A Minsky Moment

Hyman Minsky, the late American economist and professor, is best known for a working paper published in May 1992, entitled “The Financial Instability Hypothesis.”

Minsky’s theory was rooted in observations around speculative borrowing, a practice itself driven by a key behavioral bias: belief that an extended rise in asset prices will last indefinitely. This overconfidence by investors, Minsky argued, causes them to discount the possibility of negative outcomes. In fact, it is the duration and magnitude of bull markets in assets which sow the seeds of the eventual decline of the underlying asset, with those most leveraged to the rise enduring the most distress. Minsky sought to underscore the risks of speculative bubbles by describing the panic investors feel when they collectively realize the uptrend has been breached.

Minsky’s theories gained only modest recognition and interest before he passed away in 1996.

But over a decade later as economists, businessmen and politicians clawed through the rubble of the subprime mortgage crisis, the Financial Instability Hypothesis began to receive urgent new attention. The effort to understand the cause and effect of the Great Recession (December 2007 – June 2009) led many to ponder Minsky’s hypothesis as an explanation for the depth of the economic decline. The term “Minsky Moment” was coined, in reference to that instant of collective panic.

But over a decade later as economists, businessmen and politicians clawed through the rubble of the subprime mortgage crisis, the Financial Instability Hypothesis began to receive urgent new attention. The effort to understand the cause and effect of the Great Recession (December 2007 – June 2009) led many to ponder Minsky’s hypothesis as an explanation for the depth of the economic decline. The term “Minsky Moment” was coined, in reference to that instant of collective panic.

It does not require an economics PhD to appreciate the impact of investor confidence on current and future asset prices. Anyone who invests money today expecting a future stream of cash flows assumes a level of uncertainty around those cash flows being realized, and it stands to reason they choose to invest based on some level of confidence in the probability of those cash flows occurring.

Confirmation bias in us will cause our confidence in our assumptions to swell the longer the uptrend lasts and the more money is invested in the trend. Not only do we find ourselves with excessive faith in an outcome that isn’t guaranteed, we tend to ignore evidence that challenges that faith. We are particularly vulnerable, then, to a supposedly sure thing that ultimately “just ain’t so.”

It is important to emphasize that gravitational forces do not beget a cyclical turn in asset prices in either direction. Investor swings between extreme optimism and pessimism have been documented in asset bubbles and collapses for centuries. History tells us they have existed in the past and one relatively safe bet is that they will persist in the future.

However, history provides little to serve as a guide for timing of such major inflection points. The value of Minsky’s theory is the self-awareness we must have to profit from an extended rise in asset prices without being overconfident in the strength and duration of that rising tide. Without it we lose perspective as to just how far we have come and what risks may be apparent only by looking in the rear-view mirror.

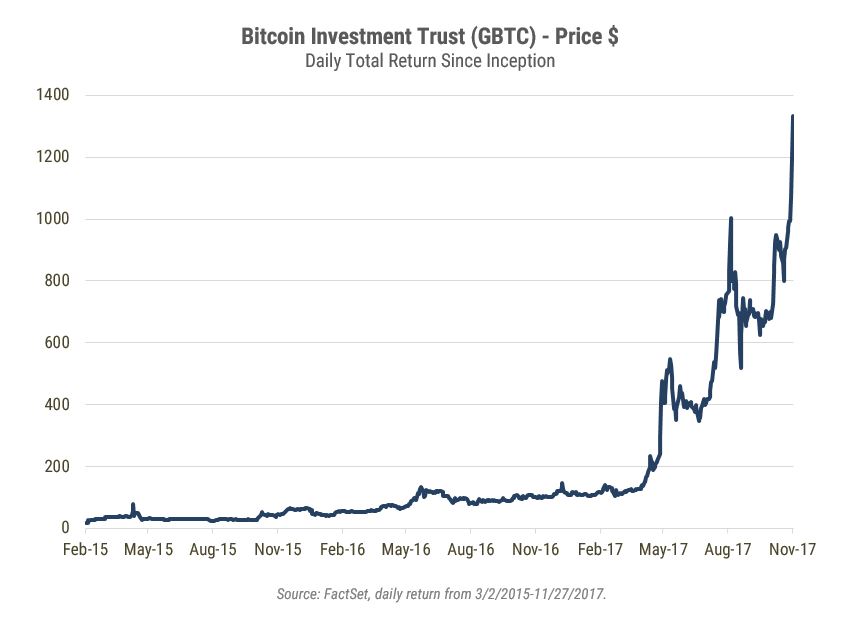

Bitcoin, for example, has mesmerized market watchers with its stunning surge over the past year and past six months especially. The below chart shows the rise of the Grayscale Bitcoin Investment Trust (GBTC), a mutual fund that trades bitcoin. The currency itself had reached $9,900 at press time, and CBNC reported yesterday about the trending Google search, “Buy Bitcoin with Credit Card.” CNBC’s Jeff Cox writes:

“...the popularity and curiosity of using leverage to get in on the action come as bitcoin's price continues to scale new heights… Google Trends says the search term "buy bitcoin with credit card" is around its historic peak, notes Nick Colas, co-founder of Data Trek Research and the first Wall Street analyst to take the digital currency seriously.”

As discussed previously, history provides little guidance as to when any asset will top out and which assets will decline in market events worthy of the "Minsky Moment" designation. Throughout the year, bitcoin has bucked skeptics and thrilled investors. Thus we are not attempting to predict future price action for bitcoin, nor are we recommending the purchase or sale of the currency or related access products. Our observation is simply that, according to these news reports, investors are literally leveraging themselves based on confidence in the continued upside of an asset that is up some 1000% in the past year. Our point is simply that a fact of investing is that it involves the risk of complete loss of capital. Investors who are confident in the prospects of a given asset may conversely be unalert to that possibility. Such investors are likely to be reluctant to sell and are thus positioned to be surprised by the severity of the decline.

Our closing thought comes from Richard Thaler, who won the Nobel Prize in Economics in 2017. Professor Thaler is known as a leading economist and researcher on the subject of behavioral finance. It is his work that has elevated the significance of understanding the internal and external influences on our decisions. Oftentimes these influences result in predictable, but poorly judged decisions which result from the behavioral biases we accumulate during our lifetimes. Not realizing which biases exist in us and which exist in other people is what makes market cycles.

Our closing thought comes from Richard Thaler, who won the Nobel Prize in Economics in 2017. Professor Thaler is known as a leading economist and researcher on the subject of behavioral finance. It is his work that has elevated the significance of understanding the internal and external influences on our decisions. Oftentimes these influences result in predictable, but poorly judged decisions which result from the behavioral biases we accumulate during our lifetimes. Not realizing which biases exist in us and which exist in other people is what makes market cycles.

For more articles like this, visit the WST Investment Perspectives category on the blog.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.