisis last year was similar; as investors fled risk assets of all types and sought the safety of cash and short-term securities the Fed stepped in with asset purchases to stabilize the markets and encourage consumers and businesses to spend and invest. That program is ongoing. The term “Taper Tantrum” refers to the short-lived but worrisome surge in Treasury yields in 2013 when the Fed announced that it would begin tapering its purchases of bonds, reducing the amount of liquidity it was feeding into the financial system.

With the economy recovering strongly from the crisis the Fed was able to return to a more normal policy, and while the market was briefly spooked the fundamental picture remained robust and the bond market normalized, albeit at higher yields than those needed to pull the system out of its spiral. Comparing the changes in the bond market in the first quarter of 2021 with the 2013 “Tantrum,” we see that yields have moved almost as much this year as they did then. So, if the economy continues to recover it's very possible that the Fed will be able to systematically reduce its bond purchases now, just as it was in 2013, without disrupting the economy. Of course many other variables are in play, but that precedent is encouraging.

Important Disclosures

Unless otherwise indicated, performance information for indices, funds and securities as well as various economic data points are sourced from FactSet as of December 31, 2020.

Wilbanks, Smith & Thomas Asset Management (WST) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. This material is not intended to replace the advice of a qualified tax advisor, attorney, or accountant. Consultation with the appropriate professional should be done before any financial commitments regarding the issues related to the situation are made.

This document is intended for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty and does not represent the performance of any specific investment strategy.

Some of the information enclosed may represent opinions of WST and are subject to change from time to time and do not constitute a recommendation to purchase and sale any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.